Simply googling another company and checking its website is not enough. In the same way, it’s not the best option to judge a company based on its incorporation date. A business that’s been registered for years might seem like a more trustworthy option to partner with than a relatively new startup. However, shelf companies, or those that are left dormant for years, create challenges for risk teams who conduct proper background checks. Mainly because this creates a gap in Anti-Money Laundering (AML) compliance. Why? The answer is opacity.

Companies can be left untouched for years, sitting on a “shelf” before being sold. Once that’s done, everything is inherited, including its legal history, which works as a legitimacy layer, especially for bad actors who want to hide under complex corporate structures. That’s how, at first glance, a shelf company can appear credible on paper. But without staff records, business transactions, or other business activities, for analysts, this creates challenges, especially when determining which red flags aren’t false positives within this blind spot.

So, how to determine when a shelf company is fake, and there’s no real business behind it, just a manufactured facade? We explain the reasons why fraudsters use this method to hide illegal funds or real beneficial ownership, and more, while giving you some extra tips for Know Your Business (KYB) compliance along the way.

Explanation of a Shelf Company in Simple Words

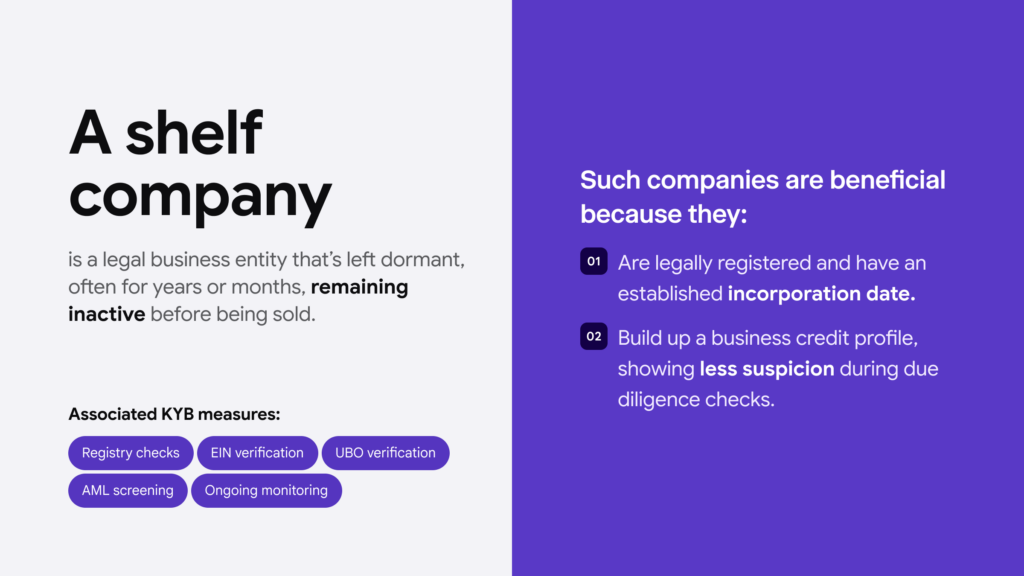

A shelf company is a legal entity that’s been registered officially, yet not used for a long time. In other words, it’s a company that was formed but did not conduct any business/trading activity. The main purpose of shelf companies is to sell them to someone who wants a company that looks older and more established, as a way to look more legitimate and credible for banks, investors, etc.

After buying the shelf company, the new owner updates key business information, such as address, director and ownership info, as well as other details, like the business bank account, and only then starts to use it. Since the entity was left to mature on a shelf, it’s known to be a shelf company, which pre-exists just to be sold.

Automate your identity verification

See how iDenfy helps 1,000+ companies verify customers in seconds with AI-powered KYC.

Explore iDenfyWhat Features Point Out That It’s a Shelf Company?

A shelf company is an entity that:

- Is legally registered

- Is sold through a company formation agent/broker

- Has never traded and has no assets or liabilities

- Has all official documents (such as a certificate of incorporation, and, in some cases, is in good standing)

For example, a company registered in 2016 can be sold in 2026 as an “established” firm that’s stable and more “trustworthy” due to it having been created a decade ago.

