Money laundering is the process of integrating dirty money, which is illegally obtained through various methods, such as organized crime and its associated activities, and cleaning it to appear legitimate. The primary challenge with money laundering is its complexity, particularly for financial institutions responsible for monitoring transactions to prevent it. A large portion of money laundering is successful and goes undetected, often through channels like real estate, art, and other tangible assets, with some estimates suggesting that up to 50% goes unnoticed.

Like many different businesses and industries, not only financial institutions, are now strictly regulated and need to comply with the Anti-Money Laundering (AML) framework. Sophisticated schemes are used by criminals who know the techniques of how to use their dirty funds without raising suspicion. Some methods are less deceptive than others, but if illegal money is used and its true source is concealed, it’s a serious crime, and that crime is money laundering.

In this blog post, we look into how criminals succeed with money laundering, examine real-world money laundering examples, explain how AML compliance addresses the issue, and share ways to detect and prevent this crime.

What is Money Laundering?

Money laundering is an illegal process that involves criminals using their illegally obtained money and making it look “clean” and appear legitimate. That’s why the laundering part means that the “dirty” cash was cleaned, and any potential links that could trace the criminals and their true source of funds are erased. To solve this issue, global regulatory organizations have created AML laws and regulations, which require companies to implement their own internal policies and AML processes designed to stop such illegal activities.

Money laundering happens in different ways. For example, since criminals don’t want to raise suspicion, they find ways to make the money look like it came from a proper, legal source. For example, they can use other entities, aka businesses they own themselves, to launder money. That’s why a huge part of AML compliance is Know Your Business (KYB) verification, a process designed to help assess and verify other companies, determining if their operations are legitimate and compliant.

For years, only individual client verification, known as Know Your Customer (KYC), was required. However, regulators began to spot serious gaps in the system, such as the use of shell companies for money laundering. To address these risks, KYB verification was introduced. However, there are multiple risk factors that increase the chances of money laundering. For example, the use of cross-border transactions or cryptocurrencies, or digital assets with a nature of anonymity, also doesn’t help when it comes to money laundering.

KYC for crypto and blockchain

Stay compliant with evolving crypto regulations. iDenfy helps exchanges and DeFi platforms verify users globally.

Explore Crypto SolutionHow Does Money Laundering Work?

Money laundering is appealing to criminals because they are driven by the goal of earning more and making a profit. To make the money appear legitimate, criminals move it through financial institutions. This works because fraudsters often profit from drug trafficking or other financial crimes, and they often end up with large sums of cash.

Money laundering is based on funneling the illegally obtained money into the legitimate financial system. With this process, criminals aim to:

- Hide the origins of illicit funds so they can be used without drawing attention to the crimes behind them.

- Turn illegally obtained money into assets that appear to come from lawful sources.

Money laundering negatively impacts not only the financial institutions that are used as channels for cleaning the money but also the general financial system. It also helps terrorists, drug traffickers, and other types of criminal organizations to expand their operations and weaken the broader economy.

Three Stages of Money Laundering

Money laundering typically consists of three main stages. While these steps may sometimes overlap or repeat, they generally include:

1. Placement

It’s the first and most vulnerable stage for criminals, as it involves moving large amounts of illicit cash into the financial system without attracting attention from authorities or banks. To avoid detection, criminals often break the money into smaller, less suspicious amounts. This can include methods like depositing funds into offshore accounts or using other tactics to begin disguising the origin of the money.

Common placement techniques include:

- False invoicing, when no real goods or services are exchanged.

- Smurfing or making multiple small deposits below AML reporting limits.

- Buying high-value items like art or luxury goods to later sell for clean money.

- Moving illicit funds through foreign exchange markets, especially in less-regulated areas.

For this reason, to prevent money laundering, regulations like the Bank Secrecy Act (BSA) mandate that financial institutions maintain records of cash purchases and need to report cash transactions over the $10,000 threshold. All red flags ned to be investigated, while detected suspicious activity needs to be reported via a Suspicious Activity Report (SAR).

2. Layering

The second stage involves moving illicit money through a series of complex and often fraudulent transactions to conceal its origin. The goal is to mix the dirty funds within the financial system and erase any clear audit trail that could link the money back to illegal activities. This process of repeatedly moving and disguising the money is why it’s called “layering.”

Common layering examples include:

- Using the stock market to move illicit money.

- Using shelf or shell companies to launder funds discretely, often through tools like real estate.

- Converting cryptocurrency and transferring it across different blockchains (also known as the chain-hopping method).

- Mixing and tumbling transactions across multiple exchanges to obscure their origin.

3. Integration

In this final stage, criminals mix illegal funds into the legitimate economy. To remain lowkey and undetected, fraudsters might even pay taxes and accept financial losses. This helps them avoid raising suspicion with tax authorities and law enforcement. The main idea still remains that what makes integration structurally difficult to prosecute is definitely not the sophistication of any individual technique. It’s the fact that by this stage, proving criminal origin requires reconstructing the placement and layering chain (often across multiple jurisdictions with different legal frameworks and limited data-sharing), while the launderers need only to maintain a plausible legitimate explanation for funds that, on paper, look entirely clean.

