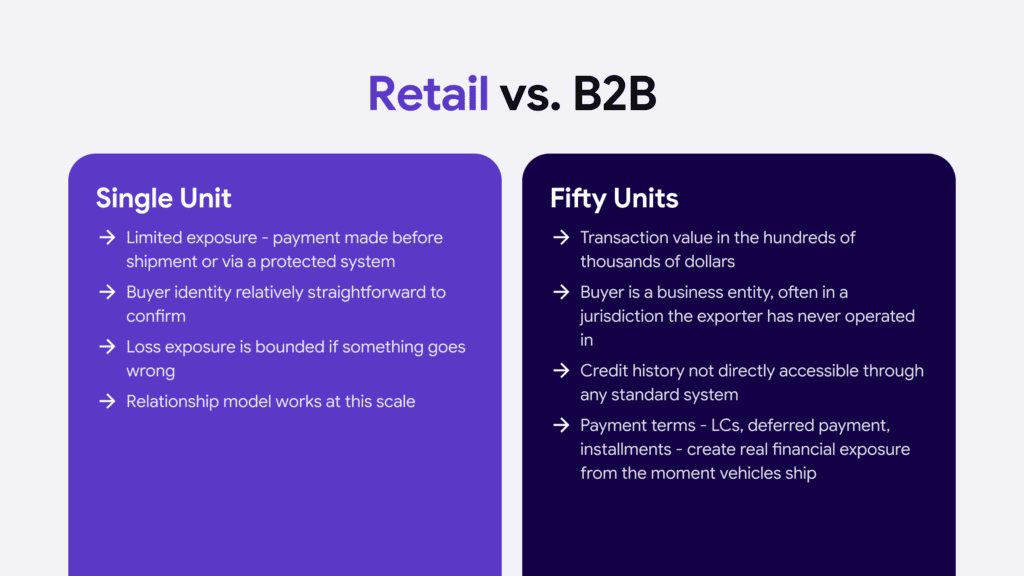

A car exporter shipping a single unit to a retail buyer takes on limited risk. The payment is made before the vehicle leaves or via a system with solid buyer protection. The loss exposure if something goes wrong is bounded.

A car exporter moving fifty vehicles to a dealership network in a new market is a different proposition entirely. The transaction value runs into hundreds of thousands of dollars. The buyer is a business entity, often incorporated in a jurisdiction in which the exporter has never operated, with a credit history that isn’t directly accessible through any system the exporter can easily query. Payment terms – particularly where letters of credit, deferred payment arrangements, or installment structures are involved – mean the exporter carries real financial exposure from the moment the vehicles ship.

That exposure is where buyer bank verification comes in. And it’s one of the most consequential steps that many exporters still handle informally, if at all.

Who this is for – and what it’s not. For automotive exporters, trade finance managers, and export sales leads shipping vehicles in bulk to dealer networks abroad – specifically those extending payment terms on deals large enough that a buyer default would actually hurt.

Not a guide to letter-of-credit mechanics or shipping documentation. For the compliance side of vetting the buying entity itself, see Know Your Business Solution; this article is the financial due diligence checklist before you ship.

Why Informal Vetting Doesn’t Scale

The traditional approach in automotive export has always been relationship-based. You know your buyers. You’ve met them at trade shows, done a few smaller deals first, and built trust over time before scaling volume. That model worked when the industry was more geographically concentrated and deal cycles were longer.

The global B2B e-commerce market was estimated at $24.08 trillion in 2025 and is projected to reach $105 trillion by 2033. That growth is being driven by digital procurement – buyers sourcing from exporters they’ve never met in person, at higher volumes, in faster deal cycles. The relationship-first model simply doesn’t scale into that environment. And the “anonymity gap” it creates – buyers nobody has actually vetted – is a significant and growing liability.

For automotive exporters specifically, the risk profile has shifted. Japanese, Korean, and increasingly Chinese vehicle exports now reach dealers across sub-Saharan Africa, Southeast Asia, Eastern Europe, and Latin America via intermediaries and platforms where the exporter may have no existing relationship with the end buyer. A dealer network in Lagos or Nairobi placing a $400,000 order for a container shipment of used vehicles needs to be financially verified – not assumed to be good for it because they sent a professional inquiry email.

Automate your identity verification

See how iDenfy helps 1,000+ companies verify customers in seconds with AI-powered KYC.

Explore iDenfyWhat “Bank Verification” Means in This Context

Bank verification in a B2B trade context is not simply asking a buyer to provide their bank account number. It covers a broader set of checks designed to determine whether the buying entity has the financial capacity to complete the transaction and honor the payment terms under discussion.

A complete bank verification process for a large automotive export deal typically includes several components.

Bank confirmation letter

The buyer’s bank provides a letter confirming that the buyer maintains an active account in good standing and that sufficient funds are available to support the proposed transaction amount. This isn’t a guarantee of payment – it’s a confirmation of capacity. The letter should be on the bank’s letterhead, signed by a named officer, and ideally verifiable by direct contact with the issuing branch.

Letter of credit (LC)

For high-value deals, particularly across markets with elevated payment risk, a letter of credit issued by the buyer’s bank is the standard instrument. The LC commits the bank – not just the buyer – to payment upon presentation of conforming shipping documents. The exporter’s freight forwarder or trade finance advisor will typically guide the specific documentary requirements, but the LC itself is the mechanism that moves the financial obligation from the buyer to the institution.

