France has long positioned itself as one of the more crypto-forward countries in Europe. While other EU member states were still debating how to approach digital assets, France was already building a dedicated regulatory framework. That ambition gave birth to the PSAN requirements – and for crypto firms operating in the country, understanding what it demands is no longer optional.

If you are running a crypto exchange, offering custody services, or building a platform that converts digital assets to fiat, the PSAN requirements framework directly impacts how your business operates.

What Is a PSAN, Exactly?

PSAN stands for Prestataire de Services sur Actifs Numériques – or Digital Asset Service Provider in English. The status was created under France’s PACTE Law of 2019, making France one of the first EU countries to establish a formal licensing framework for crypto businesses.

Since January 1, 2020, any company looking to offer the following services must register with the Autorité des Marchés Financiers (AMF) – France’s financial markets authority:

- Purchase and sale of crypto assets against legal tender

- Custody of digital assets on behalf of clients

- Trading of digital assets for other digital assets

- Operation of a crypto trading platform

Operating without registration is not just risky from a reputational standpoint; it also carries criminal penalties of up to 2 years in prison and fines of up to €30,000.

By late 2025, roughly 117 PSANs were registered with the AMF. That number might sound manageable, but it is only a fraction of total applications – the AMF rejects or pushes back on many filings, which says a lot about how seriously it takes the review process.

KYC for crypto and blockchain

Stay compliant with evolving crypto regulations. iDenfy helps exchanges and DeFi platforms verify users globally.

Explore Crypto SolutionThe Two-Tier Registration Structure

One thing that often catches firms off guard is that registration under the PSAN requirements is not a single-tier process. There are two distinct levels, and understanding the difference matters.

Simple registration was the original entry point – a lighter-touch process for firms that applied before certain transition deadlines. Companies that obtained simple registration before January 1, 2024, are grandfathered under those original rules. However, this path is now effectively closed for new applicants.

Enhanced registration (enregistrement renforcé) became mandatory from January 1, 2024, for any new provider wanting to offer the four core digital asset services: custody, crypto-to-fiat exchange, crypto-to-crypto trading, and operation of a trading platform. Enhanced registration aligns with MiCA requirements and comes with significantly more demanding compliance obligations.

There is also an optional licensing tier (agrément), which goes beyond enhanced registration. Licensed DASPs must maintain either professional indemnity insurance or a minimum level of own funds, have higher capital buffers depending on the services offered, and demonstrate stronger governance frameworks. The trade-off? Licensed status positions a firm as a more credible market player and smooths the path to MiCA authorization.

Related: [Understanding KYC and MiCA]

Core Compliance Obligations Under the PSAN Framework

What does it actually take to meet PSAN requirements?

