Picking the wrong KYC (Know Your Customer) onboarding software costs more than the licensing fee. The real damage shows up later – manual workarounds where the automation falls short, customers abandoning the process halfway through, compliance gaps that only come to light during an audit, and, at some point, the cost of moving to something else entirely.

Most teams don’t figure out what their current solution can’t handle until they’re six months in and the edge cases have started piling up. The point of this guide is to help you avoid that.

TL;DR

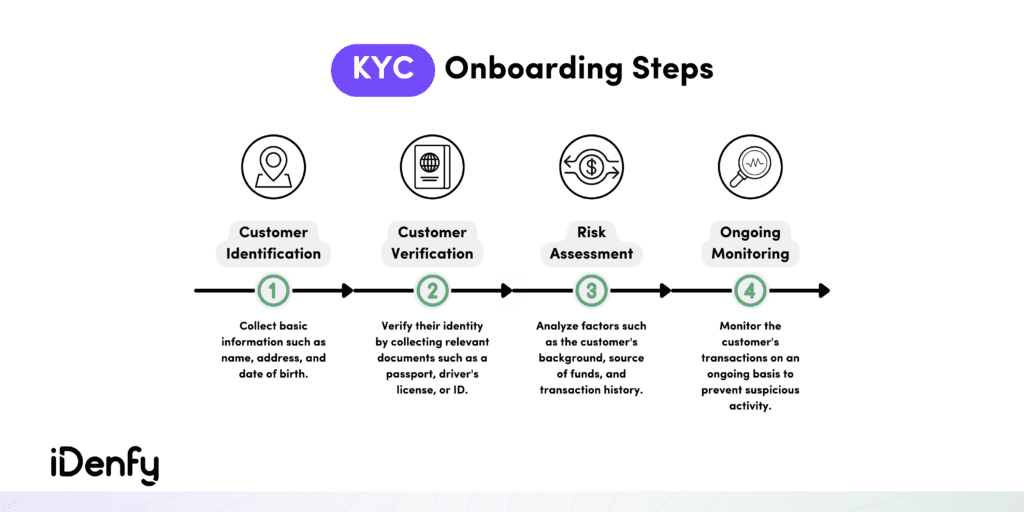

KYC onboarding can have a different workflow, depending on the platform. The exact KYC process typically involves collecting ID documents and proof of address (for example, in crypto to activate the user’s wallet), running background checks, such as screening for PEPs and sanctions (especially in higher-risk industries, like fintech), and assigning a risk score to identify and determine the result of the onboarding. Flagged, high-risk customers are often forwarded for manual review, and Enhanced Due Diligence (EDD) measures are applied. Low-risk customers go through a simpler onboarding flow. For that, a carefully chosen KYC onboarding software is required.

What is Know Your Customer (KYC)?

Know Your Customer (KYC) is the process of verifying customer identities when they register for the first time on an online platform. This is especially important for banking apps, crypto platforms, and other industries where there’s a higher risk of identity theft, money laundering, and other financial crimes. The KYC process is a security measure and a mandatory requirement for regulated entities. If a customer going through the verification doesn’t meet the minimum standards, banks can refuse to open an account or may even end the business relationship.

This is a bigger set of rules designed to ensure that transactions are transparent and not used for fraud or money laundering. And since most platforms are now monetized online, KYC onboarding is a typical process known to many internet users. Due to its wide adoption, users expect a good U/X during their ID verification process. This is achieved using KYC onboarding software. Otherwise, their journey with the brand or platform ends there. As a business, you want conversions and clients who don’t drop off during the first step of the onboarding.

So, in this sense, KYC onboarding isn’t a legal requirement; it’s more of a first impression that a user gets when they start using your services.

Key Highlights

- KYC onboarding is mandatory for AML-obligated entities. This includes banks, fintechs, crypto exchanges, iGaming operators, real estate platforms, insurance companies, some e-commerce platforms, etc., all of which must verify customers before granting access.

- Minimum data collected includes full name, date of birth, and address, supported by other, more jurisdiction-specific requirements (for example, like the SSN in the US)

- KYC onboarding differs based on the risk. That means standard CDD for most customers, EDD for high-risk individuals such as PEPs or those with adverse media alerts.

- Automation and KYC compliance software are the standard for competitive onboarding because AI-powered verification reduces manual review, lowers drop-offs, and enables real-time document checks, which users expect when registering for your services.

Automate your KYC process

iDenfy verifies customers from 200+ countries in seconds. AI-powered, compliant, and trusted by 1,000+ companies.

Explore KYC SolutionHow to Enhance the KYC Onboarding Process?

Compliance and conversion are often treated as competing priorities. But there are key points that you must have in mind when building an efficient customer onboarding process:

- Automation or KYC onboarding software, which cuts verification time and reduces the manual overhead your compliance team carries with every new customer.

- Customization, which lets you apply the right level of scrutiny to the right customer and doesn’t over-complicate low-risk onboarding scenarios or under-serve high-risk ones.

