Last updated: June 2026

Sanctions lists tell you who’s already been caught. PEP lists tell you who holds political power. But neither one tells you what’s in tomorrow’s news — and that’s exactly the gap adverse media screening is designed to close. The UNODC estimates that 2–5% of global GDP — roughly $800 billion to $2 trillion — is laundered every year, and Nasdaq’s Verafin puts illicit funds flowing through the financial system at $3.1 trillion in 2023 alone. So if you’re operating in a regulated industry, screening for negative news isn’t something you can afford to skip.

Adverse media screening is a core part of Anti-Money Laundering (AML) and Know Your Customer (KYC) compliance — and for most regulated businesses, it’s legally required. In this article, we walk through what adverse media screening actually is, why it matters, and how to build a program that works from onboarding through ongoing monitoring.

Who this is for — and what it’s not.

For compliance and onboarding teams operationalizing adverse media screening at onboarding and on an ongoing basis, for individuals, businesses, or beneficial owners.

Not a legal opinion on your obligations, and not a guide to ad-hoc Googling of customers. For a deeper look at keyword strategies and source types used in adverse media checks, see Keywords in Adverse Media Screening; this article is the “how.”

What Is Adverse Media Screening?

Adverse media screening — often called negative news screening — is the process of reviewing damaging information published about a person or company across news outlets, regulatory notices, court records, and enforcement announcements. The goal is to assess their financial crime risk before or during a business relationship, catching red flags that official lists haven’t yet picked up.

In practice, adverse media surfaces high-risk profiles before they show up on sanctions or PEP lists. The categories you’re looking for include financial crime (money laundering, fraud, bribery), terrorism financing, drug trafficking and organized crime, regulatory enforcement actions, and reputational risks like corruption or modern slavery.

Screening draws from both online and offline sources — news articles, social media, blogs, regulatory bulletins, television, and radio. While financial institutions are the heaviest users, other industries managing ESG risk or operating in high-risk markets are increasingly building adverse media programs too.

Automate your identity verification

See how iDenfy helps 1,000+ companies verify customers in seconds with AI-powered KYC.

Explore iDenfyAdverse Media Check vs. Continuous Screening: What’s the Difference?

Here’s a distinction that matters more than it looks. An adverse media check is a single lookup on one customer — usually done at onboarding. Adverse media screening is the repeatable, automated program you run across your entire customer base on an ongoing basis. Within AML and KYC compliance, it fills the gap that official lists leave behind — catching reported risk that hasn’t been formalized anywhere yet.

| Adverse Media Check | Continuous Screening | |

|---|---|---|

| Execution | Manual or ad-hoc lookup | Automated, programmatic |

| Frequency | Once, usually at onboarding | Daily, across the entire customer base |

| Primary goal | Baseline risk on a new customer | Real-time risk detection on existing customers |

| Data needs | Core identity attributes (name, DOB) | Verified identity data plus ongoing-monitoring webhooks |