AML/CFT Compliance

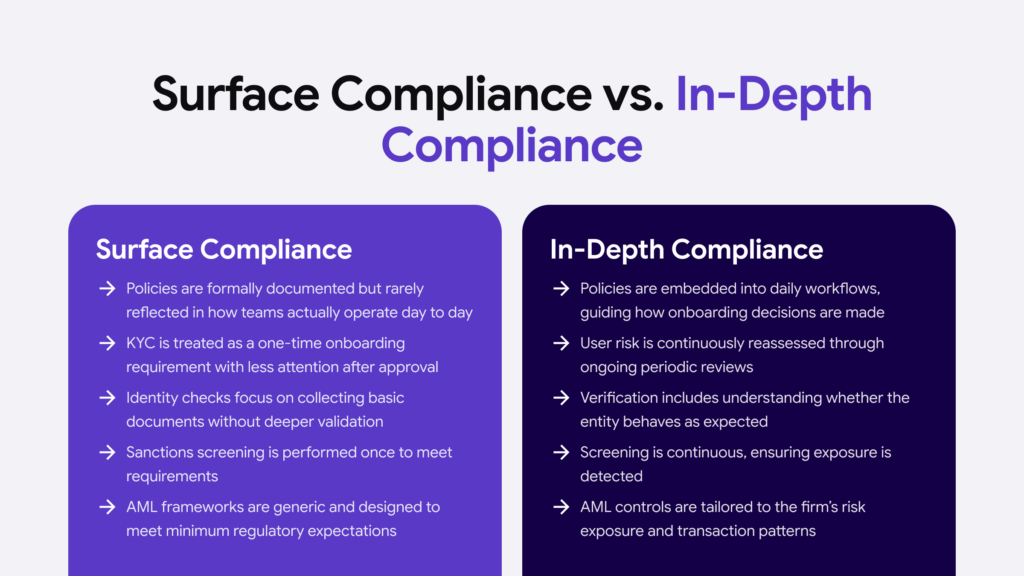

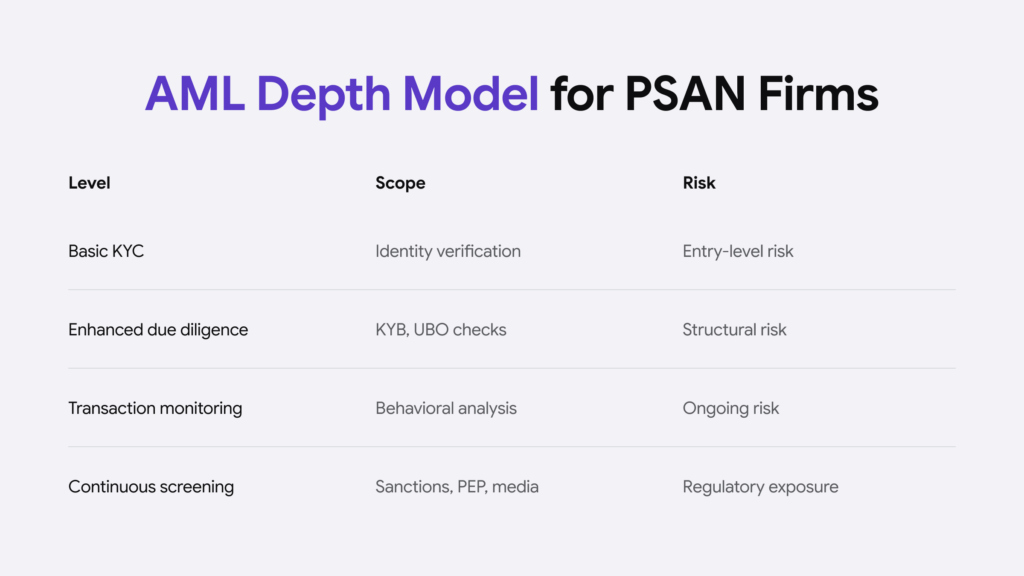

Anti-money laundering and counter-terrorism financing (AML/CFT) obligations are at the heart of PSAN registration. French PSANs must implement robust KYC procedures for all customers, conduct ongoing transaction monitoring, and report suspicious activity to TRACFIN – France’s financial intelligence unit.

This is where many firms underestimate the workload. AML obligations do not stop at onboarding. They require continuous screening against sanctions lists, politically exposed persons (PEP) databases, and adverse media – a level of ongoing vigilance that demands both the right tooling and internal processes to back it up.

Firms dealing with institutional clients or corporate counterparties face an additional layer of scrutiny. KYB verification – the process of validating the legal identity, ownership structure, and beneficial ownership of business clients – is increasingly expected as part of enhanced due diligence. For any crypto platform onboarding other companies, exchanges, or investment vehicles, skipping this step creates serious regulatory exposure.

Cybersecurity Requirements

The AMF published dedicated cybersecurity requirements for DASPs through Instruction DOC-2019-24, later updated to reflect tightened registration standards. These cover data protection, system resilience, incident response, and access controls.

Cybersecurity doesn’t always top the list when compliance teams are pulling together a PSAN application, but it carries real weight in what the AMF actually evaluates. The regulator wants to see that firms have genuinely thought through how they protect client assets and data — not just documented it.

Governance and Fit-and-Proper Tests

The AMF pays close attention to the people at the top. Key officers and board members go through fit-and-proper assessments covering professional background, qualifications, and track record. Firms with complicated ownership structures or anything less than full clarity on beneficial ownership tend to spend a lot of time going back and forth with the regulator before the application gets anywhere.

Financial Resources

Capital requirements vary depending on which services a firm offers and whether it pursues enhanced registration or full licensing. At a minimum, there must be sufficient own funds to cover operational risks and, for licensed DASPs, either professional indemnity insurance or a prescribed capital floor.

PSAN and the MiCA Transition

Here’s where things get particularly important for 2025 and 2026. The EU’s Markets in Crypto-Assets (MiCA) regulation became fully applicable across all member states on December 30, 2024. With that, MiCA effectively replaced the national PSAN requirements regime as the primary authorization framework for new crypto service providers in France.

New providers entering the French market can no longer apply for registration under the PSAN requirements; they must seek authorization directly as a Crypto-Asset Service Provider (CASP) under MiCA.

For existing PSANs registered or authorized before December 30, 2024, France established an 18-month transitional period. These firms can continue operating under their existing PSAN status until July 1, 2026, or until they receive (or are refused) MiCA authorization – whichever comes first. Crucially, during this period, firms are limited to the service scope originally approved under their PSAN requirements registration.

The case for pursuing MiCA authorization is straightforward: approved CASPs get EU passporting rights, meaning they can operate across all 27 member states without going through separate national licensing processes. For French crypto firms with European ambitions, that’s a strong reason to move early rather than wait.

Three to six months is a realistic timeline for most firms, though that assumes the compliance documentation is already in reasonable shape. The July 1, 2026, deadline doesn’t leave much room – if there’s no migration plan in place yet, the clock is already running.

What Gets Applications Rejected?

The AMF’s rigorous review process means many applications do not make it through on the first attempt. The most common failure points include:

- Incomplete AML/CFT documentation. Vague policies that don’t describe actual procedures in detail are a red flag. The AMF wants to understand precisely how a firm identifies its customers, screens for risks, monitors transactions, and escalates concerns.

- Unclear beneficial ownership. Firms that can’t clearly demonstrate who ultimately owns and controls the business – down to ultimate beneficial owners (UBOs) holding 25% or more – tend to face significant pushback. This is particularly true for firms with multi-layered corporate structures or international parent companies.

- Inadequate cybersecurity governance. Submitting a generic IT security policy without evidence of actual implementation rarely passes muster.

- Weak financial projections. The AMF looks at whether a firm’s capital base is proportionate to its intended activities. Underestimating operating costs or overstating revenue projections in the business plan raises questions about viability.

Preparing for What Comes Next

For crypto firms operating in or entering the French market, the message is clear: compliance is not a checkbox. The PSAN requirements framework – and now MiCA – demands that AML programs, identity verification processes, and governance structures are genuinely fit for purpose, not just technically present.

Firms that built strong compliance foundations under PSAN will find the MiCA transition far more manageable. Those who treated registration as a formality are likely to find the coming months uncomfortable.

Conclusion

The shift from a national licensing regime to an EU-wide one also changes the competitive landscape. With passporting rights on the table, French PSANs that successfully complete MiCA authorization won’t just be compliant – they’ll be positioned to scale across the entire European single market.

That is a significant prize. But it requires investing in compliance infrastructure that can hold up under observation, not just today, but as regulatory expectations continue to evolve.