Just imagine you are at a bank, taking out your wallet to show your ID, trying to prove you are not some shady character off the street. Now fast-forward to 2025 – same deal but with a little twist – everything is online, and the stakes are sky-high because there are just so many people, and some of them can be fraudulent. This is where KYC comes in. Short for “Know Your Customer,” it is making sure businesses do not accidentally buddy up with some bots and fraudsters.

Many people just roll their eyes at the KYC procedures, thinking it is just another additional safety measure, but it is much more than that – a system that keeps the digital world together. Interested in learning what is KYC? Its functionalities, its procedures, and everything else it has to offer to a world of security? Look no further; we will cover it right now.

What does KYC Mean?

KYC, or Know Your Customer, refers to a set of processes by financial institutions, businesses, banks, iGaming platforms, adult websites, other companies to confirm the identity of their users and customers. The main goal of KYC is to prevent illegal financial activities, which is very common in today’s digital world, for example, money laundering is one of the most common fraudulent activities out there, as well as the identity fraud.

The process typically includes three main steps:

- Customer Identification Program (CIP) – Verifying the identity of a user using official documents like a passport or a bank service to verify the identity.

- Customer Due Diligence (CDD) – The user risk profile is assessed to analyze their financial transactions.

- Ongoing Monitoring – Continuously track transactions and user behavior to monitor their activities.

This process makes KYC as a whole, and without it, the operations and maintenance of compliance with global KYC regulations would be impossible.

Automate your KYC process

iDenfy verifies customers from 200+ countries in seconds. AI-powered, compliant, and trusted by 1,000+ companies.

Explore KYC SolutionWhy is KYC Important?

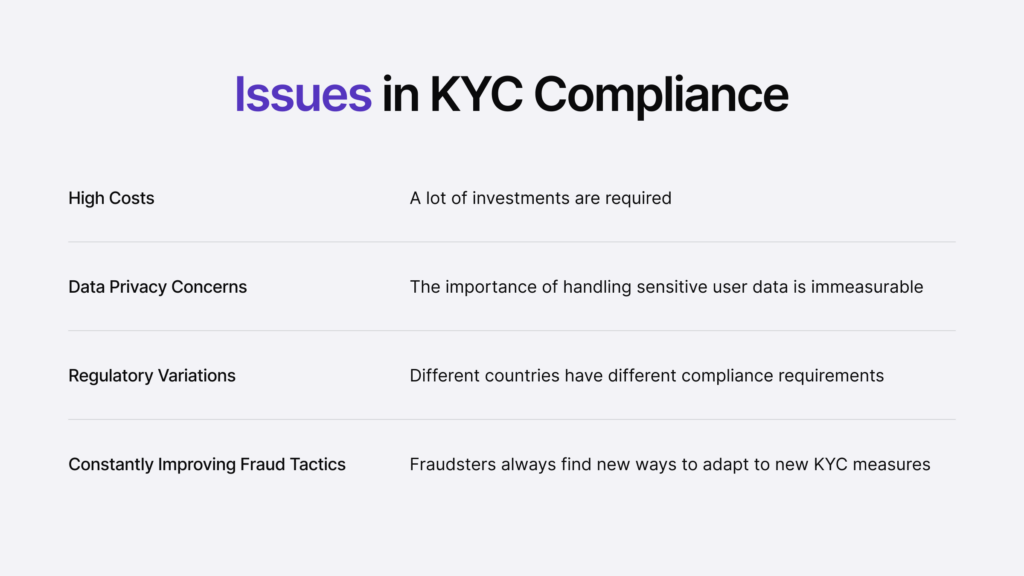

KYC is not just a regulatory requirement that is implemented only because of the fines that the company would get without it; also maintains the integrity of the financial system and many other things, which we will take a look at:

Financial Crime Prevention

With the verification of user identities, KYC helps prevent money laundering, fraud, illegal activities, and other digital crimes, ensuring businesses are not unknowingly facilitating criminal operations – criminals keep financial systems often exploited, and banks made their primary targets, to move and transfer illegal funds, but with the strict KYC measures in place, a barrier is created by requiring valid documentation and thorough identity checks and verifications.

This process reduces the chances of fraudulent transactions and improves the overall security of financial institutions, and with the implementation of strict KYC procedures, businesses can easily detect unusual activities early and prevent them from happening, report to the authorities, and mitigate financial risks effectively.

Customer Trust

If I were a customer and a user of such a site that handles my payments, I would want to feel as safe as possible. The KYC process does just that – it makes customers and users feel secure, and businesses can be trusted to handle their customers’ payments. When businesses implement strong KYC procedures, they show commitment to customer interests and prevent identity theft, which is very common.

It also encourages more individuals to engage with financial institutions without fear of fraud or unauthorized access. A secure and transparent financial environment leads to higher customer satisfaction and loyalty, meaning they will trust the institution and return to use the services more.