For example, a launderer borrows their own layered funds back from an offshore entity they control, repays with legitimate business income, and in doing so produces an entirely credible financing history complete with loan agreements and interest records. Often, they reinvest laundered money by buying businesses and generating legitimate income, which helps continue the laundering cycle. The money then becomes economically functional, successfully helping criminal networks to legitimate entity structures that are entirely built on dirty cash.

Related: 3 Stages of Money Laundering Explained

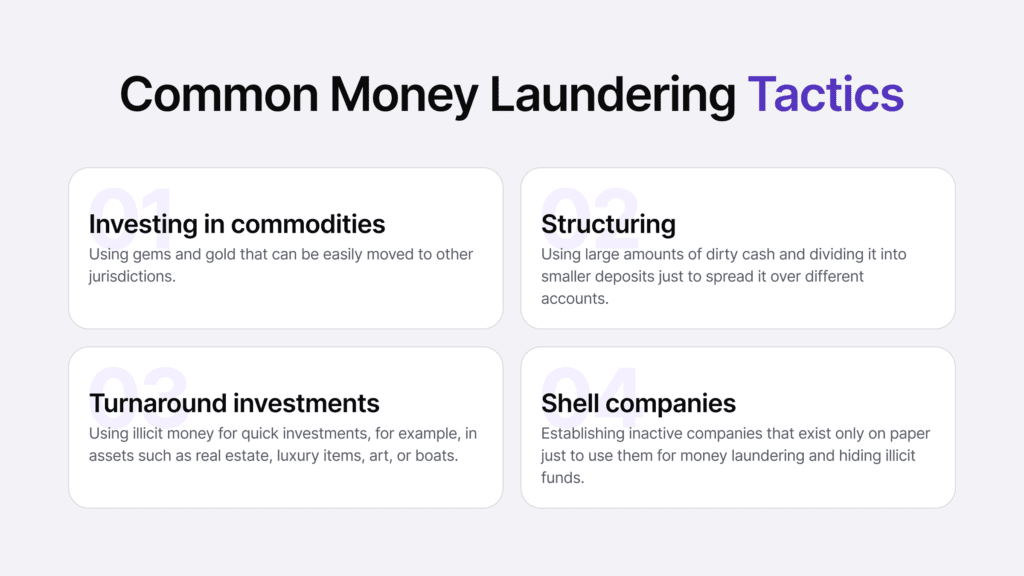

Common Types of Money Laundering

Money launderers often use:

- Smurfing. This involves breaking large sums of illegally obtained money into smaller transactions across multiple different accounts below reporting thresholds to avoid getting flagged.

- Gambling. Money laundering occurs in both physical and online casinos. Usually, a fraudster buys chips or credits with dirty money, plays through some wins and losses, then cashes out and cleans the illicit funds.

- Loan-back schemes. You can say that it’s an elegant integration technique. It means that the launderer is borrowing their own illicit funds back from an offshore entity they control. The offshore entity, holding layered funds, extends a loan to a legitimate domestic business or individual. The borrower (keep in mind that they’re the same beneficial owner) repays the loan with interest through normal business activity. The repayments are tax-deductible as business expenses with a clean financing history that, at first glance, looks entirely normal.

- Trade-based laundering. This form of money laundering is based on the opacity of international commerce (for example, the launderers use forged invoices, fake item quantities, and dual-use goods) that creates legitimate-looking transaction records. They move value across borders under the cover of ordinary trade. The money is also distributed across multiple accounts or individuals to avoid triggering AML flags.

- Cash-intensive businesses. This happens when criminals invest in businesses that are based mostly on cash, such as vending machines, and can be both a form of passive income and a source to mix into the legitimate financial system.

Once the money appears clean, criminals can use it freely. This blurs the line between illegal funds and legitimate wealth. But criminals rarely stop here; they often repeat their tactics, continuing the cycle by reinvesting the funds by buying businesses and generating legitimate income through salaries to keep laundering money.

Related: Examples of Money Laundering and Prevention Methods

What is Electronic Money Laundering?

Electronic money laundering is basically what it sounds like. It’s the same money laundering, just based on the use of digital financial infrastructure. This can be as simple as online banking or different payment platforms, including services like peer-to-peer (P2P) transfers, and, obviously, the king in this category — crypto. Due to the payments being made in seconds, even for cross-border transactions, dirty funds can be laundered faster.

They simply stage into a timeframe that “performs better” than traditional currencies. That’s why it’s been known for years now that crypto introduces additional complexity (yet, not because it’s more anonymous) because of the ability for launderers to mix services, chain-hop between assets, etc. That’s when it becomes harder to distinguish such activity from ordinary consumer behaviour at the volume of electronic payment methods.