Related: A Secretary of State (SOS) API: What You Need to Know

Is it Illegal to Establish and Sell a Shelf Company?

No. It is legal to create and later sell a previously dormant company if it was not engaging in illegal activities.

In the context of regulatory compliance, shelf companies are bashed due to “corporate age manipulation,” which indeed falls in the grey area due to the potential risk and associated abuse. So, it can only become an illegal practice if used to commit fraud, such as money laundering or misrepresenting corporate history.

Who Can Set Up a Shelf Company?

Formation agents, legal experts and law firms, or even accountants can set up and maintain a shelf company as a way to sell it and gain profit. Having the right skills and knowledge allows such specialists to initiate incorporation, registration and tax filings without conducting business activity and leaving the entity dormant. This racks up a false history profile.

In general, such agents can cooperate with criminals and create shelf companies in advance only to support further crime facilitation. However, shelf companies can be bought legally by legitimate businesses and entrepreneurs who want to kickstart their operations faster.

Why Do People Buy Shelf Companies?

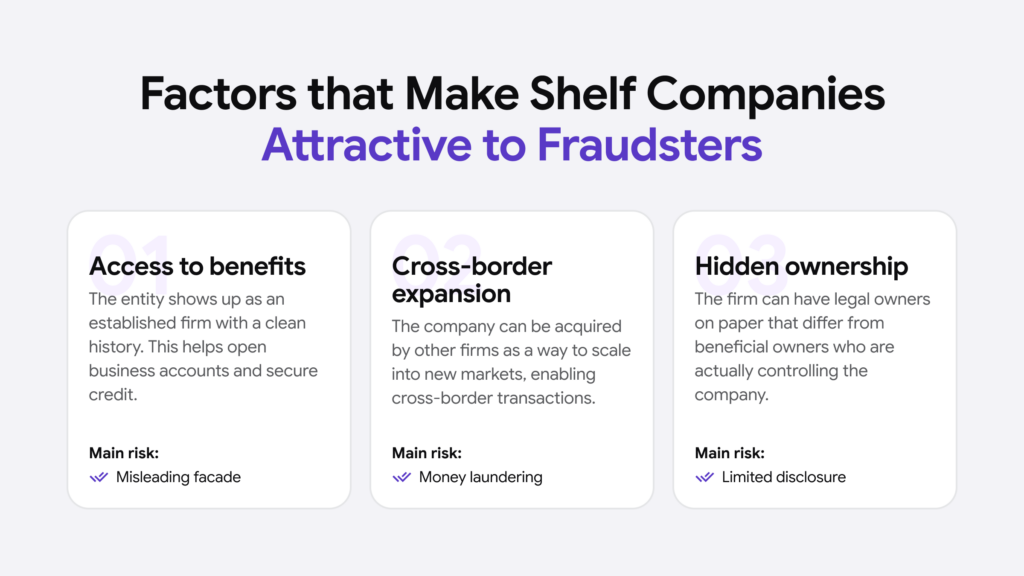

A shelf company manufactures a ready-made product, which can be attractive to fraudsters who want to create an image of stability, even in cases when there’s no real business behind the name. However, shelf companies aren’t automatically fraudulent entities, yet they are treated with caution and extra due diligence.

In general, a shelf company can be a good investment if you want to:

- Start business operations immediately and gain credibility (among other factors, like meeting thresholds for contracts and their age requirements)

- Access business benefits that require a company with a history (like opening bank accounts more easily or joining financial platforms with fewer checks)

This can help new business owners bypass certain regulatory thresholds, or make it easier to secure credit or even win contracts due to the created false “corporate longevity”. That’s why regulators, such as the Financial Crimes Enforcement Network (FinCEN) in the US, have been naming dormant and shelf entities as high-risk business structures in their AML guidelines.

What is the Difference Between a Shelf Company and a Shell Company?

