For banks, data is the first impression nowadays. When a new user applies for an account, takes out a loan, or requests credit, banks rely on digital signals to decide whether that person is trustworthy, solvent, and compliant. Nowadays, smart bank onboarding is more like a moment when user experience meets risk management – and where data is the difference between smart decisions and costly mistakes.

The best banks are not simply automating old processes. They are rethinking what onboarding means, using data as both a filter and a foundation for long-term relationships.

Why Data Has Become Central to Bank Onboarding

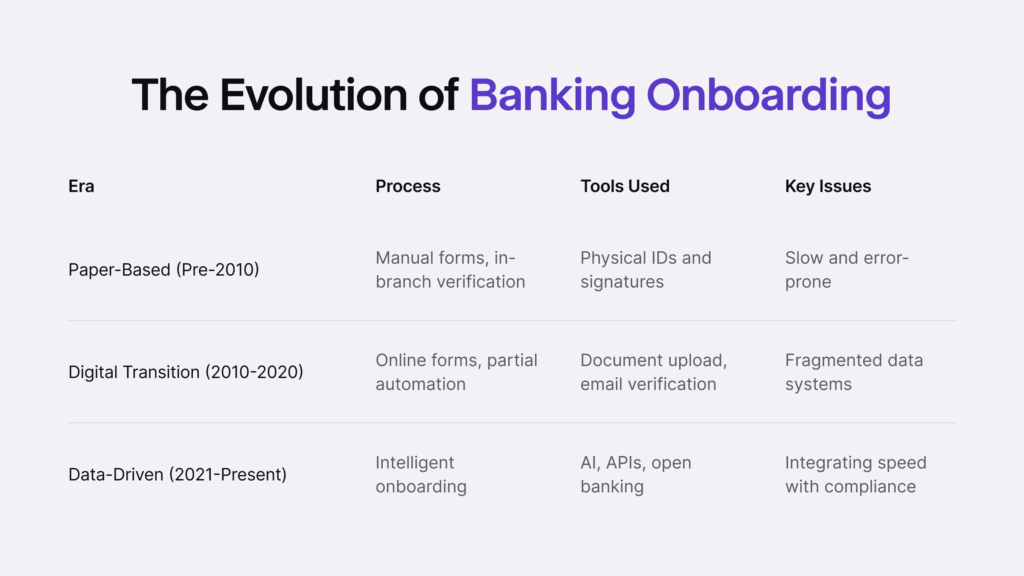

For decades, onboarding was a manual process. Branch staff collected paper forms, checked IDs, and passed applications along to compliance teams. It was slow, expensive, and mistakes were common.

That model doesn’t hold up when customers expect to open an account in minutes. The move to digital banking forced financial institutions to rethink how they assess risk without ever meeting a customer face to face.

Now, by combining identity data, behavioral analytics, credit insights, and compliance checks, banks can build a detailed picture of an applicant in seconds. Onboarding is faster, but it’s also more informed – risk isn’t just managed after the fact, it’s anticipated before anything goes wrong.

Automate your KYC process

iDenfy verifies customers from 200+ countries in seconds. AI-powered, compliant, and trusted by 1,000+ companies.