Trade reference verification

Direct contact with two or three of the buyer’s existing suppliers – particularly other vehicle exporters or suppliers of related parts and accessories – is one of the most reliable ways to assess a buyer’s payment behavior in practice. References can be coached; actual supplier contact cannot.

Beneficial ownership and KYB check

Bank verification in the narrow financial sense should run alongside a broader check on the entity itself. Who owns the dealer network? Is it a standalone business or part of a group? Are there politically exposed persons in the ownership structure? Has the entity been involved in disputes, regulatory actions, or legal proceedings? Verifying the bank account without verifying the business behind it is an incomplete process.

The Specific Risks Car Exporters Face

Automotive exports have risk characteristics that differ from those of general merchandise trade.

Vehicle-specific fraud

Invoice manipulation and vehicle substitution are active forms of fraud in automotive exports – a buyer claims to have paid for one specification but disputes the vehicles received. Verification of the buyer’s financial credibility doesn’t directly prevent this, but a buyer with a verified credit history and confirmed banking relationships is meaningfully less likely to engage in transaction fraud than an unverified buyer with no traceable financial footprint.

Currency and payment route complexity

Large automotive deals in emerging markets often involve intermediary currencies, correspondent banking arrangements, and payment routes that are more complex than standard international transfers. Understanding where the buyer’s funds are actually held – which bank, in which jurisdiction, in which currency – is relevant to both payment security and sanctions compliance. Receiving payment routed through a correspondent bank in a jurisdiction subject to sanctions creates exposure regardless of the buyer’s good faith.

Extended delivery timelines

Container shipping from Japan, Korea, or China to sub-Saharan Africa or Latin America typically runs four to eight weeks. In that window, buyer circumstances can change – business liquidity events, regulatory changes in the import market, or simply a change in market conditions that makes the buyer reluctant to complete. Financial verification before shipment doesn’t eliminate this risk, but it gives the exporter a documented basis for legal recovery if the buyer defaults.

Volume commitment vs. actual payment capacity

Buyers representing dealer networks often present aspirational volume commitments – “we’ll take fifty units this quarter, then scale to two hundred per year.” The volume is appealing. The financial verification question is whether the buyer can actually fund the first 50, let alone the 200. Bank verification anchors the conversation to demonstrated capacity rather than projected ambition.

Building a Scalable Verification Process

The challenge for most automotive exporters isn’t that they don’t understand the need for buyer verification – it’s that the process is either non-existent, ad hoc, or so labor-intensive that it slows deal closure to the point where buyers go elsewhere.

A scalable verification process for large B2B automotive deals doesn’t need to be elaborate. It needs to be consistent and documented.

At a minimum, every buyer above a defined transaction value threshold should go through:

- Entity verification – confirm the legal name, registration number, registered address, and active status against the relevant company registry. For markets where APIs don’t exist, manual registry checks with documented results.

- Beneficial ownership identification – identify the individuals who ultimately own and control the buying entity. Screen them against sanctions lists, PEP databases, and adverse media sources.

- Bank confirmation – request a bank confirmation letter or proceed via a letter of credit for transactions above a defined value threshold. The threshold will vary by business, but having one in policy is more important than the specific number.

- Credit reference check – run a D&B or equivalent report on the buyer entity. For markets where global credit reference data is scarce, trade reference calls with existing suppliers serve as an effective substitute.

- Document trail – every verification step should be documented in the deal file. The documents obtained, the searches run, the results returned, and the decision taken on that basis.

The last point is worth emphasizing because exporters sometimes treat verification as an internal sense-check rather than a formal record. In the event of non-payment, a documented verification process is the foundation of any legal recovery action. Without it, proving that due diligence was conducted is significantly harder.

Technology Is Catching Up With the Problem

The manual, relationship-dependent model of buyer verification is being supplemented by technology that makes the process faster and more consistent – even across the emerging markets that automotive exporters increasingly serve.

KYB platforms now cover company registries and beneficial ownership data across a growing number of markets. Automated sanctions and PEP screening run in seconds. Bank account verification tools can confirm that a stated account exists and is active without requiring the exporter to contact the buyer’s bank directly. Document verification technology can authenticate bank confirmation letters and trade documents with a level of scrutiny that manual review can’t replicate at scale.

None of this replaces judgment. A buyer who passes every automated check but pushes hard to avoid a letter of credit, insists on unusual payment routing, or declines to provide trade references is telling you something that no technology platform will surface. The instinct that something is off is worth acting on even when the checks come back clean.

But for exporters processing significant deal volumes across multiple markets, systematic technology-supported verification is what separates a scalable commercial operation from one that runs on accumulated good luck and the occasional expensive mistake.

Conclusion

The irony of buyer verification in automotive exports is that the deals most in need of verification are often the ones that feel least in need of it. A confident buyer, a professional inquiry, a plausible business profile, and a compelling volume commitment all create psychological momentum to say yes and deal with the paperwork later.

The verification discipline that matters is the one that runs regardless of how good the deal feels. Because the deals that go wrong are almost always the ones where something felt fine right up until it wasn’t.