Regulatory Compliance

Government and financial regulators mandate KYC compliance to ensure transparency in financial transactions, meaning that failing to comply with the regulations can lead to some serious reputational damage and legal penalties, which could be hard to cope with for companies, especially the smaller ones. All around the world, financial institutions are required to implement KYC; without it, the company could just cease to exist.

Non-compliance can result in fines, including operational restrictions and loss of customer trust, negatively impacting a company’s standing in the industry. Long story short, KYC is mandatory and not optional these days.

Risk Reduction for Companies

It is vital to understand customer behavior and the risk levels that companies are facing every day, which is only a matter of time to crumble against one of the risks, no matter – if it is a financial risk or maybe something from inside the company like embezzlement, the company has to be safe and have to know how to make informed decisions and avoid potential liabilities. With proper risk management, companies can minimize losses associated with fraud and other risks.

KYC does a good job of protecting the financial institution and keeping the economic environment stable and secure, protecting businesses from financial damages, and maintaining a trustworthy reputation in the industry.

Operational Improvements

Automated KYC procedures streamline the user onboarding process by reducing the time and effort required for manual verification, increasing business productivity while maintaining compliance, if that is not enough, digital KYC solutions help financial institutions quickly and accurately verify identities, which gives a result of a smooth and efficient onboarding process.

This increased efficiency minimizes slow administrative processes, boosts user satisfaction (as they are verified in seconds), and helps to ensure that regulatory requirements are met without unnecessary delays. Leveraging advanced technologies can strengthen security measures while optimizing workflow management.

Global Acceptance

As financial institutions operate across borders, KYC helps ensure consistency in compliance standards, which makes international transactions more secure and transparent, – allowing companies to operate in multiple countries, which reduces the risks associated with cross-border financial crimes.

This global approach can be trusted among international partners and strengthens the financial ecosystem by promoting transparency and accountability, meaning that compliance standards, financial institutions can collaborate effectively while ensuring that regulatory expectations are consistently met worldwide.

Key Components of KYC

KYC compliance consists of several essential elements which it would hardly, most likely cease to exist without them:

- Customer Identification Program (CIP)

This step involves collecting basic information such as name, date of birth, address, government-issued IDs, and other documents that are related to the person who needs the verifying process, just to be sure that they are legit and are not fraudulent.

- Customer Due Diligence (CDD)

Customer Due Diligence is a risk assessment tool that looks at user background, business relationships, and financial transactions, and based on that, it sets a certain risk level. There are various types of levels of due diligence, here are some of them:

- Simplified Due Diligence (SDD): Mainly for low-risk profiles.

- Basic Due Diligence (BDD): Standard verification process for most profiles.

- Enhanced Due Diligence (EDD): For high-risk profiles, requiring more extensive checks.

These periodic reviews will ensure the company that regular users remain compliant and help businesses identify any red flags that may appear as red flags.

- Ongoing Monitoring

KYC does not end after onboarding; it is a constant process of monitoring verified users so that companies do not have to deal with fraudsters who appear out of nowhere after a certain amount of time. The monitoring includes screening transactions, high-value transfers, or other red flags that may indicate fraud.

- Risk-Based Approach

A risk-based approach helps companies have their KYC process based on the risk level of individual users, such as low, mid, and high-risk users. Low-risk users are not monitored as deeply as high-risk users, who are more likely to commit fraud or illegal activities.

iDenfy Risk-based approach walkthrough

KYC Regulations Around the World

Different countries have different regulations for KYC – most of the countries must follow global regulations, such as:

- EU: The European Union’s Anti-Money Laundering Directives (AMLD).

- USA: The Bank Secrecy Act (BSA) and the USA Patriot Act – KYC compliance for financial institutions.

- India: The Reserve Bank of India (RBI) – KYC regulations for banks and financial institutions.

- UK: The Financial Conduct Authority (FCA) – KYC compliance under AML laws.

- Singapore: The Monetary Authority of Singapore (MAS) mandates KYC processes.

- Australia: The Australian Transaction Reports and Analysis Centre (AUSTRAC) – KYC obligations for financial service providers.

Compliance with these regulations ensures businesses operate legally and ethically – things that we want the most.

Conclusion

So, what is this thing called KYC? Well, KYC, or for short Know Your Customer, is a process that provides a very high security level to financial institutions and regulatory compliance, which, without KYC, companies just could not survive. As we all know, regulations and fraud techniques are continuously improving, so companies have to take specific steps and measures to be safe from various fraudulent activities, and the KYC is a good step towards a safer tomorrow.

Curious about how iDenfy can make KYC faster, more secure, and customer-friendly? Let’s continue the conversation and see how we can help you stay ahead in the growing financial landscape.