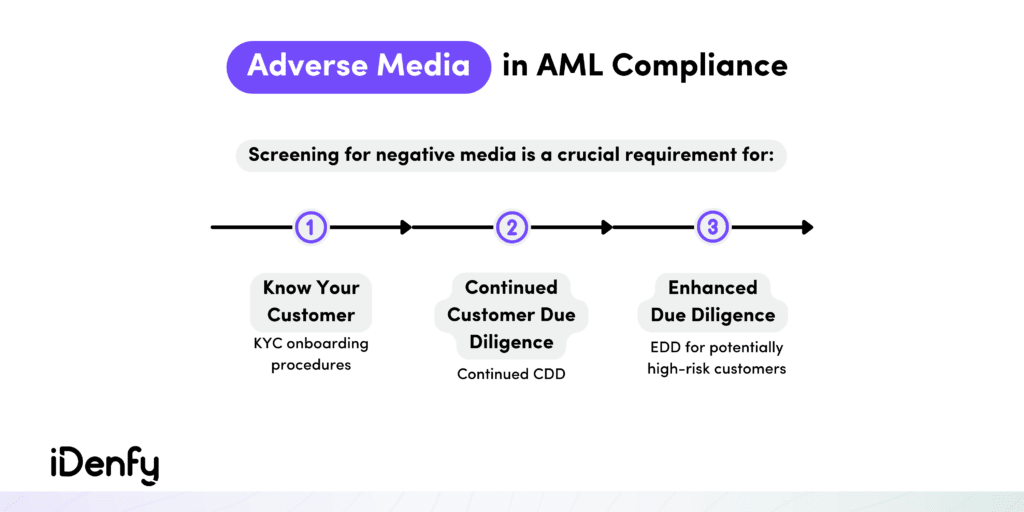

Why Is Adverse Media Screening Important?

The short answer: because the risk doesn’t stay still. A customer who was clean at onboarding can hit the news six months later — and without ongoing screening, you won’t know until it’s too late. That’s why adverse media screening isn’t just a one-time checkpoint; it’s a continuous process for detecting risk before it escalates into a regulatory or reputational problem for your business.

Under AML obligations, regulated companies must conduct ongoing customer due diligence (CDD) — and adverse media is a required element of that. The Final CDD Rule makes this explicit: you must screen and monitor each customer throughout the entire business relationship, not just at the point of sign-up. Regular checks also demonstrate your commitment to compliance — something regulators look for when reviewing your program.

Compliance Guidelines for Adverse Media Checks

The regulatory pressure is real. To establish an effective compliance program, you’ll need to adhere to the frameworks that apply to your jurisdiction:

In the United States

- The Financial Crimes Enforcement Network (FinCEN) requires regulated businesses to comply with the Bank Secrecy Act (BSA).

- Adverse media findings directly feed into Suspicious Activity Report (SAR) filings — so the quality of your screening directly affects your SAR program.

In Europe

- Under the 6th Anti-Money Laundering Directive (6AMLD), banks are required to conduct enhanced due diligence for customers deemed high-risk.

- Financial Action Task Force (FATF) guidelines explicitly recommend adverse media checks as part of Enhanced Due Diligence (EDD) — and most national regulators have adopted this recommendation into local law.

The Challenges of Adverse Media Screening

Millions of news articles are published every day. Manually reviewing all of them isn’t just impractical — it’s impossible. And yet, that’s exactly what compliance teams are forced to do when they rely on traditional third-party databases and basic search engines. The result is a pile of duplicates, irrelevant matches, and occasional misinformation that takes hours to sort through.

Manual screening creates several persistent problems:

- Hidden data. Restricted content, foreign-language sources, and paywalled articles create blind spots in your screening — and getting access often costs extra.

- Questionable reliability. Many platforms let anyone publish without verification, which means you’re often spending time checking whether a piece of negative news is even accurate.

- False positives at scale. Common names generate floods of irrelevant matches. Manually disambiguating them is the single biggest drain on compliance team bandwidth — and a major driver of analyst burnout.

“Sometimes I have a very long list of similar names … and I have to go through them one by one.”

— In-house compliance counsel at a UAE-based firm, on manually clearing adverse-media false positives

Related: Transaction Screening vs Transaction Monitoring [AML Guide]

How to Conduct Adverse Media Screening: 7 Steps

There’s no single mandated process — FATF’s risk-based approach gives you a framework, not a script. But every effective program covers the same lifecycle, from policy through audit trail. Here’s how to build yours.

Step 1 — Define a Risk-Based Screening Policy

Before you screen anything, you need to decide what you’re screening for. That means documenting your risk tiers (standard, high-risk, PEPs, high-risk jurisdictions), setting frequency per tier, and defining what actually counts as adverse media in your program. Anchor this to your KYC risk assessment so it’s consistent with your broader compliance posture.

Specifically, your policy should answer:

- Who published the negative news? State institution publications carry far more weight than tabloids.

- Allegations vs. convictions — decide upfront whether unproven allegations trigger a review or whether you only act on confirmed findings.

- Relevance to financial crime — a speeding ticket isn’t adverse media; money laundering and fraud are. Define where your line sits.

- Time horizon — set a lookback limit after which older items no longer count as actionable negative news.

