Learn how “pay-per-completed” billing quietly inflates your identity verification costs, and why a pay-per-approved model gives you a fixed, predictable cost per onboarded customer.

You budgeted for verification based on the number of real customers you expected to onboard. Then the invoice came in higher, because you also paid for every fraudster, every blurry passport photo, and every user who gave up halfway through.

In short: Most KYC pricing models charge per completed session, so you pay for failed, fraudulent, and abandoned attempts that never become revenue. A pay-per-approval model bills only for verified, accepted customers, turning identity verification costs into a fixed line you can actually forecast.

Who this is for — and what it’s not. For fintech founders, product managers, and finance leads evaluating identity verification vendors — specifically those who have been surprised by KYC invoices higher than their onboarding volume would suggest.

Not a technical guide to KYC flows or a comparison of verification accuracy. For a full overview of KYC software options, see Best KYC Providers; this article is the billing model “how and why.”

Why “Pay-Per-Completed” KYC Pricing Drains Your Budget

Most vendors bill per completed session, meaning you are charged the moment a user submits a verification attempt, no matter the outcome. You pay the same credit for a clean approval, a rejected fake, an expired document, and a session a fraudster abandons. The cost sits on attempts, not on customers. That matters because the law does not allow you to skip unprofitable attempts. Under Section 326 of the USA PATRIOT Act, FinCEN’s Customer Identification Program rules require you to identify and verify every customer before account opening, and the EU’s Anti-Money Laundering Directive framework (now consolidated under the incoming AMLR) imposes the same customer due diligence duty across the bloc.

Most vendors bill per completed session, meaning you are charged the moment a user submits a verification attempt, no matter the outcome. You pay the same credit for a clean approval, a rejected fake, an expired document, and a session a fraudster abandons. The cost sits on attempts, not on customers. That matters because the law does not allow you to skip unprofitable attempts. Under Section 326 of the USA PATRIOT Act, FinCEN’s Customer Identification Program rules require you to identify and verify every customer before account opening, and the EU’s Anti-Money Laundering Directive framework (now consolidated under the incoming AMLR) imposes the same customer due diligence duty across the bloc.