This matters because onboarding is where you lose customers before they ever become customers. A process that’s slow and asks for more than it needs to will quietly destroy your conversion rate. So, the practical fix is for you to work with a KYC onboarding service provider that lets you configure the flow.

Where Should I Start When Choosing a KYC Onboarding Solution?

Before looking at vendors, it’s worth being honest about where your current process actually breaks down. KYC onboarding software gets sold as a fix for everything, but the underlying problems vary a lot depending on the business.

A neobank onboarding retail customers across multiple European markets is dealing with different pressure points than a crypto exchange handling high-volume account creation or a B2B fintech verifying corporate clients across Southeast Asia. The platforms that work well for one don’t always work well for the others.

Some questions worth answering before you open a single sales deck:

-> Where is the drop-off happening in your current onboarding funnel? Is it at document upload, identity verification, or liveness checks? If customers are abandoning at a specific point, that’s a signal about what needs fixing – and you need a solution that addresses that specific friction, not just the category.

-> What’s your regulatory footprint? Operating in multiple jurisdictions means dealing with multiple regulatory frameworks simultaneously. Some KYC platforms are built around a single market (typically the UK or EU) and treat international coverage as an add-on. If you’re genuinely multi-jurisdictional, that limitation will catch up with you.

-> What does your tech stack look like? A platform that requires significant custom development to integrate with your existing infrastructure is a bigger investment than its licensing fee suggests. The quality and completeness of the API matter as much as the features it unlocks.

With AI, companies can carry out KYC checks more accurately, quickly, and efficiently, reducing the need for manual intervention. As specialized KYC software allows for real-time data verification, it reduces the possibility of errors, ultimately helping companies save time and resources. A proper KYC solution and automated onboarding system can reduce drop-offs during the onboarding process by automatically capturing the necessary document fields.

Additionally, AI-powered identity verification solutions provide more detailed customer risk profiling, which helps businesses identify high-risk customers and take appropriate actions.

The 4 Core KYC Software Capabilities that Matter

There’s a long list of features that KYC software vendors will highlight in demos. Most of them matter less than the three or four that determine whether the product actually works in your environment.

1. Document Verification Accuracy

The headline accuracy rates quoted by vendors are often measured on clean, high-quality document scans. Real-world onboarding involves photos taken on aging smartphones in poor lighting, documents with minor physical damage, and users who don’t follow instructions precisely. Ask vendors how their accuracy holds up in adverse conditions – and ask for data, not assurances.

2. Liveness Detection and Biometric Matching

Deepfakes and spoofing attacks have moved fast enough that a standard liveness check doesn’t do much anymore. Passive checks – where the system analyses a photo or short video – are increasingly easy to fool. Active liveness, where the user has to respond to real-time prompts, is harder to beat. Ask the vendor how they track new attack methods and what they’ve actually done about them recently.

3. Sanctions, PEPs, and Adverse Media Screening

Every platform screens against sanctions lists and PEP databases – that’s not a differentiator anymore. What actually varies is how many lists they cover, how frequently those lists get updated, and whether adverse media screening pulls from sources outside English. If you’re onboarding from higher-risk regions or operating in regions where regulators are paying close attention, those are the questions worth asking.

4. Automation Rates and Human Review Workflows

No KYC platform automates 100% of cases. The more relevant questions are: what proportion is automatically cleared, what proportion requires manual review, and how the platform handles the grey zone between them. A platform that automates 85% of cases but creates a chaotic queue of exceptions is less useful than one that automates 75% but routes the remainder intelligently to the right review tier.

What You Should Know About KYC Compliance Coverage Across Jurisdictions

KYC requirements vary considerably from one market to the next. GDPR in the EU, FCA expectations in the UK, FinCEN rules in the US, and MAS guidelines in Singapore each have their own standards for data handling, verification, and record-keeping, and they don’t always point in the same direction.

At a minimum, companies must obtain the following set of data during customer onboarding:

-> Full name

-> Date of birth

-> Address

Depending on the jurisdiction, companies may collect additional data points on top of the basics. In the US, that typically means a Social Security number; in the UK, a National Insurance number. Whatever is collected, the company is responsible for verifying that the data is accurate and belongs to the customer who provided it.

KYC and its Relation to AML

Adhering to Anti-Money Laundering (AML) compliance necessitates this process. It typically involves requesting the individual to provide a government-issued ID document (which is the document verification part) and a selfie (as a biometric check). As an alternative, companies can ask their customers to provide the mentioned PoA, and so on.

A platform built for multi-market use should have dedicated compliance coverage in each jurisdiction, not a generic framework with some localization bolted on. Ask which regulatory frameworks it’s actually certified or audited against, and how it handles requirements that conflict across borders – because they do, more often than vendors tend to acknowledge.

The question worth asking directly: when a regulatory requirement changes in a specific market, what happens inside the platform, and how long does it take? Regulation moves constantly, and if the vendor’s update cycle can’t keep up, that becomes your problem.

