Did you ever wonder what fraud feels like? Well, probably, because companies have to be safe from fraud, and to be safe from fraud, you have to imagine what one looks like. This thing called fraud is evolving fast and impacts businesses and companies worldwide, causing them to suffer reputational damage and financial losses. So the next question that comes to mind is, would you want to experience fraud? No? Well, we did expect such an answer, but just to be completely safe, we will discuss the cost of fraud, which can sometimes be immeasurable.

The True Cost of Fraud

Many businesses underestimate fraud and its capabilities. Sure, sometimes it can be lighter than for other companies, but you can not ignore the fact that it can also hit as hard, carrying the business or company to bankruptcy.

According to recent studies, global fraud losses amount to trillions of dollars annually, with cyber fraud and identity theft being the most common threats. Here’s the cost of fraud:

Direct Financial Losses:

Fraudulent transactions, chargebacks, unauthorized access, and what not can result in substantial revenue losses for businesses, disrupting the cash flow and impact overall profitability, the fraud reaches its objective, making it difficult for companies to maintain stability.

Additionally, businesses often have to deal with fraudulent transactions, even when they are not at fault. This not only leads to direct monetary losses but also increases administrative costs associated with fraud prevention and dispute resolution.

Shopify merchants can also reduce chargeback losses and automate the dispute process with solutions like Chargeflow, which helps recover revenue and minimize operational strain caused by post-purchase fraud.

Reputational Damage

When users experience fraud on a business or company platform, their trust in the company instantly disappears, keeping them further away from the institution. A damaged reputation can have long-term problems, as it is not easy to make everything right again – public distrust may keep potential users away from the company.

Low-security measures leading to fraud can result in negative reviews on social media and review sites, and as a result, user retention declines, making it harder for the business to maintain a loyal user base and attract new clients.

Legal Compliance

Lots of regulations around the world, for example, GDPR, require businesses to prioritize data protection and fraud prevention – involving investigation of security measures and ongoing audits, to ensure adherence.

Failure to comply with these standards can lead to several issues for the business, like fines and legal repercussions. In addition to financial costs, non-compliance can damage a company’s credibility, making it challenging to regain user trust.

Operational Disruptions

A common thing is that fraud investigations require a lot of resources, and it comes from the business itself, required mainly for compliance audits and the investigations itself, meaning that attention from main operations is diverted, reducing productivity and increasing operational inefficiencies.

Security and user support resources are also has to be deployed for future fraud prevention, which leads to increased costs and delays in other business functions, affecting overall performance, but what can you do when your business was affected by fraud, only implement stronger security measures, no matter the cost.

Customer Churn

When we are accessing a site, we always expect a secure environment, especially for transactions, and any security breach for users would be a big surprise, leaving us dissatisfied. When users perceive a company as unsafe, they are more likely to take their business elsewhere.

Fraud increases churn rates as users seek safer alternatives, and retaining users after a security breach requires significant effort, including transparent communication and improved security measures.

Common Types of Fraud Targeting Businesses

If you do not know your enemy that well, it will be hard to fight it effectively. In this case, businesses must understand the different types of fraudulent threats and activities they might see appear:

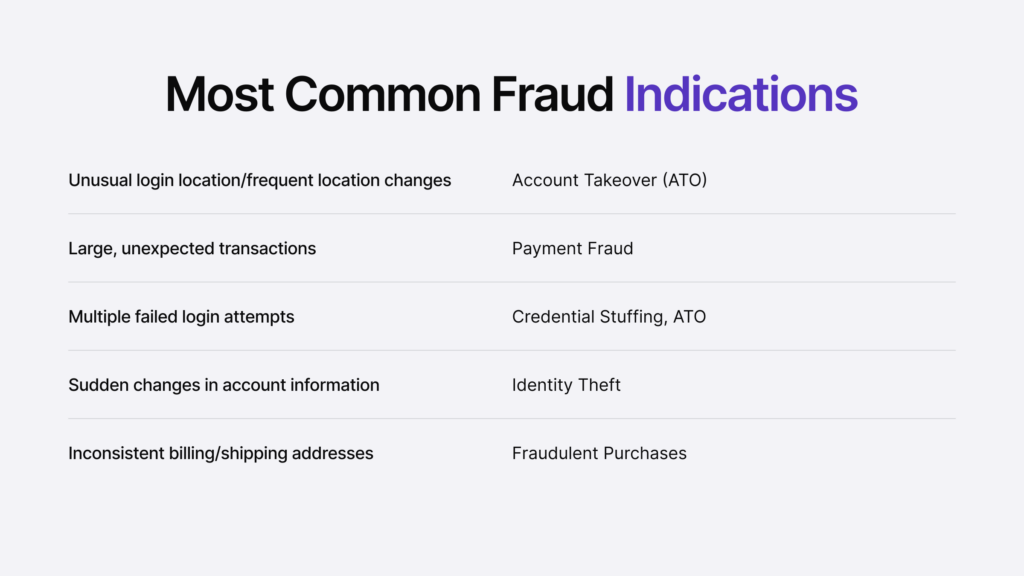

- Payment Fraud: Involves unauthorized transactions and mostly chargeback fraud.