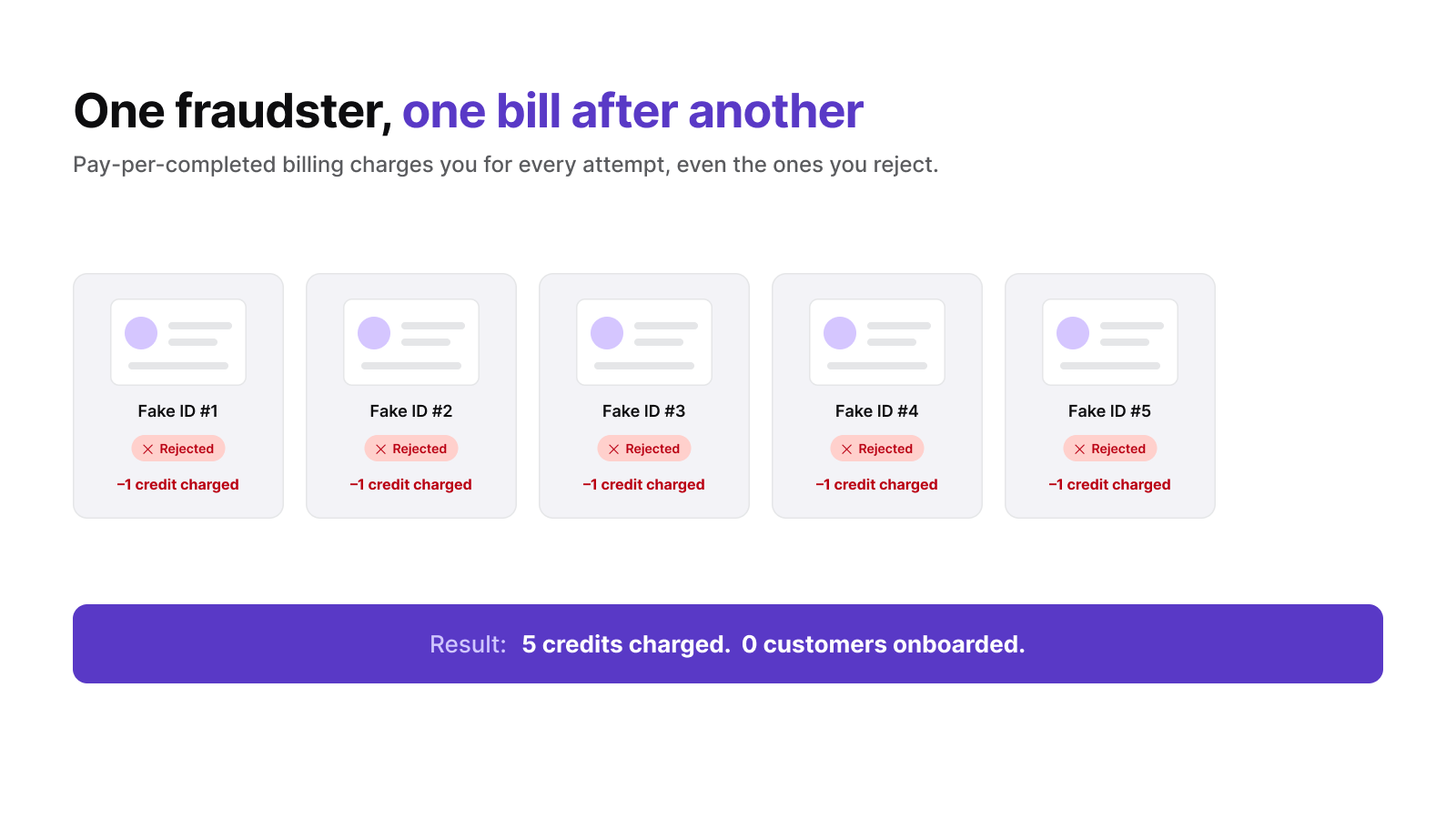

You are obligated to run the check on everyone, so a per-attempt model taxes a process you are not allowed to avoid. Fraud turns that tax into a real leak. A single bad actor cycling through 5 to 10 synthetic or stolen IDs to brute-force your digital onboarding does not cost you one credit but 5 to 10, and your system correctly rejects them all.

- You pay to lose. Every rejected fraud attempt is money spent confirming someone is not a customer.

- Fraud rings scale the cost. Coordinated attacks multiply your bill precisely when no revenue is attached to it.

- The budget becomes unforecastable. Two months with identical signups can carry very different verification costs depending on how many bad actors probed your funnel.

Related: Synthetic Identity Fraud and How to Detect It

Automate your KYC process

iDenfy verifies customers from 200+ countries in seconds. AI-powered, compliant, and trusted by 1,000+ companies.

