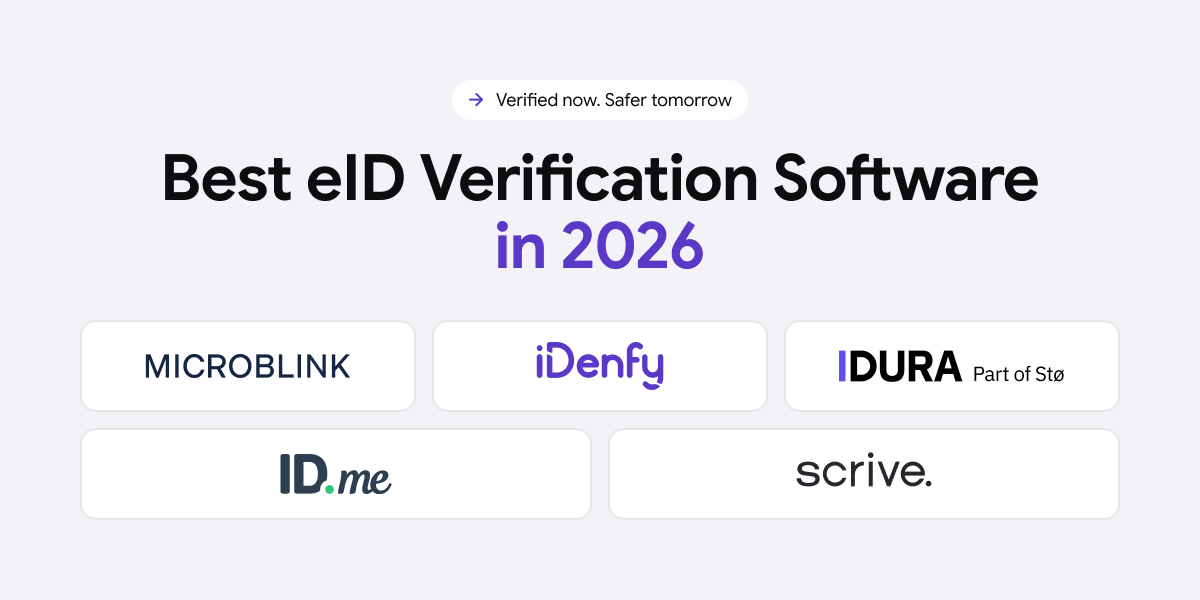

| # | Name | Score | Description |

| 1 | iDenfy | 4.9 |

All-in-one RegTech platform offering both document-based/registry-based verification methods and the widest eID provider coverage, from BankID to CLEAR and SmartID |

| 2 | IDURA | 4.7 |

Developer-first eID broker specializing in Scandinavian and European national digital identities via a single OIDC integration |

| 3 | ID.me | 4.1 |

US-focused digital identity network with federally accredited identity proofing and a reusable credential wallet |

| 4 | Microblink | 3.8 |

AI-powered document verification platform with eIDV database-matching and watchlist screening capabilities |

| 5 | Scrive | 3.9 |

European eIDAS-compliant platform combining national eID authentication with qualified electronic signatures |

We also look through the key points regarding eIDs and eID verification before breaking down the best provider list.

What is an eID?

According to the European Commission, eID, or Electronic Identification, also sometimes referred to as e-identification, is a digital method for verifying a person’s identity online, often without requiring the submission of a photo of their physical ID document (like a capture of a passport or their driver’s license).

In other words, eID is a compliant, non-document verification method (common in the EU) that is the digital equivalent of physical ID documents. For example, it works through open banking or other means that can access, extract, and cross-match already logged identity data and use it for identity verification.

➡️ An example of such a flow is iDenfy’s Swedish Bank ID solution, which is a widely popular eID in Sweden, where users are automatically redirected to the Bank ID app.

What is eID Verification?

eID verification is a non-document verification method of confirming a person’s identity using pre-verified digital credentials: government-backed (such as full name, date of birth, address) or bank-issued digital identities (log-in credentials, bank account details, etc.) that users already hold.

This approach is different from traditional, document-based identity verification (common in strictly regulated industries, like banking, where Know Your Customer (KYC) checks are required), because:

- It relies on trust already established by a bank, government authority, or accredited scheme — meaning no document scanning, no selfie, and no OCR is required.

- It cross-matches the user’s identity against official records at the source, not re-examined by a third party.

In practice, eID verification works similarly to Open Banking: the user consents to share data held by a trusted authority, and the business receives a verified, authoritative response. For example, in Europe, this is governed by the eIDAS regulation, which establishes mutual recognition of national eID schemes across EU member states.