Related: What are the 3 Steps to KYC?

Why You Should Test the KYC Conversion Rate Before Committing to a Software Solution

There’s a tendency to treat compliance and conversion as opposing forces – the stricter the verification, the more customers you lose. That framing is outdated. The better way to think about it is that a poorly designed KYC experience is a compliance failure in its own right, because it pushes legitimate customers away and creates pressure to lower standards just to hit onboarding targets.

The best KYC platforms are designed to meet both requirements. They use:

-> Progressive disclosure (asking for additional information only when risk signals warrant it)

-> Adaptive flows that adjust based on the customer’s device and location, and clear in-product guidance that reduces document rejection rates due to user error rather than actual fraud.

When evaluating platforms, ask for conversion data – not overall pass rates, but completion rates at each step in the funnel. A platform might have a high overall approval rate because it’s overly permissive, or a high pass rate for people who complete the flow, because a huge proportion of users abandon before finishing. The number that matters is the percentage of users who start the KYC process and complete it successfully.

How Can I Assess the Quality of KYC Software Integration, Scalability, and Ongoing Support?

There are a few areas that don’t always get enough attention during KYC vendor evaluation. That’s why you need to assess a few important factors before finalizing your decision. They revolve around the ease of integration or important bonus points, like the vendor offering full-time support in case any issues arise.

So, always review the software and check if it offers:

High-Quality API and Documentation

This sounds like a technical detail, but it determines how much custom development your engineering team needs to do and how brittle the integration will be at scale. Poor API documentation is a leading indicator of integration headaches down the line. Ask your developers to review the documentation before you sign anything.

Proper Scalability Under High Volumes

If you’re planning a product launch or operating in a market with seasonal spikes, you need to know how the platform performs under pressure. Vendor case studies tend to feature steady-state operations. Ask specifically about performance during high-traffic periods and how SLAs are maintained.

Audit Trails and Reporting

Compliance teams need to demonstrate to regulators that their KYC process was correctly followed in specific cases. The quality of the audit trail – how much detail is captured, how it’s stored, how easily it can be retrieved – varies considerably between platforms. A platform with a weak audit trail creates problems the moment you face a regulatory inquiry.

Onboarding and Ongoing Support

The implementation phase of a KYC platform deployment is often more complex than anticipated. Understanding what support the vendor provides during the initial rollout – dedicated implementation resources, response times for technical issues, escalation paths for compliance questions – is worth clarifying before you commit.

Red Flags to Watch For When Evaluating a KYC Vendor

Some warning signs that are easy to miss in the evaluation process:

-> Vendors who are reluctant to share accuracy and data broken down by document type or region. Headline numbers are easy to construct in a favorable way; granular data is harder to game.

-> Platforms that haven’t updated their anti-spoofing capabilities in the past 12–18 months. The threat landscape moves quickly. A vendor that isn’t keeping pace with attack evolution will leave you exposed.

-> Contracts that are ambiguous about data ownership and deletion rights. Your KYC data belongs to your customers – and to you. If a vendor’s contract makes it difficult to export or delete data, that’s both a GDPR risk and a negotiating leverage issue if you ever want to switch providers.

-> An implementation timeline that seems implausibly short. A vendor promising a full go-live in two weeks for a complex integration is either being unrealistic or planning to cut corners. The budget for implementation is taking longer than the vendor’s optimistic estimate.

Instead, look for:

🟢 Software’s adaptability and high-level functionality, with multiple built-in tools helping you maintain complete compliance with both KYC and AML requirements. This is important when stricter onboarding workflows are required, not just a standard ID check, in industries like iGaming or crypto.

🟢 Customization options and easy integration, especially with existing frameworks and compatibility with your internal risk assessment appetite.

🟢 Options to automate various compliance processes for a higher KYC conversion rate and better overall end-user experience. This means different workflows for different client types. Low-risk users shouldn’t need to go through complex, multi-step workflows.

🟢 Optimized costs for the business and a simplified dashboard experience for compliance specialists who are responsible for managing KYC processes (especially if manual reviews are conducted on edge cases or Enhanced Due Diligence (EDD)). Deny/failure reasons should be shown properly and as a way to keep up with reporting obligations if suspicious activity is detected.

Conclusion

Most organizations shortlist two or three platforms before making a final decision. At that stage, a structured pilot in a controlled environment – using real transaction data where possible – is worth the time it takes. Demos show you what the product can do in ideal conditions; people will show you what it does in yours.

What should drive the final decision: compliance coverage in your specific markets, accuracy and conversion numbers you can actually verify, how clean the integration is, and whether the vendor has genuinely kept pace with regulatory changes – not just claimed to.

Underneath all the feature comparisons, this is a risk management decision. Get it right, and you’ve got less compliance exposure, a better onboarding experience, and something that scales. Get it wrong, and you’ll feel it in all three places, usually when the timing is worst.

Take the evaluation seriously. The shortcuts taken here tend to show up later, when fixing them is considerably more expensive.