Explore KYC SolutionData as a Decision Engine

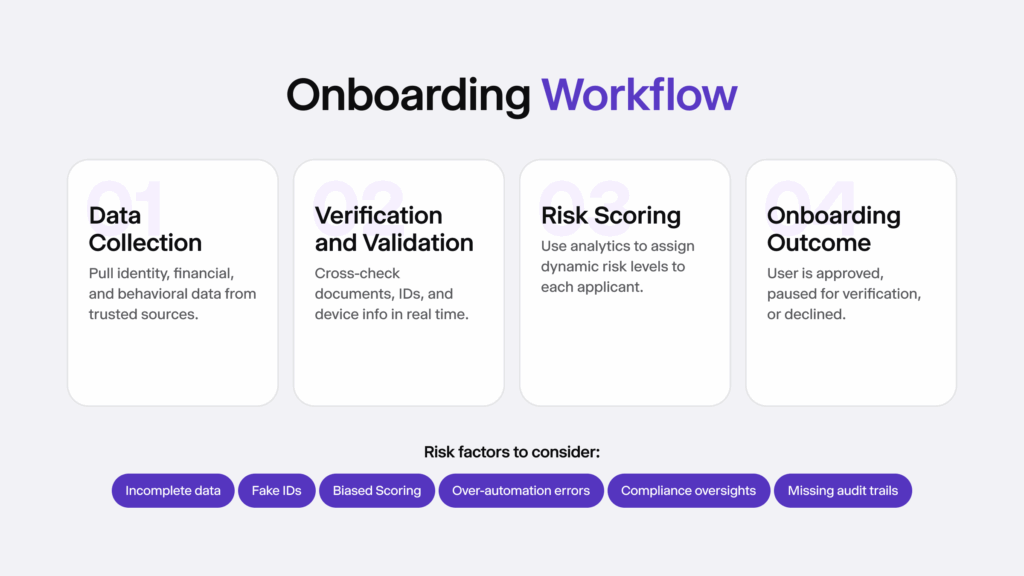

Data allows banks to move to a higher level of verification. Instead of simply confirming that a document looks real, they can understand who the customer is and how they behave financially.

Some of the most common data categories used include:

- Identity data: Government IDs, biometrics, device fingerprints, and IP addresses that establish the applicant’s identity.

- Financial data: Credit scores, transaction histories, and income patterns that help gauge risk and reliability.

- Behavioral data: Typing speed, device movement, and login frequency that can reveal potential fraud attempts.

- Open banking data: Direct account connections that show how a person or business manages funds in real time.

Instead of treating every applicant the same, banks can tailor smart bank onboarding decisions based on genuine context – approving low-risk customers quickly while flagging inconsistencies for further review, creating a dynamic risk profile.

Smarter Screening Through Predictive Analytics

One of the most significant advantages of data-driven smart bank onboarding is predictive capability, while traditional verification checks look backward – analyzing past transactions or known fraud patterns.

By feeding historical onboarding outcomes into machine learning models, banks can detect subtle correlations that humans might miss. For instance:

- A specific device type combined with a new IP address might correlate with synthetic identity fraud.

- Certain transaction sequences could signal a higher chance of account misuse.

- Behavioral deviations, like applying at unusual hours, may indicate risk even before the first transaction happens.

This predictive layer turns onboarding from a reactive process into a proactive one. Banks can act before fraud happens rather than after it is too late.

Related: Fraud Detection Using AI in Banking

How Data Personalizes the User Journey

Smart bank onboarding is also about creating a seamless experience and Quality of Life (QoL). Data allows banks to personalize the process to each user’s profile.

For example:

- Returning users can skip steps where their verified data is already on file — and get prompted to update anything that’s gone stale

- Low-risk applicants go straight through; higher-risk ones get routed to a more thorough verification process

- Small businesses can receive onboarding flows that match their sector – for instance, fintech startups might trigger due diligence compared to low-risk service companies

This kind of contextual onboarding makes users feel understood rather than processed. It reduces friction without compromising compliance – a balance that is increasingly becoming more difficult to achieve in regulated industries.

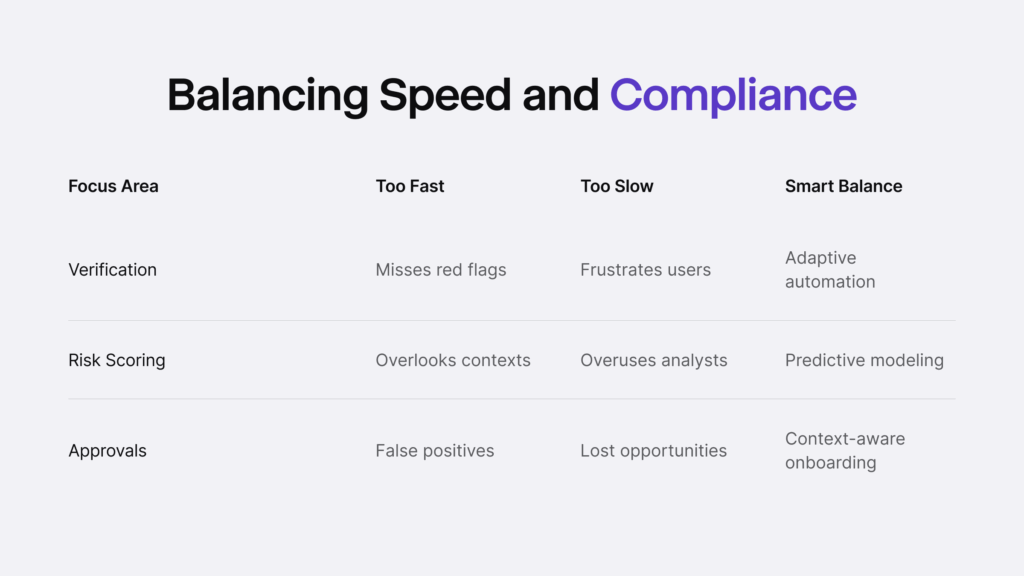

Speed and Security

Banks face a constant trade-off: please users by being fast, but stay cautious enough to satisfy regulators; therefore, data analytics helps close that gap.

