Many businesses are responsible for handling financial transactions, which automatically means one thing — identity verification and robust fraud prevention measures before the user is able to open an account. Since many companies now operate digitally, industries like banking, crypto, e-commerce, or insurance need to implement Know Your Customer (KYC) and Anti-Money Laundering (AML) measures. This might seem easy in theory, but in practice, risks like global operating markets, jurisdictional differences, cross-border transactions, and other risk factors all add a layer of complexity for those who are responsible for their business and their financial security.

However, with growing regulatory requirements, the demands from the customers are also reaching new heights, so companies simply need to prioritize a robust onboarding process, which often consists of multiple security checks that are done by the user and the internal compliance team. Customers now also care about data security and want to make fast and secure transactions. To meet these expectations, companies need to both validate documents and extract identity information, which also consists of verifying their bank account and financial background. This process is known as bank account verification.

In this blog post, we look into the main challenges businesses face when scaling and ensuring regulatory compliance and how bank account verification can help maintain security while enabling quick, seamless payments.

What is Bank Account Verification?

Bank account verification is the process of confirming if a user’s bank account is valid and if it really belongs to the owner, who is a legitimate customer. This process verifies that the bank account is valid, active, and belongs to the person claiming ownership, supporting compliance with KYC requirements. Bank account verification also checks if the account has sufficient funds for transactions like automated payments or deposits. Many fintech platforms and similar services use this process to help reduce fraud.

In general, the goal of the bank account verification process is to:

- Confirm a client’s account ownership.

- Verify their eligibility to open a new account.

- Check personal details (such as the account holder’s name, account number, and savings).

- Ensure that customers’ transactions are accurate and legitimate.

- See if the customer is eligible for further financial services (for example, stricter checks are conducted on investment platforms).

When opening a new account, customers are often required to complete identity verification (using ID documents and cross-checking with external databases like a credit bureau) or provide proof of account ownership, such as a recent bank statement, which is an additional check and can be considered a bank account verification measure.

Related: KYC in Banking Explained

Automate your identity verification

See how iDenfy helps 1,000+ companies verify customers in seconds with AI-powered KYC.

Explore iDenfyWhen is Bank Account Verification Required?

This process is vital for any platform that handles online transactions and is required when the business first transacts with a new customer. It’s used for online transactions, such as electronic funds transfers and similar financial activities. The main benefits of implementing this check are to prevent errors, protect the user from fraud, and ensure the overall accuracy of transactions.

So, like with a standard identity verification check, which is often the process of asking the user to upload a photo of their government-issued ID document or a selfie for biometric verification, bank account verification can be conducted at both the onboarding stage and updated periodically (if there are concerns about the user’s intent or signs of risky financial behavior).

Examples of Industries that Use Bank Account Verification

Companies in various sectors implement bank account verification because it’s fast and secure. Additionally, it often doesn’t require many steps or manual effort from the end-user in general.

For example:

- E-commerce (including subscription-based service providers), for verifying accounts that are monetized and need to process payments, for example, for selling or purchasing items on an online marketplace.

- Investment platforms, as a way to verify the source of funds and the overall financial history, before getting access to the platform’s services.

- Personal finance apps that use transactions as a behavioral biometric to assess and better recommend budgeting plans.

- Insurance providers that use this as a fraud prevention method, verifying policyholders’ accounts and confirming payouts.

- Lending/credit platforms that need to verify income and confirm account ownership before they can actually approve loans or credit.

For example, often, even less tech-savvy individuals remember their banking credentials and can log in to their account using the same info easily. That means the same method for accessing services is used on multiple occasions, not just for logging in to a fintech app.

What is a Bank Verification API?

Bank verification API (Application Programming Interface) is an open banking solution used for verifying account ownership and ensuring that the customer’s personal details match their bank account records.

APIs work like intermediaries and are very popular due to simplifying the development process. The rise of APIs in various industries has created terms like “API economy”, since companies that want to stay competitive now need to offer solutions that save time and boost efficiency, which makes solutions like a bank verification API beneficial.

Such an API is often used in fintech and other financial industries where firms deal with financial transactions and are required to conduct Know Your Customer (KYC) verification. A typical Bank verification API is used to automate both bank account and identity verification processes, making it more efficient for financial institutions to comply with regulatory requirements and still ensure a good experience for the end-user who’s signing up on their platforms.

How Does Bank Account Verification Work?

