The gig economy runs on trust between strangers, for example, a passenger gets into a car with someone they have never met, a homeowner hands over their keys to a guest found online, a business wires a payment to a freelancer on the other side of the world based on a profile picture and a few reviews – this is KYC for the gig economy and online marketplaces.

Most of the time, that trust holds, but the fraud numbers tell a different story about how often it does not – and about how not prepared most platforms are to address it before something goes wrong.

Over 25% of people using a gig economy platform will experience fraud or identity theft, according to several websites, a rate double that outside these marketplaces. In the mobility and gig sector, specifically, the 2025 Fraud Report recorded a 21% year-over-year increase in fraudulent activity, with over 90% of it driven by impersonation – fraudsters using stolen or fake identities to gain access to platforms they would otherwise be rejected from.

These cases are the predictable result of platforms that scaled fast and treated identity verification as a speed bump rather than a foundation.

Gig Platforms Are a Target?

The same things that make gig platforms appealing to workers and customers make them appealing to fraudsters: low barriers to entry, high transaction volumes, and a model that operates mostly remotely.

A fraudster who gets a verified account on a ride-sharing platform can use it to run scams, collect payments fraudulently, or sell the account on dark web marketplaces – verified Uber accounts have been documented for sale at around $5. Freelance platforms have been documented as venues for account selling and renting, where a verified profile built by one person gets used by someone else entirely. The platform has done its verification once. After that, it assumes the account user is the same person who created it.

On the buyer side of marketplaces, the risks are different but just as real. Fake orders, payment fraud, chargebacks after services are rendered, and accounts created with stolen credentials are standard tools for organized fraud operations targeting marketplace platforms.

What makes all of this harder is volume. Platforms processing millions of transactions can not manually review each one, which is exactly why investing in the right infrastructure from the start matters more than bolting it on after a fraud wave hits.

Trusted transactions, verified buyers

Reduce chargebacks and fraud with age and identity verification built for e-commerce platforms.

Explore E-Commerce SolutionWhat KYC Means for Marketplace Platforms

Most gig platforms do not think of themselves as financial institutions, and for a long time, they could operate without the compliance obligations that come with that label. That is changing.

As these platforms have expanded into payment processing, digital wallets, and embedded financial services, the regulatory perimeter has expanded with them. Under the EU’s upcoming AMLR framework and PSD3 – expected to come into force in 2027 – digital marketplaces facilitating payments will need to comply with AML and KYC obligations in a much more formal sense. Even before those changes land, platforms operating in regulated markets are already subject to AML requirements if they process payments above certain thresholds or act as intermediaries between buyers and sellers.

But even for platforms that are not technically classified as obliged entities under financial regulations, there is a practical case for KYC that has nothing to do with regulatory risk. Identity fraud costs money, damages trust, and once that trust erodes, it is hard to rebuild – users who have been defrauded on a platform do not always come back.

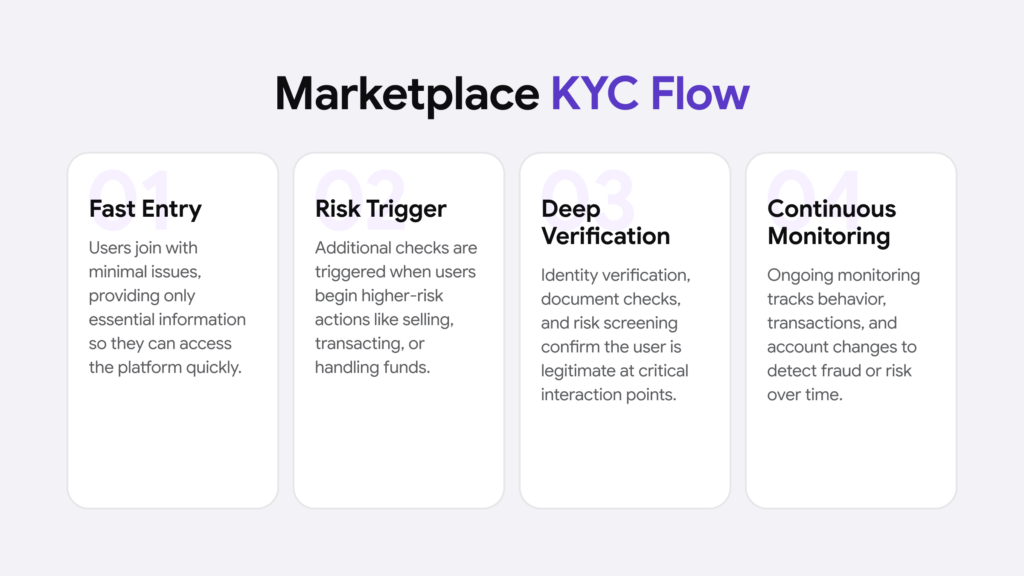

KYC verification in the gig economy context covers a few distinct obligations depending on the platform model:

- Worker/seller verification – confirming that the person onboarding as a driver, freelancer, or service provider is who they claim to be

- Buyer/customer verification – confirming that the person making bookings or payments is a legitimate account holder, not a fraudster with stolen credentials

- Ongoing monitoring – watching for account takeovers, unusual transaction patterns, and behavior that suggests the person using an account is no longer the person who created it

The degree of rigor required at each of these stages depends on the platform and what it is facilitating. A food delivery platform has different risk exposure than a peer-to-peer payment marketplace. But the baseline expectation – that you know who is on your platform – is consistent across all of them.