Manual document review and broad assumptions have given way to real-time data. Automated systems pick out the cases that need human attention, so compliance officers aren’t buried in routine checks – they’re looking at the ones that actually warrant it.

In practice, that might mean an identity verification service that combines biometric checks with data analytics, validating individuals and businesses on the spot. The automation handles the volume. The humans handle what the automation flags.

Data and the Rise of Collaborative Intelligence

One of the quiet revolutions happening in banking is the shift from isolated data to shared intelligence.

Banks increasingly participate in data-sharing networks that pool anonymized risk insights across institutions. When one bank detects a fraud pattern, others can learn from it almost instantly. This “collaborative intelligence” model strengthens the entire financial ecosystem, making it harder for fake individuals to exploit isolated gaps.

In practice, that might mean shared blacklists of known fraudulent identities, or cross-platform behavioral markers that flag unusual applications across different institutions. It is a powerful reminder that data is not just useful – it is communal.

Compliance and Data Science

Compliance teams used to be filtered from data teams. Now, the two work side by side.

Modern onboarding uses regulatory data – such as sanctions lists, PEP databases, and adverse media – alongside advanced analytics to surface risk patterns more quickly. Instead of checking names manually, algorithms continuously monitor new applicants against live data streams.

This approach has transformed how banks manage compliance workloads. Automated screening not only saves time but also reduces human bias and error. Regulators are beginning to recognize this shift too, encouraging banks to adopt data-driven systems that maintain accuracy and improve efficiency.

From Data to Trust

Fast, well-run onboarding leaves a mark. A customer who gets through the process quickly and without unnecessary friction starts the relationship on the right foot. A business that’s vetted thoroughly but without feeling interrogated sees the institution as professional – not something to work around.

That first impression carries further than most banks give it credit for. What starts as a smooth sign-up becomes a reason to stay, and eventually a reason to bring more business.

None of it works without honesty, though. People share personal and financial information during onboarding, and they notice when institutions are vague about what happens to it. Being straightforward about data use, consent, and privacy isn’t just good compliance practice – it’s what makes the trust feel earned rather than assumed.

Issues of Data-Driven Onboarding

Data-driven onboarding comes with real tradeoffs. Collecting enough information to make sound decisions while staying within privacy boundaries isn’t a problem that gets solved once – it requires constant attention as regulations shift and customer expectations change.

Data silos make things harder than they need to be. Credit risk, compliance, and other departments often run on separate systems, which means duplicated work and insights that fall through the gaps. Pulling those sources together takes technical investment, but it also takes the kind of internal alignment that’s harder to buy than software.

Then there’s the ethics question. As machine learning takes on more of the onboarding process, banks have to make sure their models are explainable, consistent, and not quietly encoding bias into decisions. A system that’s fast and automated isn’t an improvement if it’s discriminating against certain applicants or producing outcomes nobody can account for.

What the Future of Smart Bank Onboarding Looks Like

Data-driven onboarding is quickly shifting from a differentiator to a baseline. Customers already expect fast, accurate decisions – what’s changing is how much of what sits behind that expectation gets rebuilt from the ground up.

More real-time data will feed directly into onboarding engines – open banking APIs, verified identity networks, and behavioral signals that didn’t exist a few years ago. The sources will multiply, and the systems processing them will get better at knowing what to do with them.

Predictive models will keep getting sharper, learning from every application that moves through the system. The feedback loop compounds over time – each decision, successful or not, adds to what the model knows.

Regulators will follow. Automated decision-making at scale will attract scrutiny, and banks will need to demonstrate not just that their systems work, but how. The ones that come out ahead will be those that stopped treating onboarding as a compliance exercise and started treating it as the opening move in a longer relationship.

Conclusion

Banking has always run on trust. In a digital environment, that trust gets established earlier than it used to – often before a customer has spoken to anyone. The institutions that know how to handle data responsibly and use it well will make better onboarding decisions: faster, fairer, and with greater confidence.

It is not just about preventing fraud or satisfying regulators. It is about understanding customers better – seeing more than just the form fields and behavior.

With tools like AI analytics, open banking integrations, and modern identity verification services, banks now have the ability to turn onboarding into a strategic advantage. The smarter the data, the stronger the trust – and in modern finance, trust is the ultimate currency.