Bank account verification requires account holders to provide information to confirm their bank account (to verify that it’s valid), typically through an app or online banking. It works both for individual accounts and business accounts, verifying that the banking info, such as the IBAN, is legitimate. Financial institutions and payment service providers rely on bank account verification to minimize fraud risks. As part of this process, new account holders may need to complete identity verification using government-issued ID documents and database cross-checks (for example, with a credit bureau) or provide proof of ownership, such as a bank statement.

So, in other words, bank account verification works by confirming the account holder’s name, their account number, as well as the routing number through internal/external databases or other secure systems. Alternatively, many fintechs rely on automated third-party software providers or APIs, often for both identity and account verification, using real-time data via special APIs that provide bank account verification services.

Other popular approaches for bank account verification include:

- Using multifactor authentication to confirm the customer’s identity

- Asking the customer to verify their account by logging in through their bank

- Requesting the customer to upload a document, like a bank statement, to prove account ownership

- Sending small deposits to the customer’s account and asking them to confirm the exact amounts

How Long Does It Take to Verify a Bank Account?

It depends on the method. If it’s an API solution and integrated in a way that the check runs in seconds, as part of the user bank account creation process on a fintech, of course, this sort of business will prioritize security and user experience as much as it’s allowed based on compliance requirements. More traditional methods for traditional banks, such as verifying a bank account and then confirming certain changes, like exceeding an allowed payment threshold, require heading to a bank’s physical branch, which takes booking a meeting, so several days.

Common Bank Account Verification Methods

There isn’t a one-size-fits-all approach to this process, as financial institutions can tailor bank account verification according to their internal risk assessment and protocols. The main idea here is that this process should check the account number’s structure, verifying the account’s status. Consequently, verifying bank account data helps businesses guarantee that transactions are authorized and that customers provide accurate banking information.

We look into some popular bank account verification methods that businesses like to use in a more detailed manner.

1. Document-Based Verification

In general, document-based verification or document verification involves confirming the document’s authenticity to ensure that it’s accurate and genuine. In bank account verification, the account holder is asked to upload a bank statement or a voided check so that the system can automatically check it and confirm the account status, either approving or denying access to financial services.

Documents that can be accepted for bank verification include bank statements, letters from the bank, online banking screenshots, or cheques, as well as deposit tickets. However, handwritten notes, edited documents without personal information or a date, emails with sensitive info such as new credit card details, and email screenshots that aren’t approved by the bank are not accepted.

Customers are often asked to upload a document for KYC verification as well, which can be a passport, driver’s license, or ID card. Using this approach, the customer’s identity is verified to confirm that their name and account number match the provided personal data. Alternatively, some companies also have an in-house compliance team responsible for double-checking the software’s results. This means they manually assess banking and KYC documents to ensure accuracy.

Some use-case examples include:

- Crypto exchanges need bank account verification to enable users to buy and sell cryptocurrency or facilitate conversions.

- Lending platforms need to review documents and check the applicant’s financial background to ensure they’re eligible for a loan.

- Insurance firms must also review documents, especially before large claims, to ensure secure payouts to their customers.

2. Micro-Deposit Verification

This method is exactly as it sounds. When the account holder links their bank account to complete the verification, they’re sent a small amount, such as $0.15. After the micro-deposit is sent, the user is asked to enter the exact deposit amounts and activate their account. Investment platforms, payment service providers like PayPal, P2P apps, or some traditional financial institutions use this method because it’s reliable and helps them comply with KYC/AML requirements.

Companies choose this option because:

- It’s a less invasive method. The end-user is asked to check their transaction history, but it doesn’t require uploading any documents.

- It’s easily applicable. Many financial service providers can use this method in their particular use case.

- It’s a familiar routine. This method is known and trusted by the user, like other similar-styled methods, such as phone verification.

3. Database Verification

This method cross-references the client’s account details with a database, such as a credit bureau. In general, government-official databases provide reliable information, including credit accounts and payment records, which are valuable details used for bank account verification. Database verification uses the data pulled from the credit bureau and compares the customer’s account details with the existing data to find a match.

Often, companies implement AI-powered tools that can handle large data volumes and that already have multiple databases synced into their systems. This helps maintain a good user experience and quickly build a better, more accurate picture of the user’s financial history.

Some advantages that show why companies use this method are:

- Better fraud prevention. Since financial institutions juggle high-risk operations, like handling large transactions and personal information, fraud prevention measures are vital. With database verification, users are confirmed swiftly, reducing crimes like identity fraud or ATO fraud.

