The financial world is changing, and it is not the same as it was yesterday, so yes, we could say that it is changing every day. On one hand, technology has allowed banks to process millions of transactions every day at lightning speed; on the other, it has exposed them to various fraud risks, which is why banks need fraud detection tools. Synthetic identity fraud and phishing scams mean that fraudsters are using various tactics and technologies to bypass banking systems and their security measures just to profit. For banks, it is a lot more than just a financial issue. It is a matter of trust as well.

AI is powerful against fraud. Its ability to learn from data, identify patterns, and make real-time decisions allows financial institutions to keep user accounts secure.

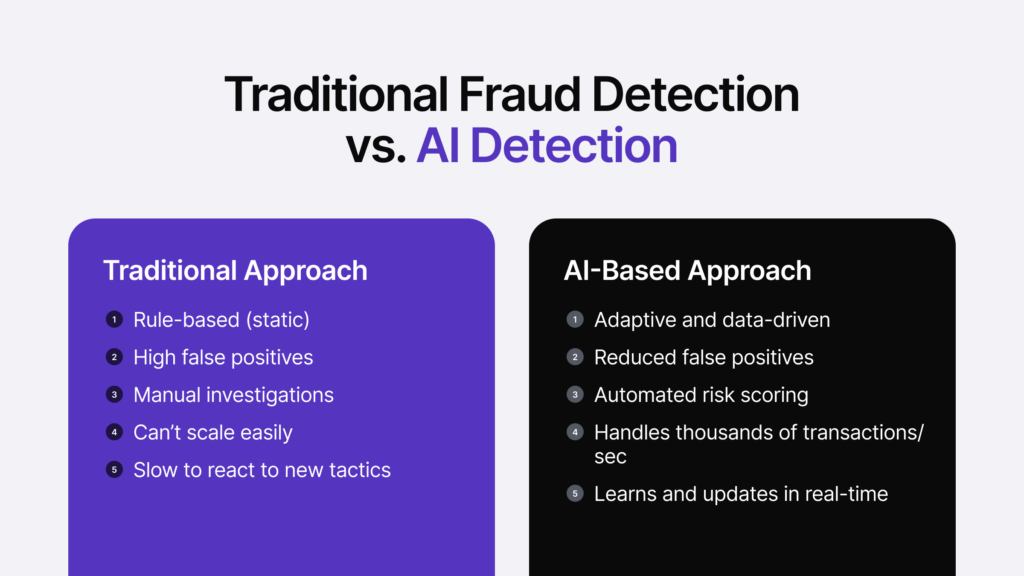

Why Traditional Systems No Longer Work

Traditional fraud detection methods almost always rely heavily on rules and manual processes, like:

- Transactions over a certain amount might trigger alerts.

- Transfers from specific locations could also be alerted to the team.

- Known blacklisted accounts or IPs are automatically blocked.

Well, yes, you can say that these rules offer protection against fraud, but it is not as effective as AI could be, because these traditional rules almost always run short when fraudsters decide to change their tactics.

The thing with these traditional methods is that they can not adapt in real-time, which often results in a high number of false positives, and they can not keep up with the volume of today’s digital banking activity.

Verification built for fintech

From neobanks to payment platforms — see how iDenfy helps fintech companies automate KYC and stay compliant.

Explore Fintech SolutionConsider The Implementation of AI

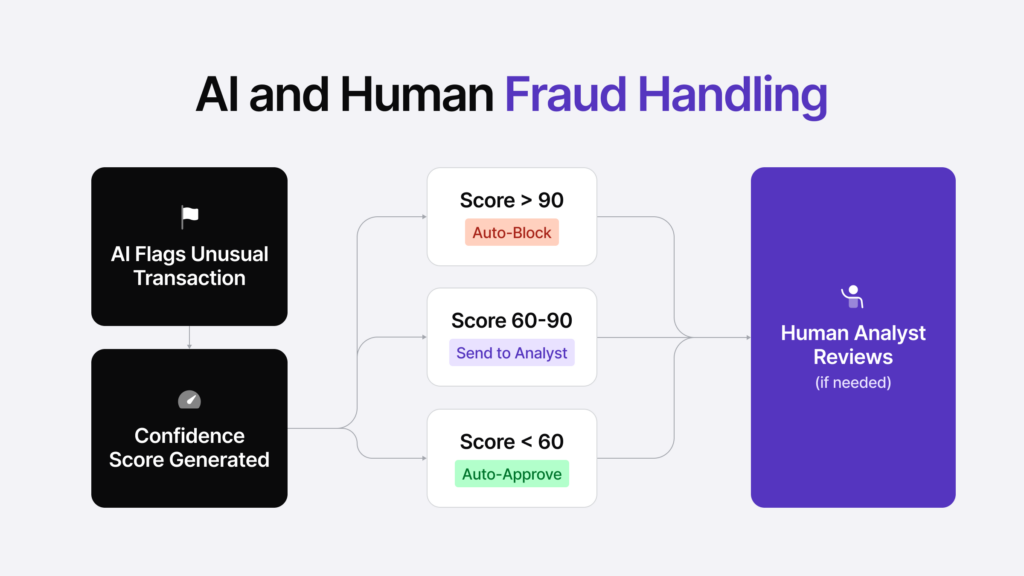

If you are still using traditional systems as your primary security for the bank, well, we hate to break it to you, but the bank could be in real danger. AI brings something that traditional systems lack: adaptability.

Instead of depending on predefined rules, AI systems learn what constitutes “normal” behavior and continuously update their understanding as new data comes in. When something deviates from the norm, the system flags it, and then the human agent takes over for the investigation of the issue that occurred.

AI does this:

- Real-Time Monitoring: AI can analyze thousands and thousands of transactions in minutes, and if any unusual activity or transaction occurs, it instantly gets alerted to the human team.

