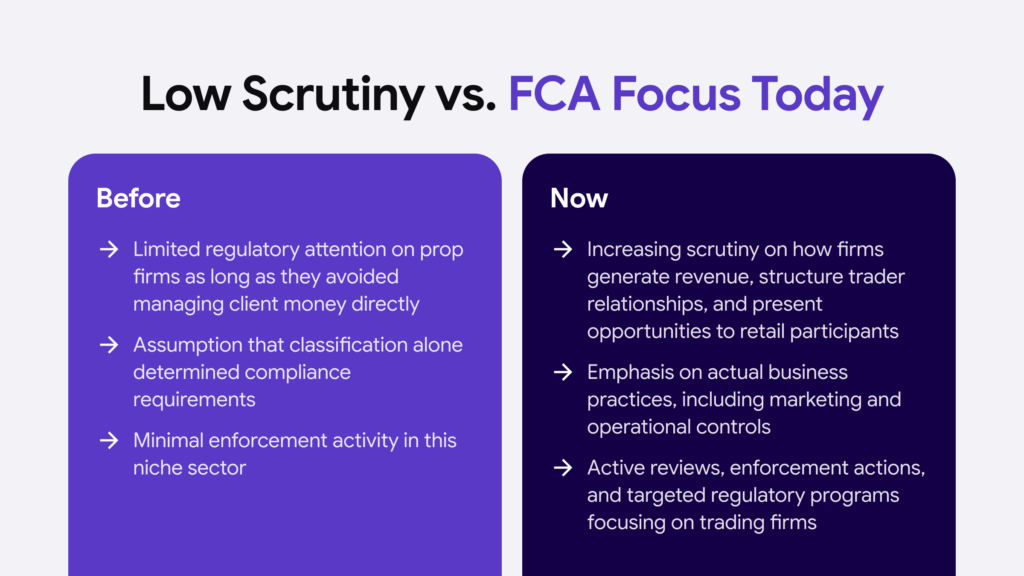

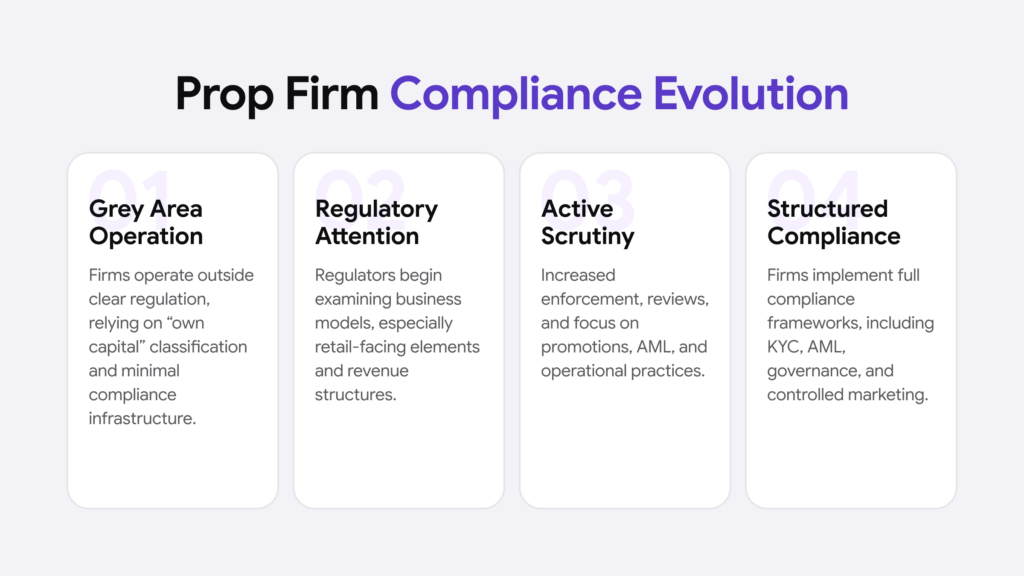

The prop trading industry has had an unusually long run operating in a regulatory grey area. For most of the FCA regulation’s existence, the model was simple enough that it sat comfortably outside the boundaries of what financial regulators focused on: a firm trades its own capital, takes its own risk, and doesn’t manage client money. No client money, no regulation – roughly speaking.

That framing is getting harder to sustain.

The retail evaluation model – where traders pay a fee to take a challenge, pass to access a funded account, and split profits with the firm – has blurred the lines enough that regulators are paying close attention. In the UK, the FCA’s scrutiny has been building for the past two years. Understanding where the regulatory lines actually sit in 2026, and where they’re heading, matters if you’re running one of these businesses or planning to.

Where Prop Firms Currently Stand Under FCA Rules

The starting point is the legal distinction that most of the industry has operated on: a firm trading its own proprietary capital is not, in the FCA’s traditional framing, conducting regulated investment activities. Investment firms that manage client money require FCA authorization. Prop firms that trade exclusively with their own funds generally do not.

That distinction remains valid for traditional institutional prop shops – firms where the firm itself takes on the risk, and the traders are employees. The picture gets significantly murkier for the retail evaluation model, and that’s where most of the regulatory attention is now focused.

When a retail prop firm:

- collects fees from traders to participate in funded account challenges

- makes financial promotions promising traders access to capital and profit splits

- operates in ways that could be interpreted as managing or intermediating trader funds

…the question of whether these activities fall within the FCA’s regulatory perimeter becomes a lot less clear-cut. The FCA has not issued definitive guidance specifically targeting retail prop firms, but it has made clear through its broader supervisory activity and enforcement actions that it will pursue firms whose business model crosses the line into regulated territory without authorization.