Explore KYC SolutionHow High Rejection Rates Inflate Your True Cost Per User

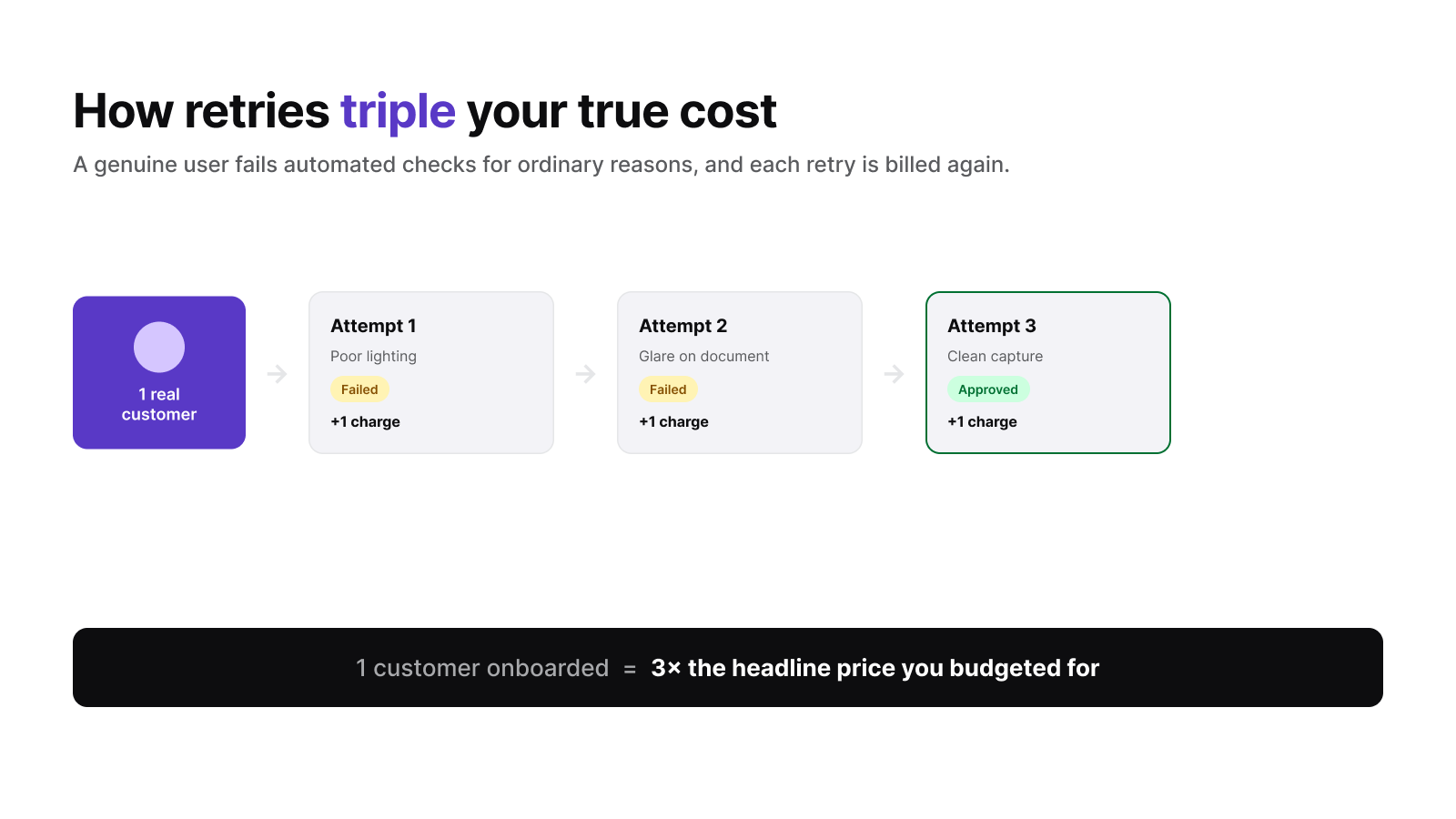

Your true cost per onboarded customer is total verification spend divided by the number of approved users, not the price on the vendor’s rate card. Rejected and repeated attempts sit in the numerator, so the more friction your flow creates, the further your real cost drifts above the advertised per-check fee. The drift is not driven by fraudsters alone. Legitimate, non-technical users fail automated checks for ordinary reasons: poor lighting, a thumb over the document, an outdated phone camera, or a glare-covered hologram. Each retry is billed as a fresh session under a pay-per-completed model.

Your true cost per onboarded customer is total verification spend divided by the number of approved users, not the price on the vendor’s rate card. Rejected and repeated attempts sit in the numerator, so the more friction your flow creates, the further your real cost drifts above the advertised per-check fee. The drift is not driven by fraudsters alone. Legitimate, non-technical users fail automated checks for ordinary reasons: poor lighting, a thumb over the document, an outdated phone camera, or a glare-covered hologram. Each retry is billed as a fresh session under a pay-per-completed model.

Here is the math executives miss. If a genuine user needs three attempts to pass, you have paid three credits to onboard a single customer, so your effective cost on that account is triple the headline price. Across thousands of signups, that gap is the difference between hitting your user acquisition cost target and blowing past it.

