You passed the challenge. Your funded account is live, you’ve hit your profit target, and now it’s time to request a payout. Then the KYC request lands in your inbox – and suddenly the process feels a lot less straightforward than the trading itself.

This is something many traders run into, and it’s not just a formality. Prop firms are under increasing pressure from payment processors, financial regulators, and anti-money laundering frameworks to verify the identities of those they pay. If your documents aren’t in order when that payout request gets reviewed, you’re looking at delays, frozen withdrawals, or – in worst cases – account suspension.

So, let’s break down exactly what prop firm payout KYC involves, why firms are tightening these checks, and what you need to have ready before you submit your first withdrawal.

Why Prop Firms Run KYC at the Payout Stage

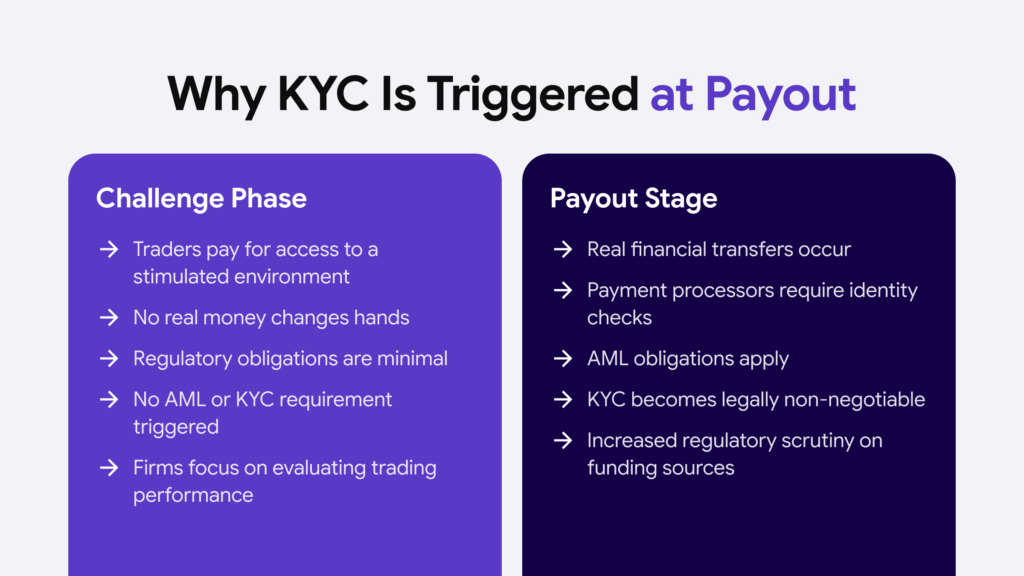

It might seem odd that a firm lets you trade for weeks, maybe months, and only asks for identity verification when money is about to move. There’s a straightforward reason for this: payouts are where things get regulated.

During the challenge phase, traders are essentially paying for a simulated environment. But once real money is being transferred – even if it’s technically profit-sharing from the firm’s capital – payment processors and banking partners require the firm to verify identities under AML (Anti-Money Laundering) and KYC obligations.

This isn’t unique to prop trading. The same logic applies to crypto platforms, iGaming operators, and online brokerages. The moment a financial transfer is involved, identity verification becomes non-negotiable. Firms that skip this step risk losing their payment processing relationships entirely, which is far more serious than a delayed trader payout.

Some firms, especially newer ones, have also faced scrutiny over where their funding actually comes from – and regulators have taken notice. Tighter KYC at the withdrawal stage is partly a response to that pressure.

Automate your KYC process

iDenfy verifies customers from 200+ countries in seconds. AI-powered, compliant, and trusted by 1,000+ companies.

Explore KYC SolutionWhat Documents You’ll Typically Need

The exact requirements vary between firms, but most follow a standard KYC framework that covers three core areas: identity, address, and payment method verification.

Government-issued photo ID

The starting point for almost every prop firm’s KYC process. This is typically a passport, national identity card, or driver’s license. The document needs to be valid – expired IDs are rejected outright – and the photo, name, date of birth, and document number must be clearly visible. Some firms now use automated document verification systems that scan for tampering, so image quality matters more than traders often realize.

Proof of address

Most firms ask for something recent – typically within the last three months – that has your full name and home address on it. Utility bills, bank statements, or letters from a government body tend to work well. Mobile phone bills are hit-or-miss depending on the firm, so it is worth double-checking before you submit one. One thing that catches people out: the address on whatever you send in has to match what’s listed on your trading account, which becomes a problem if you’ve moved and haven’t updated your details.

Selfie or liveness verification

Many firms now ask traders to submit a photo holding their ID document, or to complete a short video verification through a third-party identity provider. This step is specifically designed to prevent account sharing and identity fraud – both of which have become more common as the funded trading industry has grown.

Payment method verification

For bank withdrawals, some firms will want to see a recent statement or a screenshot from your banking app that shows your name and IBAN. Crypto is usually simpler – most firms just need the wallet address, though some will ask you to confirm the wallet is actually yours.