- Pattern Recognition: Machine learning models can identify simple and complex patterns that humans or traditional software would just simply miss.

- Behavioral Analysis: AI systems track user behavior, such as login patterns and device usage. Additionally, mouse movement and typing speed can also be monitored. Sudden changes could indicate fraud.

Main Technologies That Are Used in Fraud Detection (AI)

There is not just one type of AI. Several technologies work together to make fraud detection way smarter and faster:

- Machine learning: Trained on historical data, so it improves the more it processes. Unusual locations, transaction timing, amounts, merchant categories – patterns that would take an analyst time to piece together get picked up automatically, and the model gets sharper with every case.

- Deep learning: Extends what machine learning can do by using neural networks to get closer to human-style reasoning. Where it earns its place is in reading sequences – a series of transactions that looks unremarkable individually but tells a different story together.

- Natural language processing: Handles the unstructured stuff: emails, chat logs, support tickets. Fraud doesn’t always show up in transaction data. Phishing attempts and social engineering often leave traces in communication channels that purely numerical analysis would never reach.

- Anomaly detection: Doesn’t need labeled examples of fraud to work. It watches for anything that falls outside normal behavior, which means it can flag something suspicious even when there’s no prior case that matches it.

- Behavioral biometrics: Builds a profile of how each user normally operates: when they log in, what device they use, how they type, and how they move a mouse. A sudden shift from that profile raises a flag – even when the transaction itself gives no obvious reason for concern.

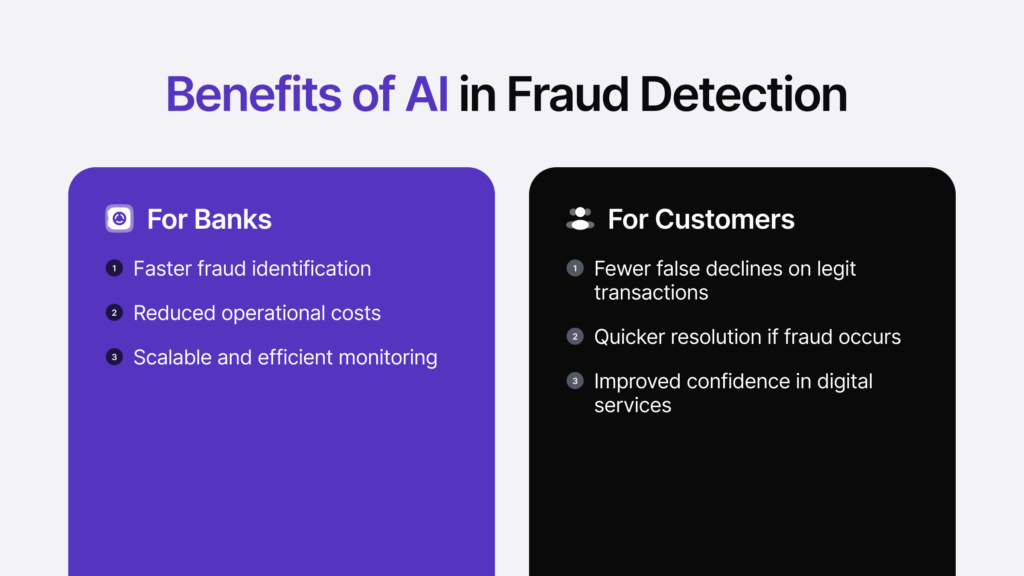

Benefits for Banks and Users

If you thought that AI only does safety things, well, you are right, but it also does more than that – it gives benefits for banks and their users as well. Let’s talk about it.

- Fewer false positives mean legitimate transactions go through without being held up – less friction for users who’ve done nothing wrong

- When fraud gets caught quickly and accurately, resolution moves faster – affected users get their money back sooner, and the bank spends less time managing the fallout

- Routine tasks that used to sit in an analyst’s queue run automatically, leaving the team free for work that actually needs a human

- Less fraud means fewer chargebacks and lower operational costs across the board

Ethical Concerns

AI in fraud detection comes with real tradeoffs worth acknowledging.

Data privacy: These systems run on large volumes of personal and financial data. Collecting, storing, and processing that data in line with GDPR, CCPA, and equivalent regulations isn’t optional – and getting it wrong carries serious consequences.

Bias and fairness: A model is only as fair as the data it was trained on. If that data reflects historical biases – and it often does – the model carries them forward. Certain demographics end up flagged more often or treated less favorably, not because of anything they’ve actually done, but because of patterns baked into the training set.

Explainability: Deep learning models, in particular, are difficult to interrogate. When a decision is made – a transaction blocked, an account flagged – regulators and users increasingly want to know why. That’s a reasonable expectation, and one that black-box models often can’t meet.

Fraudster Evolution: The irony is that criminals are using AI themselves to make better attacks, leading everybody to the technological arms race, so as AI gets smarter, so do criminals.

The Future

AI is just getting started in the banking sector, but various forecasts are available, and in the next few years, we are likely to see these innovations:

Federated Learning: Allows banks to collaborate and train shared models without risking sensitive user data.

Explainable AI (XAI): New tools are being created to make AI decisions more transparent.

Deeper Integration With Blockchain: Smart contracts could automate security checks and make fraud nearly impossible.

Collaboration Across Institutions: With AI, various platforms that share anonymized fraud data to improve the defense against fraud collectively.

Conclusion

Fraud detection used to mean catching problems after they’d already happened. That’s changed. Banks can now spot and stop fraud before it causes damage, protect data, and secure accounts against threats that keep shifting.

The other side of that is that fraud tactics move just as fast as the technology built to counter them. There’s no finish line – just the need to keep pace, and to do it together.