Additionally, criminals use extra tools that hide their identities and can make it more complex for internal Trust and Safety teams to detect fraud. For example, proxies that hide the user’s IP address can be used for fraud, including money laundering, as a way to obscure internet activity, making the integration stage of money laundering difficult to trace. However, the same principle applies to various use cases.

What is Anti-Money Laundering (AML)?

Anti-money laundering (AML) is a set of regulatory frameworks that are designed to help companies establish a system that constantly works towards identifying and preventing all sorts of fraudulent activities, including fraud and financial crimes. In this sense, AML’s goal is to combat money laundering and other related crimes through a unified system, both on the national and international levels.

Aside from standard AML processes, like monitoring user transactions and reporting suspicious activity (if detected), there are major regulatory bodies like the Financial Action Task Force (FATF) and its 40 Recommendations that help regulated entities shape their in-house measures and tools for an effective AML program.

An AML system includes various steps. In fintech, banking, crypto, and other regulated industries, this means: vis tiek braukia

- Know Your Customer (KYC) verification. Verifying customers and business partners through KYC/KYB procedures before and throughout the business relationship.

- Know Your Business (KYB) verification. This is the initial onboarding process for corporate entities, but it includes more elements (such as identifying the true beneficial owners behind legal entities), compared to a standard KYC check on individual clients.

- AML screening. This includes screening clients against different AML databases: PEPs and sanctions, global watchlists, adverse media, and others, sometimes doing an extra check, like a criminal background check, depending on the concrete use case.

- Transaction monitoring. This includes using automation to constantly run checks on customer behaviour, potentially identifying anomalies and filing suspicious activity reports (SARs) where required.

- Keeping accurate records of customer identities and financial transactions.

What are Money Laundering Red Flags?

Money laundering red flags (also simply known as “AML red flags”) are signs of suspicious behavior. It’s not necessarily automatically straight-up fraud, yet a sign of potential illicit activity. Often, businesses use AML software that detects such signs automatically since a human analyst isn’t capable of manually reviewing thousands of transactions or behavioral signals in real-time. Suspicious activity can be an atypical move from the customer’s side that doesn’t match their risk profile and typical, daily behavior.

Skilled fraudsters know the tactics that work and help them not get flagged by AML systems. That’s why they go below reporting thresholds, for example, and generally try to mimic proper legitimate activity, not to show up on these monitoring systems.

For example, it might be a person making the transaction who isn’t an official representative or party, or the bank notices multiple transactions between the same parties in a short period. Also, classic signs are third parties or intermediaries that are based in high-risk jurisdictions without a clear reason. When it comes to business ownership, it could be a listed director or representative who is underqualified and doesn’t appear appropriate for their role. It means the true owners behind the financial crime are hiding their identities.

Other red flags include large cash payments, unexplained third-party involvement, concealing ownership to obscure the origin of assets, frequent use of multiple accounts, setting up or managing nonprofits that may serve as fronts for laundering criminal proceeds, and transactions involving foreign bank accounts or virtual wallets from various jurisdictions.

How to Prevent Money Laundering?

Standard steps, such as verifying all clients and business partners using a proper AML program, help prevent financial crimes and being used as a money laundering channel. Most businesses that get tangled up in such schemes and need to pay legal fines are being used unknowingly. For this reason, constant screening, staff training, and monitoring internal controls to see if they work are needed.

Companies should also know which behaviors or types of transactions need to be treated with extra caution and additional due diligence measures. Complex business structures or challenges in identifying the true owner of an entity or purchases of high-value items like art, jewelry, or luxury goods need to be reviewed and monitored according to the company’s internal risk appetite. This is why regulatory authorities stress the importance of the risk-based approach to AML. When onboarding customers, automated identity verification solutions, such as iDenfy’s, are beneficial.

For example, fintech companies can prevent fraud and money laundering by implementing a more stringent KYC flow. This includes requesting the user to upload their government-issued ID photo and complete a biometric check. Sometimes, database verification is also used, where the user’s personal information is cross-checked against another government database to find potential matches.

Additionally, the institution often needs to screen the client against AML databases, such as PEPs & sanctions, global watchlists, and adverse media. For instance, a PEP, or a Politically Exposed Person, is always a high-risk customer, which means they need to be inspected more carefully than a low-risk customer without any potential links to financial crime. Screening negative news also helps detect ties to money laundering and other crimes, which should not be tolerated when forming new business relationships in certain industries.

At iDenfy, we help companies prevent money laundering and other financial crimes with our complete compliance and fraud prevention platform. Our AML toolkit includes services like:

- Identity verification (document and biometrics)

- Business verification (including features like EIN verification, AI data cross-matching & more)

- AML screening (PEP screening, sanctions screening & watchlist screening)

- Adverse media checks

- Bank verification (available in the EU)

- Other due diligence measures, such as address verification (like automated utility bill verification)

- Other fraud prevention solutions, such as phone or email verification (to collect extra information about the customer)

Book a free dashboard tour to see any of the mentioned solutions in action.