Common Reasons KYC Gets Rejected (and How to Avoid Them)

The majority of KYC delays aren’t caused by anything suspicious – they come down to avoidable document issues that traders could easily fix before submitting.

Document glare and poor lighting

The most common issue by far. Photographing a passport under overhead lighting creates glare that covers the text, and most automated verification systems will reject it straight away. Lay the document flat on a dark surface, use natural light or soft indoor lighting, and make sure all four corners are in the frame.

Cropped documents

The full document – including all four edges – needs to be in frame. It’s easy to accidentally cut off a corner when taking a photo with a phone, especially with larger ID cards.

Mismatched details

If your ID shows your full legal name, including a middle name, your account should reflect the same. Nicknames or shortened versions of your name on the account create friction and slow the review.

Outdated proof of address documents

Some people submit documents from the right institution, but from four or five months ago, which sits outside the standard three-month window most firms require.

Screenshots of documents, rather than the originals

Firms require actual documents – PDFs downloaded from your bank’s portal or clear photographs of physical documents. Screenshots of screenshots, or images of a phone screen showing the document, are typically rejected.

Enhanced Due Diligence: When Firms Ask for More

Most traders will move through standard KYC without any issues. But certain situations trigger Enhanced Due Diligence (EDD) – a more intensive review process in which the firm requests additional documentation.

This typically happens when a trader requests a large payout for the first time, when the account activity looks unusual compared to the trader’s profile, or when the trader is based in a jurisdiction flagged as higher risk under AML frameworks. Some firms also automatically apply EDD to traders with multiple funded accounts.

In EDD scenarios, firms might request a source-of-funds declaration, additional proof of identity, or even a short video call with their compliance team. It’s not a sign that something is wrong – it’s a risk management process that financial institutions use across the board.

If you’re asked for additional documentation, the best approach is to respond quickly and completely. Delays on the trader’s side during an EDD review are among the main reasons payouts are held for extended periods.

How to Prepare Before You Request Your First Payout

The traders who complete KYC the fastest are those who treat it as part of account setup rather than an afterthought when a payout is pending.

A few practical steps that make a difference: Check that your account details – name, address, date of birth – match your primary ID document exactly, and make this check when you first register, not when you’re waiting for a payout. Keep a folder with digital copies of your KYC documents ready to go. Scan your passport rather than photographing it, if possible, since scanned copies tend to produce higher-quality images. Make sure your proof of address document is consistently updated – if you move, update your account details at the same time.

Rather than the originals, it’s also worth reading the prop firm’s specific KYC policy before your first payout request. Requirements vary more than traders expect, particularly around which document types are accepted for proof of address and whether the firm uses a third-party identity verification platform or handles checks internally.

Conclusion

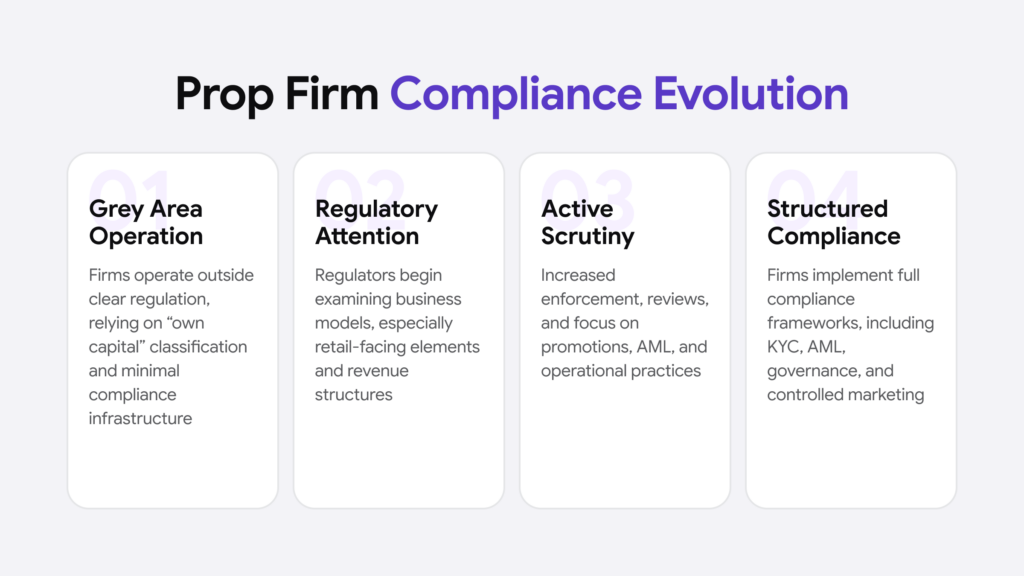

KYC at the payout stage isn’t going away – if anything, it’s going to become more thorough as the prop trading industry matures and faces more regulatory scrutiny. Payment processors have already tightened requirements for prop firms, and that pressure flows directly to traders at the time of withdrawal.

Understanding what’s required and having your documents ready isn’t just about getting paid faster, though that’s obviously a benefit. It’s about operating professionally within a framework that exists to protect both traders and firms from fraud, money laundering, and financial abuse. The traders who approach it that way tend to have significantly fewer problems.