- Multi-layer approach. Cross-referencing information is considered to be a stricter security measure than, for example, a standard document check because documents can be forged, altered, and manipulated by fraudsters. To minimize fraud, companies combine various methods, such as KYC document checks (like passports or SSNs) and credit bureau checks for bank verification.

How is PSD2 Linked to Bank Account Verification?

EU’s PSD2, or the Revised Payment Services Directive (2015/2366), is a regulatory framework that governs electronic payments and financial data access across the European Economic Area. It requires banks and other account providers to open their infrastructure to licensed third-party providers via APIs, with customer consent (typically acquired through an extra pop-up window).

In this context, some bank account verification solutions, such as iDenfy’s, support this regulatory requirement. As a result, businesses can rely on standardized, secure infrastructure to verify bank account data in real-time. Which makes this a win-win situation, compliance-wise and end-user experience-wise. It works through open banking technology, where authorized providers can access direct, real financial data on behalf of the user and safely use it for verification.

For regulated businesses, this is beneficial for cases like source of funds (SOF) checks, payment method verification, and overall improvement of the internal risk assessment processes.

Limitations That You Should Know About Some Bank Account Verification Methods

A part of a successful bank account verification process consists of various elements, and one of them is knowing the challenges linked to each method. This helps adapt the process and choose the right service vendor based on your industry and its requirements.

For example:

- Using micro-deposits only means you’re verifying the account, not the customer. For example, if the fraudster has already taken over the account, this bank account verification method won’t help because it will only prove that the account exists and can receive funds, but not who controls it or is behind the transactions in real-time.

- Using bank statements without any sort of AI-altering and forgery detection technology. Even if you’re accepting bank statements using a vendor that extracts information and cross-checks it, you need to focus not only on speed but also on accuracy. Using AI, it’s relatively easy to create fake IDs, fake bank account statements, etc., so you need to detect fake documents as well.

- Relying on credit bureau checks as a single measure. It’s good for corporate entity onboarding and checking if the records match as part of KYB onboarding, for example, but it doesn’t prove full ownership or that the account is legitimate in real-time. Depending on the solution you’re using, bureau checks can also leave a footprint on the credit file, which customers notice.

The best option to solve these limitations is to use open banking and a third-party bank account verification service provider like iDenfy that connects to the customer’s bank via API and confirms account details against their own bank’s records in real-time. This is often paired with other methods, like KYC verification (document-based, selfie, database/credit bureau check, etc.).

Related: How to Improve KYC Verification? Tips For a Frictionless User Experience

Why is Bank Account Verification Important?

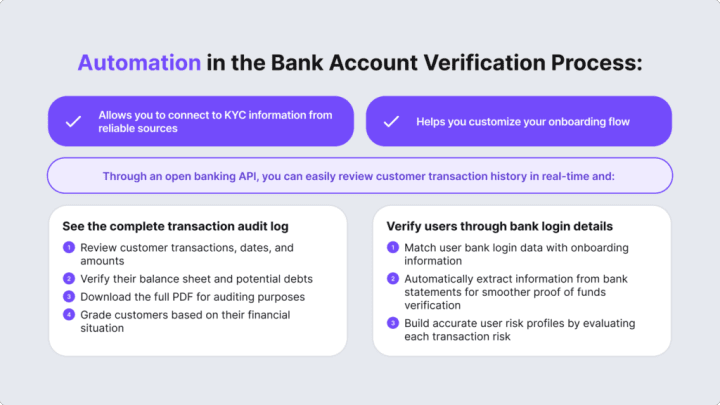

Bank account verification is the number one process that online payment processors need to build alongside ID verification in order to have a proper onboarding process. Some bank verification APIs allow companies to access detailed logs of customer transactions, including dates and amounts. This helps prevent financial crime and money laundering, for example, structuring, where transactions just below the reporting threshold are made into multiple bank accounts to avoid getting flagged and detected.

Through it, companies can verify their users and their banking information quickly while mitigating risks, such as identity theft or, even worse, money laundering and other financial crimes. Additionally, there are certain AML risks, such as cross-border transactions, that make verifying bank accounts, along with other methods, such as identity verification and transaction monitoring after the user is onboarded, vital.