- Light-touch flows hide the problem. A 2% rejection rate barely moves your average, but a poorly tuned flow at 20% or 30% quietly multiplies cost per user.

- Retries stack invisibly. Each re-attempt looks like a new line item, not a repeat of the same person.

- UAC takes the hit. Verification is part of acquisition spend, so inflated retry costs raise the price of every customer you keep.

If your onboarding is leaking budget on rejected and repeated checks, the fix is not just a cheaper per-check rate. It is a billing model that stops charging you for outcomes that never become customers. That is the model we built at iDenfy.

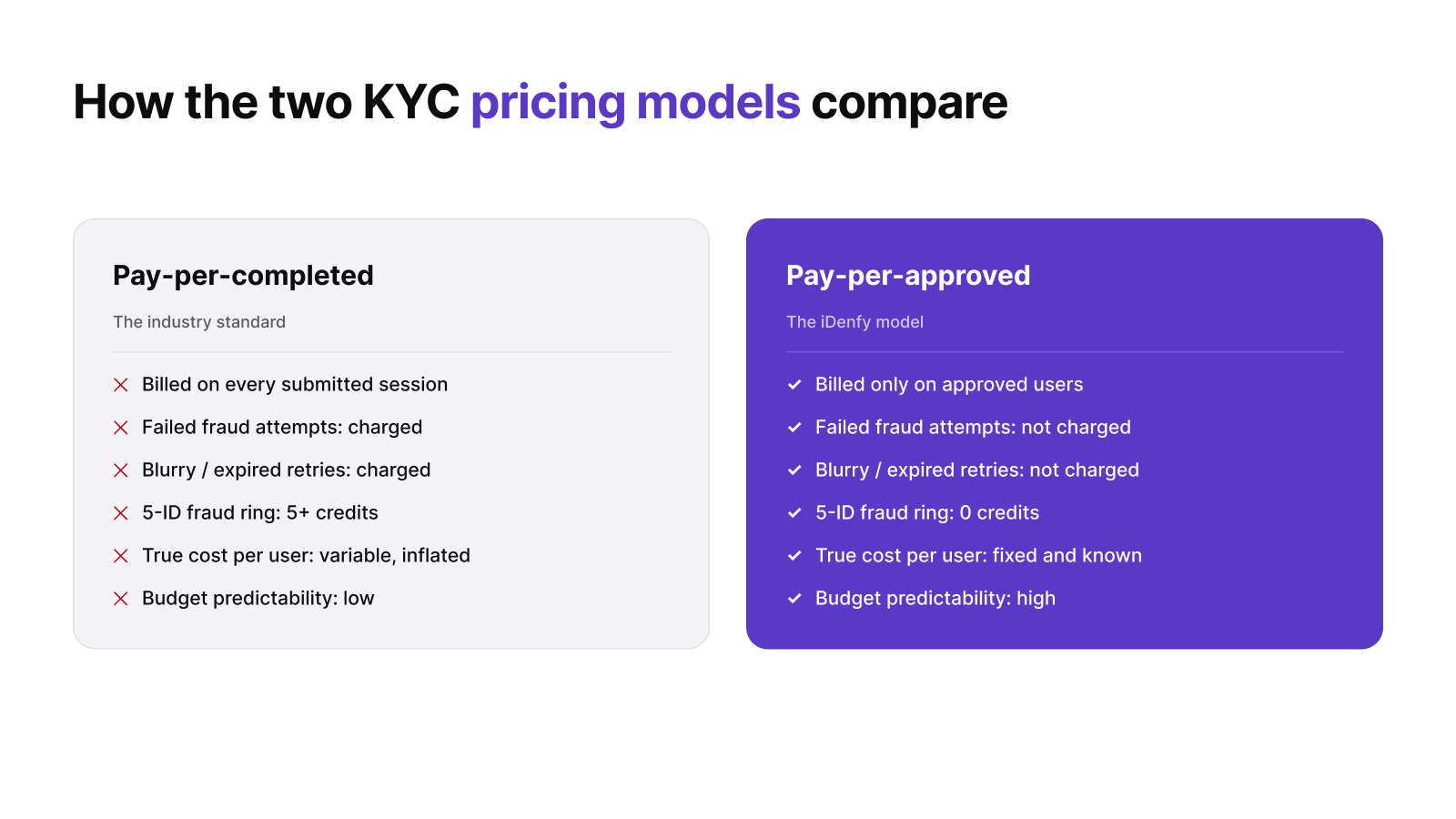

How the Two KYC Pricing Models Compare

The two dominant identity verification cost structures look similar on a quote and behave very differently on an invoice. The table below shows what each model actually bills you for.