Step 2 — Standardize Verified Customer Data

Your matching quality is only as good as the data you’re matching against. Use verified attributes — full legal name, date of birth, nationality — and for businesses, the registered entity name and beneficial owners (UBOs). Clean, verified identity data cuts false positives dramatically before a single screen is even run. Don’t skip this step — it’s what makes everything downstream manageable.

Step 3 — Run the Initial Screen at Onboarding

Screen each customer against adverse media alongside sanctions, PEP, and watchlists in a single pass. Doing this in one integrated step — as part of your digital onboarding flow — means identity verification and risk assessment happen together, not as disconnected manual stages that slow down your team and frustrate your customers.

Step 4 — Filter False Positives

Raw media search is noisy — that’s just the reality. You’ll need to strip out context-irrelevant and non-criminal records, then confirm potential matches using verified data points like date of birth, location, and entity identifiers. This is the single most important step for keeping your program manageable. Without it, analysts spend most of their time on false alarms instead of real risk.

Step 5 — Investigate and Risk-Rate True Matches

Once you’ve confirmed a real hit, you need to assess its severity, recency, and relevance to your business relationship. Assign a risk rating, update the customer’s risk profile, and escalate serious cases into Enhanced Due Diligence (EDD). Document your reasoning at every step — not just the outcome, but why you made the call you made.

Step 6 — Switch on Ongoing Monitoring

This is the step most compliance teams skip — and it’s the one that creates the biggest exposure. A customer who was clean at onboarding can hit the news a year later. If you’re not monitoring, you won’t know. Enroll every active customer into continuous, ideally daily, ongoing monitoring so new adverse media triggers an automatic alert — no manual re-screening, no delays.

When new adverse media surfaces, a well-configured monitoring platform pushes a webhook to your endpoint in real time:

{

"event": "aml.adverse_media.match",

"customer_id": "cust_90210_uk",

"status": "alert_triggered",

"severity": "high",

"match": {

"category": "financial_crime",

"matched_term": "money laundering investigation",

"source_url": "https://news-source.example/article"

}

}Step 7 — Document Every Decision for Audit

Record what you screened, what you found, how each alert was dispositioned, and who approved it. A time-stamped audit trail is what proves an effective AML program to regulators — and it’s your protection if an investigation ever comes knocking. Don’t treat documentation as an afterthought. It’s part of the program.

Automated Solutions for Adverse Media Checks

Running seven steps manually across thousands of customers doesn’t scale — and it doesn’t have to. Automated adverse media screening improves quality, efficiency, and speed all at once, while reinforcing the overall effectiveness of your compliance program. FATF has flagged AI-powered screening as one of the most promising opportunities for AML programs trying to keep pace with modern financial crime volumes.

At iDenfy, we’ve built adverse media screening into a fully automated KYC system that you can also layer into your existing AML screening workflow. Here’s what that means in practice:

- In-house adverse media search with a proprietary filter that automatically removes non-criminal, context-irrelevant records — Step 4, handled for you.

- One pass, full coverage — adverse media plus sanctions and all four PEP levels plus watchlists in a single flow.

- Daily monitoring pushed to your dashboard or via API webhooks — no manual re-screening required.

- Tied to identity verification — customers enter monitoring automatically after verification, with audit-ready results in seconds.

“We can now provide a straightforward automatic KYC and AML system in the form of our easy-to-use plugin, which has lifted the burden of manual documentation review.”

— Adrian Pollard, Co-Founder, HollaEx

“iDenfy has played a critical role in our ability to rapidly and accurately verify the identities of our clients.”

— Giedrė Blazgienė, CEO, Mano Bank

Related: What is AML Screening?

You can combine PEP and sanctions monitoring with continuously updated adverse media results — all in one place. Try iDenfy for free or contact us to see how it fits your workflow.

Read More Articles

- Enhanced Due Diligence: What It Is and When It’s Required

- What Is Ongoing Monitoring in AML Compliance?

- KYC & AML Compliance: A Practical Guide

- Transaction Screening vs Transaction Monitoring [AML Guide]