Source of Funds (SOF) examines how and where the client got the money for a specific transaction. On the other hand, Source of Wealth (SOW) explores the bigger picture, or the client’s entire financial situation and how they built up their total wealth.

Both SOF and SOW verification are key elements of Know Your Customer (KYC) protocols, recommended by the Financial Action Task Force (FATF) for anti-money laundering (AML) efforts. These checks verify the legitimacy of your customers’ funds and ensure they aren’t linked to risky or illegal activities, helping you better understand a client’s risk profile.

But why are these checks important, and what are the main differences between them? This simple guide answers all these questions and explores key topics, such as the regulatory landscape and issues linked with Source of Funds (SOF) and Source of Wealth (SOW).

What is Source of Funds (SOF)?

Source of Funds (SOF) describes the origins of where the money in a specific transaction or investment comes from. This can be proceeds from selling a property, gifts, personal savings accounts, or even gambling winnings. Companies gather this information from their customers to verify that the transactions are not being used for money laundering and other financial crimes.

SOF verification involves tracing the money back to its original source to ensure it was acquired legally. In practice, companies ask the customer to provide proof, such as pay slips or bank statements confirming the sale of an asset. If the funds originate from the customer’s business, the company can ask for business financial statements or transaction records to confirm the money was earned legally.

Source of Funds (SOF) Examples

Some common examples of Source of Funds (SoF) include:

- Income from employment

- Personal or joint savings accounts

- Inheritances or gifts received

- Compensation from legal settlements

- Profits from investments or legitimate business activities or

- Proceeds from the sale of assets such as stocks or real estate

So, if a customer wants to invest a significant sum in a mutual fund, the financial institution will need to conduct an SOF check and:

- Evaluate the risk level associated with the transaction by considering factors like the presence of a gift, the origin of the funds, and the complexity of the transaction structure.

- Request documentation like bank statements or records that trace the money back to its source, such as the customer’s salary, a gift from a family member, or proceeds from a business sale.

- Record the decision-making process, noting the reasoning and any relevant details, in the client’s file for future reference. This helps verify that it matches expectations and that the client’s explanation is consistent with their known background.

Criminals often attempt to inject their illegal funds into the financial system by concealing their origins through layering. That’s why verifying the Source of Funds is crucial for identifying, preventing, and reporting potential money laundering.

What is Source of Wealth (SOW)?

Source of Wealth (SOW) refers to the origins of the person’s total wealth that they have acquired throughout their whole life. An SOW check is designed to help assess various activities that have contributed to an individual’s total wealth, which have contributed to its growth. This way, financial institutions can detect undisclosed income, hidden assets or illegally obtained funds.

For example, if a high-net-worth customer wants to open a private banking account, their bank will check their Source of Wealth. When evaluating a person’s SOW, companies consider factors such as business ownership, real estate holdings, investments, and inheritances. With SOW, the goal is to construct a profile that verifies the customer’s legitimate wealth.