Evaluation Criteria for the Best eID Verification Software

When evaluating eID verification software in 2026, the following factors matter most for businesses:

The Scale of Supported eIDs

Different markets use different national eID schemes. BankID dominates in Sweden and Norway, MitID in Denmark, FTN in Finland, Smart-ID across Estonia, Latvia, and Lithuania, OneID in the UK, CLEAR in North America, etc. The more providers a platform supports through a single integration, the more geographies the business can serve without rebuilding its verification flow or having to partner with multiple vendors, which damages sustainability.

Integration Process Simplicity

Rather than negotiating and integrating separately with each eID provider (a process that can take weeks in some cases), the best eID verification software acts as a broker. In practice, this allows businesses to connect once and access all supported eIDs through a single API. This is especially critical for businesses that work in different markets and want to improve conversions by providing a familiar flow (different eID verification triggered based on the user’s entered country or selected bank, etc.)

Data Sources Used in Line with KYC Compliance

A proper eID verification service provider should cross-match legally verified personal data, such as the user’s full name, date of birth, national identification number (CPR, personnummer, etc.), and, where available, registered address, directly from the authoritative registry. This is important for regulated industries, where KYC and Anti-Money Laundering (AML) requirements are very important.

Related: eIDV: Electronic Identity Verification (Definition, Examples & More)

Use Case Flexibility

eID should support more than a single use case, or one-time user registration/onboarding. Leading software providers also support re-authentication of returning users, transaction approvals, digital signing, age verification, caller authentication, and address verification, all using the same eID credential. This is especially vital for good user experience, since it directly impacts drop-offs that can happen during user onboarding.

Pricing Transparency

Common models include monthly platform fees for verification credits plus per-verification transaction fees. Naturally, the specific cost of each eID method can vary since some national schemes charge different rates. Clarity about what triggers a charge, and other factors, whether testing is free, is important when you’re planning your verification budget.

#1 iDenfy

4.9 Average Score · (4.8 Capterra | 4.9 G2 | 5.0 TrustRadius)

Website: www.idenfy.com

iDenfy is a global all-in-one identity verification, fraud prevention, and compliance platform, specializing in RegTech products, such as eID onboarding. Apart from the initial registration process, iDenfy covers AML tools for screening and ongoing monitoring (such as PEPs & sanctions or adverse media checks), as well as an end-to-end Know Your Business (KYB) platform for corporate client compliance.

In the eID space specifically, iDenfy stands out for offering the broadest combination of national digital identity providers in a single platform, covering BankID (Sweden, Norway, and the Czech Republic), MitID (Denmark), Smart-ID (Lithuania, Estonia, Latvia), FTN (Finland), OneID (UK), CLEAR (North America), Verimi (Germany), and SPID (Italy).

Best for: Businesses that need to verify users across multiple European and North American markets using a single integration, particularly in fintech, iGaming, lending, and e-commerce.

How the Flow Works

- User selects their eID provider at onboarding or is redirected directly based on country

- User verifies themselves via their existing digital identity app (no document upload required)

- Verified personal data (name, date of birth, national ID number, address, where available) is returned from the authoritative source

- Data is cross-matched against the business’s onboarding requirements

- Optional: additional KYC layers (document check, liveness, AML screening) can be appended to the same session, or if the eID flow isn’t supported in a specific country

iDenfy’s eID flow works without requiring the user to upload a physical document. Instead, the user is redirected to their chosen digital identity provider, for example, Swedish BankID, where they authenticate using the app they already have on their phone. After a successful verification, verified identity data is returned to iDenfy and passed to the business. This is a genuinely frictionless process for users in markets where national eIDs are widely adopted.

Compliance

- eIDAS-compliant for EU eID flows

- AML-compliant; supports full KYC workflows when combined with document and AML checks

- KYC Risk Assessment with configurable rules and scoring weights

- PEP screening (all 4 levels), sanctions checks, and ongoing monitoring available as add-ons

Pricing

- Pay per successful verification

- No charge for failed or incomplete sessions

- Book a demo for pricing details

iDenfy operates on a pay-per-successful-verification model, which means businesses are not charged for failed or incomplete sessions. For industries like iGaming, where a high rate of fraud (KYC bypassing attempts through deepfakes, for example) is a common issue, this saves at least 2x costs, and is extremely beneficial.

You can review and calculate the actual ROI for identity verification using iDenfy here.

#2 IDURA

4.7 Average Score (based on developer community reviews and integration feedback)

Website: www.idura.eu

IDURA (formerly Criipto) is a Denmark-based eID broker and authentication platform built specifically for developers who need to integrate national electronic identities into their products. Where iDenfy offers eID as part of a broader identity and compliance platform, IDURA is more focused: its entire product is built around connecting businesses to national eID schemes, and doing so as smoothly and quickly as possible.