This is a vital process in many industries that process payments, including e-commerce, personal finance apps, and more:

Automated Digital Payments

Bank account verification ensures the validity of the user’s data. If done right, the process is simple and secure, minimizing abandonment rates while ensuring regulatory compliance.

This is an important factor since many financial institutions need to find a way to integrate these security measures and collect/verify necessary information to maintain a user-friendly process. Incorrect user data can create a backlog, resulting in the need for lengthier manual checks and fees, along with additional disruptions to the business that handles automated bill payments, online purchases, direct debits, etc.

Minimized Chances of Financial Crime

Since multiple data points are checked through the digital onboarding process, such as name, address, financial background, sometimes credit report, or tax ID, the risks associated with the user are identified.

This information helps assess the user’s risk level, determining whether they’re approved or denied access to the financial services they’re applying for. The same principle applies to bank account verification. Businesses can keep track of accurate client risk profiles and prevent costly financial irregularities.

Related: Customer Risk Assessment — How to Do it Right

Ensured Regulatory Compliance

Bank account verification is one of the measures that is part of the KYC and AML framework. These regulations require companies to verify customers’ identities and bank account details before establishing a business relationship and to maintain transaction records to report any suspicious activity.

However, there are other measures, such as Customer Due Diligence (CDD) and assessing the risks associated with a customer, including continuously monitoring their accounts after they’re onboarded to the financial platform. Other country-specific regulations, such as the Bank Secrecy Act (BSA), require regulated entities to verify the source of funds (SOF) and monitor account activity to detect any unusual behavior.

How to Handle Challenges Linked to a Typical Bank Account Check

Like with any onboarding process or compliance-linked task where information needs to be submitted or checked, if manual input is required, there can be failures. If the client has outdated information logged with their bank, then the API won’t help if you’re cross-checking the information and it doesn’t match the one they had to provide earlier during their KYC verification. This isn’t fraud, more of a “soft fail”, similar to how fuzzy matching is used in AML screening for similar names (J. Smith against Jonathan Smith). Coverage gaps, especially linked to business accounts, are also a common challenge. Unsupported banks, joint accounts, business accounts where the verifying director isn’t the named holder, or recently opened accounts missing from bureau data, illustrate that.

Even a typo or a close-match name can lead to a drop-off. The same goes for sending everyone to document upload after a failed attempt to verify their bank account. This maximizes friction for cases a simple retry would resolve. So, depending on your risk appetite, it’s best to collect other behavioral signals and trigger stricter verification flows only if the risk is higher. Otherwise, low-risk customers should not have issues verifying their bank accounts. Don’t send everyone who failed their session instantly to the manual queue as well. This prolongs the waiting time and increases the workload for analysts.

How iDenfy Can Help with Automated Bank Verification

We’ve developed a fully automated Bank Verification solution that helps companies confirm the ownership and validity of a client’s bank account, ultimately verifying if they’re eligible to open a new bank account. Our open banking API helps swiftly analyze your customers’ transactions while verifying personal details, like the account holder’s name, account number, and other info, such as current savings, ensuring that transactions conducted by the customer are accurate and legitimate.

This option is supported on our KYC and KYB dashboard (enabled via Settings on iDenfy’s dashboard), allowing you to:

- Verify users in real-time by matching their bank login details with onboarding information.

- Access detailed logs of customer transactions, including dates and amounts, for full transparency.

- Connect to all major European banks with a single integration for streamlined onboarding. Our solution supports 2,500+ banks in 29 EU countries.

KYC/KYB Onboarding Flow Options with Bank Verification

Once enabled, the bank verification option becomes mandatory for all users before completing identity verification. In general, you can easily either:

- Request existing users to verify their banking details, or

- Start bank account checks during onboarding.

This helps verify bank account ownership and confirm payment legitimacy without implementing extra complex processes or software from additional third-party AML service providers.

This solution is ideal for high-risk industries where assessing financial risk is key to effective AML compliance. Extra options are available if you want to create a custom verification flow. We recommend checking concrete examples here.

For instance, you can mix and match between ID document, biometric, and bank account checks and, at the same time, adjust language preferences, device type, link expiration time, and other settings like KYC questionnaires for a smoother data collection process.

With our expertise in document verification, biometric verification, and now this comprehensive financial background check, our RegTech platform can help you ensure complete KYC/AML and KYB compliance, including a custom approach to your unique use case, such as adding features like Risk Assessment or Ongoing AML Monitoring.

Let’s talk for more info.