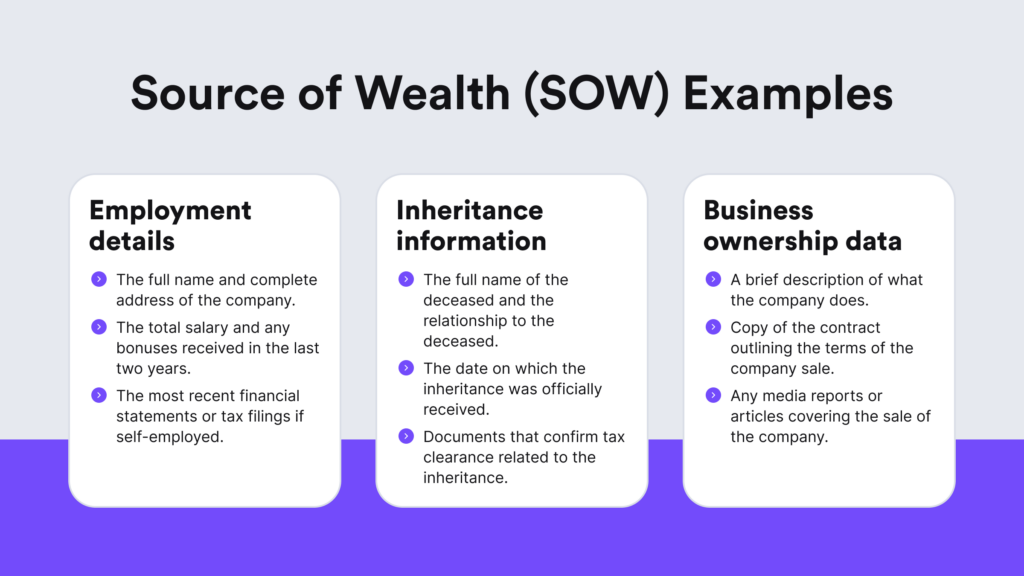

Source of Wealth (SOW) Examples

Some common examples of Source of Wealth (SOW) include:

- Family inheritances

- Investments

- Business ownership

- Earnings from employment

Consider a customer with a net worth of hundreds of thousands of dollars. An SOW check shows the person established this wealth through a successful software engineer career, real estate investments, and a family inheritance. The financial institution would then confirm these details using employment records, inheritance documents, and investment statements.

SOW checks are also part of the Know Your Customer (KYC) compliance framework that allows businesses to:

- Identify when clients are acting on behalf of another individual, a family member, or a corrupt official.

- Gain a more comprehensive understanding of a client’s risk profile and overall financial background.

Consequently, SOW verification allows businesses to manage risk by verifying that their clients have legally acquired their wealth. This process is vital, especially when dealing with high-risk and high-net-worth individuals or those engaged in complex financial transactions.

What is the Main Difference Between Source of Funds and Source of Wealth?

Even though there are similarities between Source of Funds (SOF) and Source of Wealth (SOW), such as both checks help companies assess customer risks, both checks focus on different aspects. SOF examines the money used in a specific transaction to determine its origin. In the meantime, SOW explores how the customer built their wealth over time.

The difference lies in the depth of the investigation and the focus of the inquiry:

- SOF looks at the money used in a specific transaction and answers the question, “Where did this money come from?”

- SOW explores how a customer built their wealth over time and answers “How did this customer become wealthy?”

Both SOF and SOW checks could include employment income. Despite that, SOF examines the money used in a specific transaction, while SOW looks at the accumulation of funds over time, offering a broader view of the person’s financial history.

In financial due diligence, understanding the difference between Source of Funds and Source of Wealth is crucial, as it extends beyond their basic definitions. By clearly understanding how SOF and SOW interact, companies and compliance professionals can perform more thorough due diligence and risk assessments.

The Role of SOF and SOW Checks

The FATF recommends SOF and SOW checks as part of a company’s AML compliance efforts. These checks are also critical components of KYC protocols, which include an enhanced due diligence (EDD) approach, which helps financial institutions and other obliged entities to conduct thorough risk assessments.

By conducting SOF and SOW checks, companies can:

- Assess a person’s financial history

- Uncover complex financial schemes or hidden assets

- Identify any discrepancies and undisclosed activities

- Detect potential risks of money laundering or illegal activities

In the context of KYC and AML compliance, verifying both SOF and SOW is crucial. Both checks enable institutions to identify AML red flags and implement measures to mitigate risks.

What are Some SOF/SOW Compliance and Regulatory Considerations You Should Know?

AML guidelines heavily emphasize the importance of verifying SOF and SOW as key parts of compliance efforts. Companies must use a risk-based approach when setting requirements for conducting SOF/SOW checks. That means they should apply measures that are reasonable and proportionate to the client’s potential money laundering and terrorist financing risks.