IDURA’s approach is straightforward. A business integrates once using OpenID Connect (OIDC) and OAuth2 — the same standard protocols used by any OAuth2 login flow — and then selects which eIDs to activate for their user base. From that point, adding a new country market requires activating a new eID in the dashboard, not a new integration. Beyond authentication, IDURA also supports eID-based digital signing, address lookups from national registers, and age verification, all built on top of the same eID flow.

Best for: SaaS companies, fintechs, and digital services expanding primarily across Nordic and European markets that need a fast, developer-friendly, standards-based eID integration.

How the Flow Works

-

One simple integration

The business integrates once using standard OIDC/OAuth2 protocols. There’s no need to re-integrate for every national eID scheme, since the connection works across supported providers.

-

User authenticates with their national eID

The user is redirected to their trusted national eID provider, where they log in in a familiar and secure environment. This keeps the experience consistent and reassuring.

-

Verified identity data is returned securely

After successful authentication, verified identity details, such as name, date of birth, and national ID number (for instance, SSN, CPR, personnummer), plus address if enabled, are securely returned.

Supported eID Providers

- Swedish BankID

- Norwegian BankID

- Danish MitID

- Finnish Trust Network / FTN (aggregates all Finnish bank and telecom eIDs)

- Belgian itsme® (active in 16 countries)

- Freja (international eID; supports passport holders from 167 countries)

- Vipps MobilePay Login (Norway)

- MitID Erhverv (Danish business employee identity)

- Dutch iDIN (via Dutch banks)

Pricing

- Monthly platform fee + per-verification transaction fee (varies by eID)

- Free test account; unlimited test logins at no cost

- BankID Sweden: from 0.10 DKK per verification + subscription

#3 ID.me

4.1 Average Score · (4.4 G2 | 4.0 Trustpilot)

Website: www.id.me

ID.me is a US-based digital identity network founded in 2010. It is the closest equivalent in the American market to what national eIDs like BankID and MitID provide in Europe: a reusable, trusted digital identity credential that users verify once and then carry with them across multiple organizations and services without re-verifying.

ID.me’s network is extensive: over 156 million verified users, integrations at 21 federal agencies, 50 state government agencies, and more than 70 healthcare organizations.

Best for: US-focused organizations (particularly government agencies, healthcare providers, and financial services firms) that need federally accredited identity proofing solutions.

How The Digital Wallet Flow Works

- Stores Legal ID, Employee ID, Veteran ID, community, and group-based credentials

- Verify once and allow your users to be recognized across all ID.me-integrated organizations

- Users never re-verify their identity across any participating service

- Multi-Factor Authentication (MFA) protection on the wallet

The core concept of ID.me is its identity wallet. Once a user has been verified through ID.me (using a combination of document checks, biometric video selfie, SSN cross-check, and mobile network operator (MNO) data) that verification is stored in a portable wallet. The user can then authenticate into any ID.me-integrated service by presenting their wallet, without going through the full verification process again.

Other Offered Services

- US driver’s license, state ID, passport, or passport card cross-checked against issuing databases

- Social Security Number (SSN) validation

- Mobile network operator (MNO) data cross-check

- Biometric video selfie with liveness detection

- Trusted Referee option: live video call for users who cannot complete automated proofing

Compliance

- NIST 800-63-3 IAL2 / AAL2 certified

- Federally approved for US government and state agency use

- Trusted by the IRS, the Department of Veterans Affairs, and state unemployment agencies

Pricing

- Enterprise pricing (contact sales)

#4 Microblink

3.8 Average Score (based on product reviews and analyst coverage)

Website: www.microblink.com

Microblink is a New York-based AI and computer vision company whose core products (like BlinkID, BlinkID Verify, and the Microblink Platform) are primarily focused on identity document scanning, extraction, and verification. Microblink’s strength is document intelligence: its AI models have processed over 12 billion identity documents from 180+ countries and are widely used as an underlying technology layer by many leading identity verification platforms globally.

In the context of eID verification, Microblink’s relevance comes through its eIDV (Electronic Identity Verification) and PII data validation capabilities within the Microblink Platform. After extracting and verifying a document, the platform can cross-check the extracted identity data against authoritative databases and watchlists, performing what is sometimes called “soft” eIDV or database-based identity verification.

Note: This is distinct from the redirect-based national eID flows (like BankID or MitID), but it achieves a similar goal: cross-matching a person’s identity data against external trusted sources to confirm it is real and consistent. Microblink does not natively support redirect-based national eID flows such as BankID or Smart-ID.

Best for: Technology companies and identity platform builders that need a best-in-class ID document scanning and database-matching engine.