- Identity Theft: Fake and stolen identities are used by fraudsters to commit fraud.

- Account Takeover (ATO): Hackers gain access to legitimate user accounts and conduct fraudulent activities.

- Phishing Scams: Fake emails, phone calls, messages, and websites trick users into providing sensitive information.

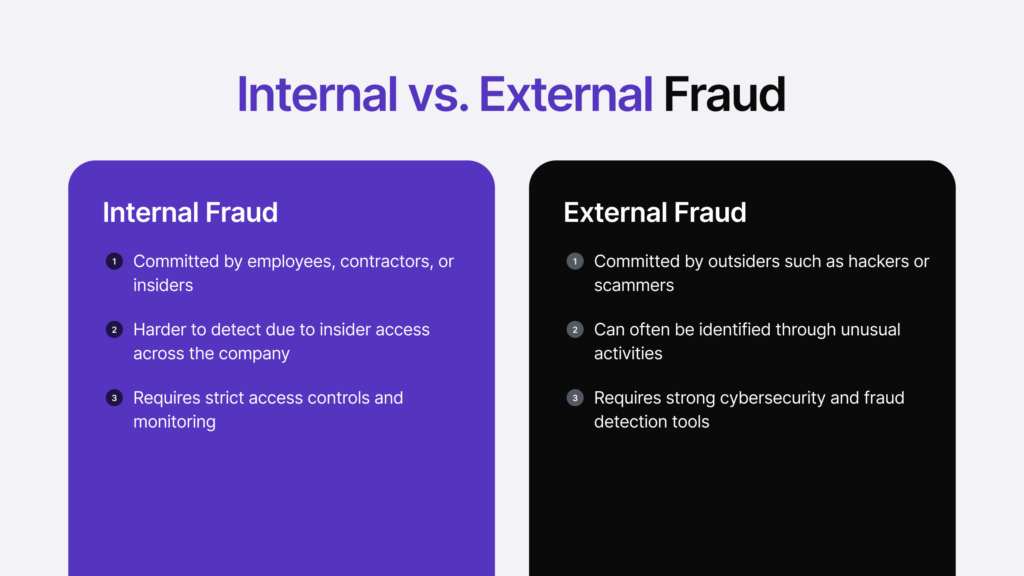

- Insider Fraud: Employees misuse company resources for personal gain – embezzlement is a perfect example.

- Return and Refund Fraud: Fraudsters exploit loopholes in return policies to receive funds for fraudulent purchases.

Related: What is Fraud Detection?

Top Anti-Fraud Strategies

Now that we know and understand the actual cost and types of fraud let’s discuss anti-fraud strategies that are proven to be effective and that businesses should implement to protect their assets and enjoy a safe journey through the digital world.