Fraud Patterns to Watch

The fraud gig platforms face is not random. It follows patterns that a well-designed verification and monitoring stack can catch, if the platform is built to look for them.

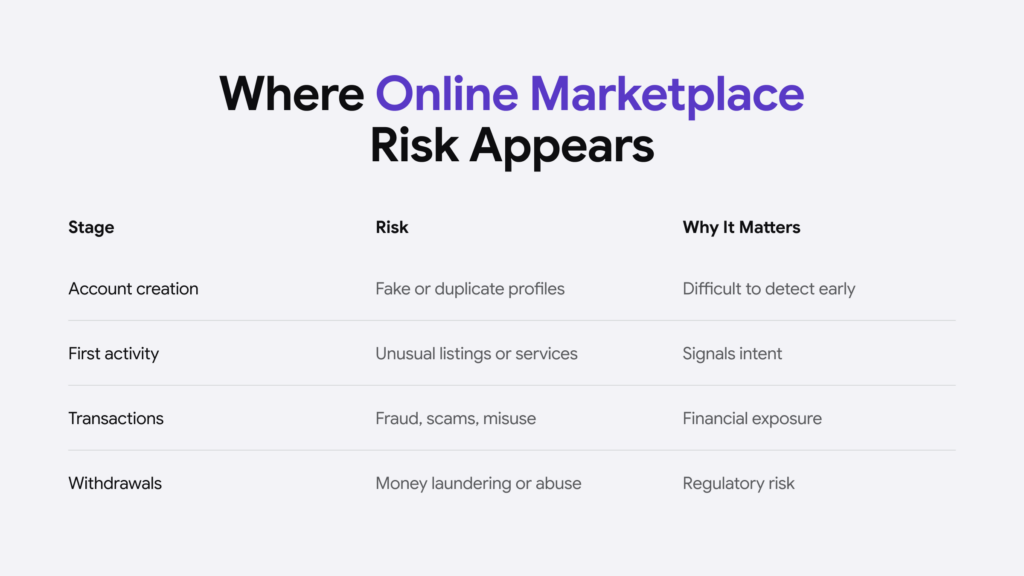

Identity fraud at onboarding

Someone creates an account using a stolen or synthetic identity – real personal data combined with a fabricated or generated face. They pass a basic document check because the document is real. They fail a biometric check because their face does not match. This is exactly why document-only verification is not sufficient, and why liveness detection matters.

Account takeover

A legitimate account gets compromised through credential stuffing or phishing, and a fraudster takes over. The platform’s records show a verified user, but in practice, that user is someone else, as continuous monitoring that flags unusual behavior – new device, different location, changed payout details – is the control that catches this after the fact.

Profile misrepresentation

A freelancer or gig worker presents qualifications, credentials, or a work history they do not actually have – on professional platforms, this often coexists with account sharing or renting – a verified account with a strong track record gets sold to someone who could not build one on their own, periodic re-verification is the mechanism that addresses this, but few platforms have implemented it at scale.

Payout fraud

Fraudsters complete work and redirect payments to accounts they control using stolen financial details. Or they use a legitimate account to receive payments for services never delivered. Tying payouts to verified identities and monitoring for unusual payout patterns closes most of this.

Building a Compliance Framework That Fits

Gig economy KYC is not a one-size-fits-all problem – the right approach for a freelance marketplace looks different from the right approach for a ride-sharing platform, which looks different again from a peer-to-peer marketplace facilitating high-value transactions.