The two dominant identity verification cost structures look similar on a quote and behave very differently on an invoice. The table below shows what each model actually bills you for.

| Cost Factor | Pay-Per-Completed (Industry Standard) | Pay-Per-Approved (iDenfy) |

|---|---|---|

| Billing trigger | Every submitted session | Only approved, verified users |

| Failed fraud attempts | Charged per attempt | Not charged |

| Expired/blurry document retries | Charged per retry | Not charged |

| Cost of a 5-ID fraud ring | 5+ credits | 0 credits |

| True cost per onboarded user | Variable, often inflated | Fixed and known in advance |

| Budget predictability | Low | High |

The practical takeaway: under pay-per-completed, your worst fraud weeks and your highest-friction user segments cost you the most. Under pay-per-approved, those same events cost you nothing because there is no approved customer attached to them.

The Pay-Per-Approved Model: Pay Only for Approved Users. Pay-per-approved means you are charged once, only when an identity is successfully verified and accepted. Fake IDs, expired documents, blurry uploads, abandoned sessions, and repeated fraud attempts are not billed. You pay for outcomes that turn into customers, and nothing else.

That changes how you plan. Because the only billable event is an approved user, you know your exact cost to onboard a customer before the quarter starts, and that number does not move when an attack hits or when a segment of users struggles with their camera.

“For me anyway, the idea for the premium is a bit more attractive, the idea itself. So you mentioned that Rejected are not charged as well.” — Head of Strategy at a European remittance platform

“iDenfy’s Pay-Per-Approved pricing model removed the risk of verification abuse and provided predictable costs, which was a major factor in our decision.” — Timur Gok, the Founder of Byteful (Read more at Byteful case study).

In practice, teams apply this by mapping verification spend directly onto their acquisition model. You take your approved-user cost, plug it into your UAC and lifetime value math, and get a clean per-customer figure with no fraud surcharge baked in. See the full breakdown on our KYC verification and pricing pages. Related: 5 Key Customer Onboarding Mistakes Costing Your Business Growth

Predictable ROI and Zero Wasted Spend

Predictable ROI is the commercial payoff: a fixed, known cost per approved customer that you can forecast, defend in a board meeting, and tie straight to revenue. There are no fraud surcharges, no retry penalties, and no surprise overage from a bad actor stress-testing your funnel.

- Forecastable budgets. Verification spend scales with real customers, not with attack volume.

- Cleaner UAC. Acquisition math stops absorbing the cost of users you never onboarded.

- Zero waste. Not a cent goes toward confirming a fraudster is a fraudster.

For a CFO, this removes a volatile, unforecastable line item. For a product manager, it removes the pressure to under-screen users just to protect the verification budget, because tighter screening no longer costs you more. This matters especially in AML-regulated industries where you cannot reduce screening to save money. Pay-per-approved removes the financial tension between compliance depth and cost. Related: KYC & AML Compliance: A Practical Guide

The Bottom Line

The hidden trap in KYC pricing is not the per-check rate on the quote. It is the volume of failed, fraudulent, and repeated attempts you quietly fund under a pay-per-completed model, all of which inflate your true cost per user and distort your acquisition math. A pay-per-approved model closes that gap by charging only for verified customers, so identity verification becomes a fixed, predictable cost instead of a variable one that spikes with every fraud attack.

The financial case is simple: you pay for customers, not for catching the people pretending to be them. Want a cost-per-approved-user number you can actually forecast? Let’s talk, and we will give you a free dashboard tour of how pay-per-approved verification works at iDenfy.