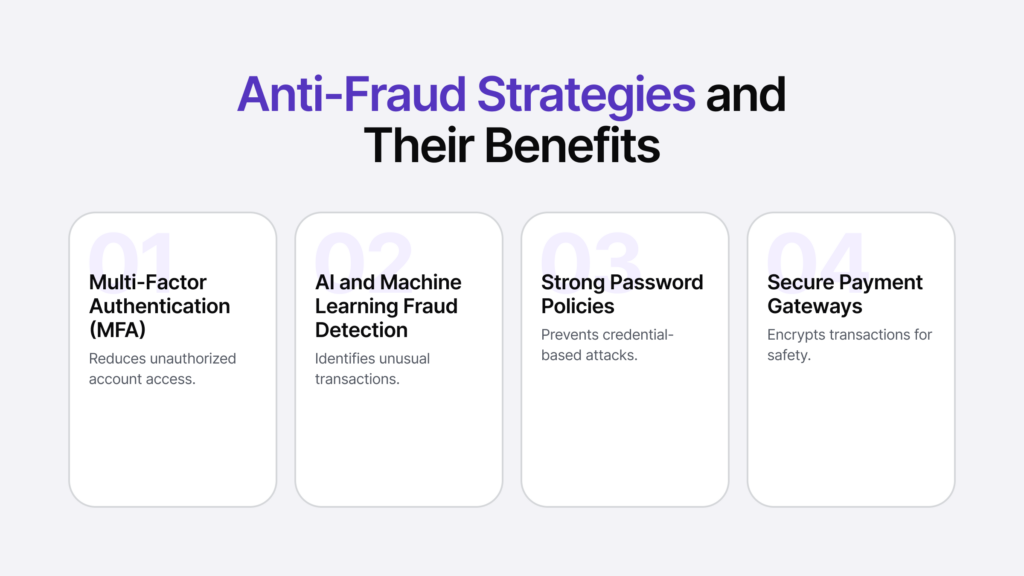

Multi-Factor Authentication (MFA)

MFA is widely used by various organizations as it requires users to verify their identity through many authentication methods. The methods can be something they know (a password), something they have (a mobile device), or something they are (biometric verification). MFA can significantly reduce the risk of unauthorized access and account takeovers.

On the other hand, fraudsters find it more difficult to compromise accounts, even if they have passwords and usernames stolen from the users. MFA helps all the systems and user accounts protect sensitive data and prevent fraud-related incidents.

Related: New Account Fraud — Alarming Red Flags and Ways to Fight Back

AI and Machine Learning for Fraud Detection

AI and ML tools were not as good as they were then, but if you compare them 10 years ago to now in fraud prevention and detection, they are way better than before. Employees can sometimes feel tired from analyzing a lot of data daily, but with these technologies, everything is more straightforward – they can detect unusual patterns and flag fraudulent activities in real-time, easing employee work.

AI also adapts to new fraud tactics, learning and making security more effective over time. Automated fraud detection helps reduce false positives and improves accuracy in identifying threats.

Transaction Monitoring and User Behavior

An automated monitoring system set up will help the organization to track user behavior and transaction history which is very important for detecting fraudulent activities. Unusual transactions and multiple failed login attempts should trigger real-time alerts for further investigation by the employee team.

The identification of potential fraud becomes relatively easy by continuously monitoring transactions for various organizations. Organizations should also implement behavioral analytics for fraud detection, as they can add another security level, preventing unauthorized access to other accounts, which organizations would not want to miss.

Employee Education on Fraud Risks

Human errors were and are common mistakes that are a leading cause of fraud incidents, making education a really important addition to fraud prevention. Users and the whole company will feel safer knowing that their employees have been trained effectively, allowing them to easily recognize phishing attempts and social engineering tactics.

The lectures and training can sometimes be a bit boring, and some information could be easily forgotten, so try to make presentations or the training as a whole somewhat interesting because a well-informed employee creates a stronger defense against potential fraud.

Related: First-Party, Second-Party, and Third-Party Fraud

Implementation of a Business Verification Procedure

Doing a business verification procedure and implementing it in your business is one of the most effective ways to lower the risk of fraud. Such a process ensures the reduction of chances of dealing with fraudulent institutions and making sure that the transactions are legitimate. The whole process consists of verifying the very details of a business’s incorporation country, shareholder’s data, and activity code, from which organizations can gain valuable information about a business’s legitimacy and financial stability.

Also, businesses are checked for global sanctions and law enforcement records to ensure they are not associated with criminal activities or corruption, which is evenly worse. Incorporation of automated risk assessment tools, businesses are capable of flagging high-risk institutions or individuals and taking necessary actions before proceeding with transactions. These verifications contribute to an overall conclusion – final risk score – helping businesses determine whether to proceed with the partnerships

Secure Payment Gateways and Data Encryption

If the organization uses end-to-end encryption, tokenization, and secure payment gateways, it ensures secure payment processing, which is one of the most important things for protecting users’ financial information. Without it, the organization could face legal consequences.

Businesses should also partner with compliant payment processors to maintain security standards and prevent breaches. Measuring across all digital touchpoints will help to prevent unauthorized data access and ensure compliance with security regulations.

By using these anti-fraud strategies and methods, the true cost of fraud could be mitigated to its lowest, and the company or organization as a whole could be saved from financial and trust losses that could affect it negatively.

Conclusion

Fraud is constantly spreading, and businesses can not afford to ignore it because the reputational and operational costs of fraud can be devastating, but they can be avoided by adopting top anti-fraud measures that will keep the organization safe. It is safe to say that business protection from fraud is not a one-time thing; it is an ongoing effort that helps organizations stay ahead of the fraudsters.