In August 2025, the FCA conducted a multi-firm review specifically assessing algorithmic trading controls among principal trading firms. The focus included risk management frameworks and whether firms’ internal controls were adequate for the activities they were conducting. The message was clear: the FCA is watching how firms actually operate, not just how they classify themselves.

Automate your KYC process

iDenfy verifies customers from 200+ countries in seconds. AI-powered, compliant, and trusted by 1,000+ companies.

Explore KYC SolutionFinancial Promotions

For prop firms operating in the UK, financial promotions rules are currently the most direct and immediate regulatory exposure.

Under the Financial Services and Markets Act 2000, any financial promotion must either be issued by an FCA-authorized firm or approved by one. This applies regardless of whether the firm itself needs FCA authorization – and the FCA has been aggressive about enforcement here. Between 2023 and 2025, the FCA removed or amended thousands of financial promotions, including a significant number targeting retail traders with claims about funded accounts, challenge programs, and profit-sharing arrangements.

The risk isn’t abstract. Prop firms that market their services using claims about trading returns, implied performance outcomes, or the value of funded account opportunities – without either being FCA-authorized or having promotions approved by an authorized firm – are operating in direct breach of Section 21 of FSMA. Penalties include unlimited fines and criminal liability for individuals involved.

The FCA’s 2026/27 work program explicitly includes continued action against financial influencers and financial promotions that mislead retail consumers, and prop trading is squarely in the frame for this.

AML Obligations: Who They Apply to and Why They Matter

Anti-money laundering obligations in the UK are set out in the Money Laundering Regulations (MLRs), which apply to firms in specific sectors regardless of their FCA authorization status.

For prop trading firms, the critical question is whether their activities bring them within the scope of the MLRs. Firms conducting certain financial activities – particularly payment services or currency exchange – may find themselves in scope even where they lack FCA authorization for investment activities. Firms that have sought and obtained FCA authorization for any regulated activity are subject to the full suite of MLR obligations.

Where AML obligations do apply, the requirements are substantive:

- User due diligence on all clients, including identity verification, before establishing a business relationship

- Enhanced due diligence for higher-risk users, including PEPs and clients from high-risk jurisdictions

- Ongoing transaction monitoring and suspicious activity reporting to the National Crime Agency

- Appointment of a qualified Money Laundering Reporting Officer

KYC verification isn’t just a compliance box for firms in scope – the FCA issued over £1.07 billion in AML-related fines between 2015 and 2025, and fintechs and newer financial services firms are no longer given the benefit of growth-phase leniency. The pattern from the last two years of enforcement is clear: the FCA will pursue smaller and newer firms just as readily as established institutions.

Even for prop firms that assess themselves as currently outside MLR scope, the direction of regulatory travel makes building AML-compliant infrastructure early a sensible position. The FCA’s 2026/27 work program notes explicit plans to explore more proportionate KYC approaches for smaller transactions – which signals regulatory maturation rather than deregulation. The bar is being calibrated, not lowered.

The Consumer Duty Dimension

One development that often gets missed in prop trading compliance discussions is the Consumer Duty, which came into force for all FCA-regulated firms in July 2023 and has been embedded in FCA supervisory expectations since.

Consumer Duty doesn’t directly apply to unregulated prop firms – but it shapes how the FCA thinks about the sector and what it looks for when it does have jurisdiction. The core obligation requires that authorized firms act to deliver good outcomes for retail customers: fair pricing, clear communications, products that serve genuine customer needs, and appropriate support.

For prop firms whose evaluation products target retail traders – often people with limited trading experience who pay significant upfront fees for challenges that most will fail – the Consumer Duty framework creates an obvious reference point for what regulatory intervention could look like if these businesses are eventually brought within the FCA’s scope.

Several firms have proactively restructured their product disclosures and challenge terms in response to this expectation. Whether they needed to or not, it reflects a sensible read of where regulatory momentum is heading.

What Full FCA Authorization Actually Involves

Some prop trading businesses have chosen to seek FCA authorization – either because their activities require it or because they see authorization as a commercial and reputational asset. It’s worth understanding what that involves.

FCA authorization is not a single status. Firms apply for specific permissions depending on the regulated activities they want to conduct. For a prop trading firm that wants to deal in investments as principal, the relevant permission is under Article 14 of the Regulated Activities Order. Firms that also want to arrange deals or transmit orders need additional permissions.

The authorization process involves demonstrating to the FCA that:

- The firm has adequate financial resources for the activities it wants to conduct

- Senior management and beneficial owners are fit and proper – no relevant criminal convictions, no history of financial regulatory breaches, demonstrable competence for their roles

- The firm has effective systems and controls for risk management, compliance, and financial crime prevention

- Client assets (where relevant) will be properly safeguarded

The threshold conditions for authorization are significant enough that many firms underestimate the preparation required. Applications that arrive without properly documented governance frameworks, adequate financial projections, or clear evidence of AML controls tend to generate extended back-and-forth with the FCA or outright rejection.

Conclusion

The prop trading industry is not facing imminent blanket regulation in the UK – but the conditions for it are assembling. The FCA has the tools, the enforcement appetite, and the regulatory mandate. What it hasn’t done yet is issue sector-specific rules for retail evaluation prop firms. When it does, firms that have been operating without any compliance infrastructure will find the transition painful.

The firms navigating this period well are the ones that have taken a clear-eyed look at their actual activities rather than relying on how they prefer to classify themselves. They’ve asked: do our financial promotions comply with Section 21? Does our business model bring us within MLR scope? If we were scrutinized tomorrow, would our AML controls and KYC documentation hold up?

These aren’t abstract questions. They’re the ones the FCA is already asking, through multi-firm reviews, enforcement actions, and a work program that explicitly names financial promotions and AML controls as 2026 priorities.

The prop trading grey area is getting smaller. The time to build compliance infrastructure is before the formal rules arrive, not after.