For example, in the United States, SOF checks are required under the USA PATRIOT Act for specific types of customers, such as Politically Exposed Persons (PEPs) who are considered high-risk individuals due to holding significant public roles and increased possibility of money laundering or corruption.

Additionally, regulatory bodies like the FATF set out frameworks, such as the 40 Recommendations, that financial institutions later follow. These regulations provide detailed steps and procedures that institutions should use in their due diligence processes. Companies should use them to guarantee that their SOF and SOW checks are properly executed, assessed, and conducted to prevent and detect money laundering, terrorist financing, and other illegal activities.

The Importance of Source of Funds and Source of Wealth in AML Compliance

Implementing AML compliance measures is crucial for fulfilling regulatory requirements. Beyond regulation, Source of Funds and Source of Wealth checks also safeguard a company’s reputation and integrity, enhancing customer trust and overall financial system security.

Even companies not legally mandated to perform these checks often do so voluntarily as part of their internal controls to strengthen their risk management systems. In-house compliance officers play a key role in this process because they establish internal controls, monitor transactions, and also take part in improving the company’s AML program to reduce the risks associated with money laundering.

When AML software flags unusual patterns or transactions, the company typically initiates SOF/SOW checks. A classical example would be in cases when a customer exceeds a specified threshold, and they’re asked to demonstrate that their funds come from a legitimate source. If these transactions raise suspicions, a company must file a Suspicious Activity Report (SAR).

What Actions Should I Take If I Have Concerns Regarding the Source of Funds?

There are several actions that you should take, depending on your company’s risk tolerance.

For example:

- Using EDD measures for further assessment

- Escalating the case to senior management

- Applying monitoring to the customer’s transactions

- Stopping the transaction

- Ending the business relationship/not onboarding the customer

Related: How Does an AML Investigation Work? [5 Steps]

How to Perform SOF/SOW Verification?

If your business is in the financial sector, you need to continuously track the Source of Funds (SOF) and Source of Wealth (SOW) for all your customers. That said, data analysis is crucial in the SOF/SOW verification process.

For PEPs, additional measures are necessary under CDD procedures for private banking to establish the SOW. If you detect any suspicious activity, you must fill out a SAR and report the case to the relevant authority, such as FinCEN.

Using AI-powered AML tools and screening mechanisms, financial institutions can spot suspicious patterns in transaction data, such as:

- Frequent large transfers

- Complex chains of transactions

- Sudden changes in the customer’s financial behavior

Companies initiate SOF/SOW checks when a user’s transactions exceed a predefined threshold, such as exceeding $100,000 or multiple transactions within a short time frame.

SOW checks are useful when starting a new business relationship, helping entities detect illegal cash flows, such as third-party money laundering. Depending on their source of wealth, companies need to request various types of documentation. This can include records of previous transactions, public property registers, copies of trust deeds, tax returns, bank statements, etc.

Why You Should Apply an Automated Approach to SOF/SOW Checks

To make informed decisions about their customers’ Source of Funds or Source of Wealth, companies need to have a proper KYC and AML program, which includes:

- Verifying customer identities by requesting various pieces of identifying information, such as names, addresses, dates of birth, and details of company incorporation.

- Determining the beneficial ownership before getting tangled in suspicious new business relationships and conducting proper Know Your Business (KYB) checks.

- Screening PEPs and sanctions lists to detect any changes in the PEP status and checking customer names against relevant sanctions and global watchlists.

- Monitoring transactions to identify any activity that deviates from established SOF, including transactions involving high-risk jurisdictions.

Great news — at iDenfy, we have all the RegTech tools in one place to automate these processes.

Our compliance toolkit enables you to apply an automated approach to SOF/SOW compliance and efficiently process large data volumes, identify potential risks, minimize manual errors, and, more importantly, also enhance your ongoing due diligence.

Our KYC/AML and KYB tools help you quickly detect any suspicious or unusual activity related to Source of Funds or Source of Wealth. Get started right away.