A few principles that hold across most of them:

Verify at onboarding, but do not stop there

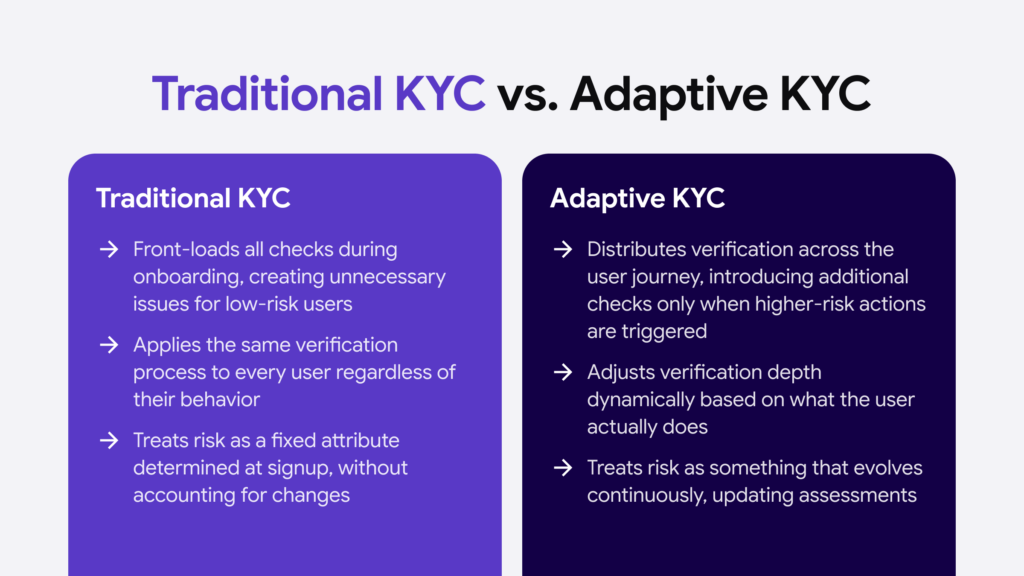

A one-time identity check at sign-up is table stakes, catching some fraud. It does not catch account takeovers, profile sharing, or the gradual drift that happens when a legitimate account gets used for illegitimate purposes, as platforms that are taking fraud seriously treat identity as something that gets reconfirmed periodically, or when behavior suggests something has changed.

Match the level of friction to the level of risk

Not every user needs full biometric verification. A customer placing a first order on a food delivery platform has different risk exposure than a freelancer being onboarded to handle enterprise contracts. Risk-based approaches trigger more intensive checks where the stakes are higher, and keep the experience frictionless for everyone else.

Think about both sides of the marketplace

Most fraud prevention investment goes into verifying the supply side – workers, drivers, sellers. The demand side gets less attention, partly because customers are revenue and friction costs conversions. But buyer fraud is real, and verifying workers without verifying customers means protecting one side of a two-sided market.

Document everything

When fraud occurs – and it will – having a clear audit trail of what checks were run, when, and what the result was matters. For regulatory purposes, for insurance, and for understanding where the gap was. Platforms that treat verification as a checkbox rarely have the documentation they need after an incident.

The Solution

For platforms that need to move beyond basic identity checks, our identity verification solution covers the core requirements in a single flow – document verification, biometric face matching, 3D liveness detection, and more, confirming that the person onboarding is real, that their documents are genuine, and that they are physically present rather than attempting to bypass the system with a photo or deepfake.

We support over 3,000 document types across 200+ countries, which matters for operators dealing with workers and users from multiple markets, so checks can be triggered at onboarding, before specific transactions, or periodically for ongoing monitoring, and for marketplaces that verify both workers and customers, the flows are configurable independently – no need to apply the same level of scrutiny to everyone.

Results, audit logs, and compliance records are in one place. If you want to see how it works in practice, the demo is a better starting point than a spec sheet.

Book a demo to see iDenfy’s identity verification in action for gig economy and marketplace use cases.

The Regulatory Direction

The gig economy has benefited from being in a regulatory grey area for most of its existence. That is closing.

The EU’s Digital Services Act has already introduced new obligations for large platforms around transparency and accountability. The forthcoming AMLR and PSD3 frameworks will extend formal AML and KYC obligations to digital marketplaces facilitating payments, which covers a significant share of the gig economy by transaction volume. In the US, the picture is more fragmented by state, but scrutiny of platforms facilitating large payment volumes to workers without adequate identity controls has increased, particularly around money laundering risk and tax compliance.

48% of employers have already dealt with identity fraud among freelancers in the gig economy. That is not a niche compliance problem – it is a mainstream operational one. Platforms building verification infrastructure now, rather than treating it as a future requirement, are the ones better positioned when the scrutiny arrives.

Conclusion

The gig economy is not going to slow down, nor is the fraud that follows it – what will change is the regulatory environment, and platforms that have been coasting on light-touch identity checks will find the next few years uncomfortable as the compliance bar rises across the board.

The good news is that none of this requires building something from scratch, – verification infrastructure exists – tools to handle document checks, biometric matching, and ongoing monitoring at scale are available, integrable, and increasingly affordable compared to the cost of the fraud they prevent, the gap is not usually technical – it is a decision about whether to treat identity verification as a foundation or an afterthought.

Platforms that get this right do not just reduce fraud losses. They build something harder to quantify but ultimately more valuable: a reputation for being a place where trust holds.