Relevant Features

Database Cross-Matching (via Microblink)

- PII data validation: cross-checks extracted document data against authoritative databases

- Sanctions, PEP, and adverse media screening

- Real-time watchlist checks integrated into the verification workflow

- Automated Data Matching: cross-compares MRZ, VIZ, and barcode data for consistency

Document-Based Identity Verification

- 2,500+ supported ID types from 180+ countries

- Fully automated: screen detection, photocopy detection, AAMVA barcode analysis, VIZ/MRZ cross-checks

- iBeta Level 2 Presentation Attack Detection (PAD)

- Injection Attack Detection (IAD)

- Real-time face matching and anti-spoofing

Workflow and Integration

- No-code drag-and-drop workflow builder with pre-built compliance templates

- Cloud API and self-hosted options

- Available on Google Cloud Marketplace

- ISO/IEC 27001 and ISO/IEC 27701 certified

Pricing

- Custom enterprise pricing (contact sales)

#5 Scrive

3.9 Average Score · (4.4 Capterra | 3.7 G2)

Website: www.scrive.com

Scrive is a Stockholm-based Qualified Trust Service Provider (QTSP) under EU eIDAS, primarily known as an electronic signature platform. Its eID Hub is the identity verification product within Scrive’s broader suite, a single-API hub that provides access to national eID schemes for onboarding, authentication, KYC compliance, and e-signing.

Where Scrive differentiates itself most is in its signing use case: because Scrive is a QTSP, eID authentication performed through its platform can be directly combined with Qualified Electronic Signatures (QES), which is the highest level of legally binding signature under eIDAS.

Best for: European enterprises and regulated businesses that need to combine eID-based identity verification with legally binding electronic signatures.

How the Flow Works

- User authenticates with their national eID provider via Scrive’s eID Hub

- No document upload required; the identity is confirmed at the source

- Verified legal name, national ID number, and address (where supported) are returned

- Authentication evidence is stored and can be attached to signed documents

Supported eID Providers

Scrive’s eID coverage is strongest in the Nordic regions, where it is a certified broker for Swedish BankID, Norwegian BankID, Danish MitID, Smart-ID, and FTN. It also supports Belgian itsme® and British OneID. In the Scrive model, businesses sign one contract and get access to all supported eIDs through a single API, which means no individual agreements with eID providers are required.

Pricing

- Subscription-based (contact sales for enterprise pricing)

- Free 14-day trial for the eSign platform

Comparison

Feature |

iDenfy |

IDURA |

ID.me |

Microblink |

Scrive |

BankID (Sweden/Norway) |

✅ |

✅ |

❌ |

❌ |

✅ |

MitID (Denmark) |

✅ |

✅ |

❌ |

❌ |

✅ |

Smart-ID (Baltics) |

✅ |

❌ |

❌ |

❌ |

✅ |

SPID (Italy) |

✅ |

❌ |

❌ |

❌ |

❌ |

CLEAR (North America) |

✅ |

❌ |

❌ |

❌ |

❌ |

OneID (UK) |

✅ |

❌ |

❌ |

❌ |

✅ |

Verimi (Germany) |

✅ |

❌ |

❌ |

❌ |

✅ |

FTN (Finland) |

✅ |

✅ |

❌ |

❌ |

✅ |

US Digital Identity Network |

❌ |

❌ |

✅ |

❌ |

❌ |

Reusable Credential Wallet |

❌ |

Partial (pseudonym) |

✅ |

❌ |

❌ |

Qualified eSignature (QES) |

❌ |

✅ (via eIDs) |

❌ |

❌ |

✅ (QTSP) |

AML Screening |

✅ Full |

❌ Native |

✅ |

✅ |

✅ AML-compliant |

Single Integration, Multi-eID |

✅ |

✅ |

N/A |

❌ |

✅ |

Pricing Model |

Pay per success |

Monthly + per-verification |

Enterprise |

Enterprise |

Subscription |

Primary Market |

Global (EU + US) |

Nordics, Europe |

United States |

Global (doc-based) |

Europe (Nordics) |

Final Thoughts

The right eID verification software depends almost entirely on where your users are and what you need to do with their verified identity. For example, if your business serves users across multiple European markets and/or the US, you need the widest possible eID provider coverage from a single vendor. In this case, iDenfy is the strongest choice.

However, if you need to combine eID verification with legally binding electronic signatures in a single, eIDAS-compliant workflow, then Scrive is your best choice. So, once again, all the dots can be connected only when you know your concrete use case and analyze the best options in the market.

Still not sure what to pick? Book a free demo with our experts, and they’ll give you a quick tour of iDenfy’s dashboard.

DISCLAIMER

The information presented has been compiled from publicly available sources. It does not represent a final assessment, endorsement, or opinion. While we aim to keep the content accurate and up-to-date, certain details might change over time. If you notice any missing details, please contact the website owner.