A shelf company is a legally incorporated entity that was created without the goal of immediate use until it is purchased by a buyer. A shell company, by contrast, is a legal entity that exists on paper but conducts no genuine business operations; however, it can be actively used in this state (for example, occasionally holding bank accounts or investments), rather than simply waiting to be activated.

In other words, the defining characteristic of:

- A shelf company is held for a time before being sold. The price is based directly on the seniority of its incorporation date, which is the main commercial appeal.

- A shell company is holding assets for another company, often as a way to establish offshore accounts and avoid taxes. It often doesn’t have physical locations or commercial activity and real employees, but is still used to sign contracts or open bank accounts.

Both business structures are legitimate and can be used properly. For instance, companies hold shells to structure cross-border investments. However, both structures can be used for fraud. Shell companies are also known to be used as instruments for tax fraud, money laundering or sanctions evasion in AML compliance (because they can transact without revealing anything about the real ownership structure and who actually controls them).

Why Do Regulators Treat Shelf Companies as High-Risk Entities?

Shelf companies create the illusion that they are trustworthy. Regulators stress that this pre-made history is a scam in some cases. That’s why shelf companies can only be set up as a way to bypass security checks, Know Your Customer (KYC) and Know Your Business (KYB) onboarding processes in particular. For example, a legal and common practice is to acquire shelf companies in foreign markets to fast-track compliance with local requirements.

This helps open foreign bank accounts faster or apply for permits. However, that’s precisely why stricter due diligence is required for all potential partners (investors, suppliers, vendors, etc.). In the same sense, criminals can use these newly purchased shelf companies with a history to facilitate cross-border transactions and launder funds without triggering AML checks and deeper due diligence.

Related: The Main KYB Risk Factors You Should Know

How Criminals Use Shell Companies

A bad actor can abuse this structure and use a shell company for the wrong reasons, such as:

Hiding Ownership

Regulators see hidden company ownership as a risk because it helps criminals launder and hide assets with the real people behind the company (using nominee directors, for instance). Simply because it’s harder to track who is actually involved. In AML compliance, this breaks the audit trail, complicating the main task: identifying ultimate beneficial owners (UBOs) and all high-risk individuals linked to the company.

To this day, the notorious example of Panama Papers remains one of the books that showed how poorly regulated jurisdictions like the British Virgin Islands or Belize were used to cover a paper trail between a business and its true controller.

Tax Evasion

Criminals can use shelf companies as a channel to shift profits to low-tax jurisdictions. This is a grey zone as well due to regulatory diversity and different countries and their loopholes. For criminals and those who want to abuse the taxing system, this works in their favour.

The funds can be routed through a complex network of shelf companies, reducing the overall tax liability in the home country. So, in this sense, shelf companies work as a key layer in many aggressive tax structuring arrangements (profits are artificially shifted to low-tax jurisdictions).

Related: Tax Avoidance vs Tax Evasion: Legality Aspects & Detection Measures

Fraud

When it comes to fraud and shelf companies, they can be used for all sorts of illegal activities. If the shelf company is only established to be a fictitious, front company, it’s a relatively cheap way for fraudsters to buy it and commit further fraud. The older the registration date, the bigger the chances this will work as a golden ticket later in different types of financial fraud. This includes cases like forging documents and creating fake invoices for illegitimate services, as well as applying for business loans and pretending to be a legitimate entity.

For example, in fraudulent invoice schemes, this can be used like a tool to reactivate the dormant entity and then use it for billing for goods or services that are actually never delivered. And, naturally, a shelf company’s apparent corporate longevity helps it pass Know Your Vendor (KYV) checks.

Money Laundering

Criminals are drawn to shelf companies because they can immediately provide a look of a genuine business. This opens a door to other opportunities, like opening a business bank account to make large transactions (since the shelf company is bought with an old incorporation date).

Paired with an opaque ownership structure, this helps create the look of a “clean business revenue stream”. This helps disguise the origin of the dirty money, which can be integrated into the financial ecosystem. This approach is also used to bypass basic/surface-level transaction monitoring systems without triggering AML alerts.

What is the Main Challenge Linked to KYB Compliance and Shelf Companies?

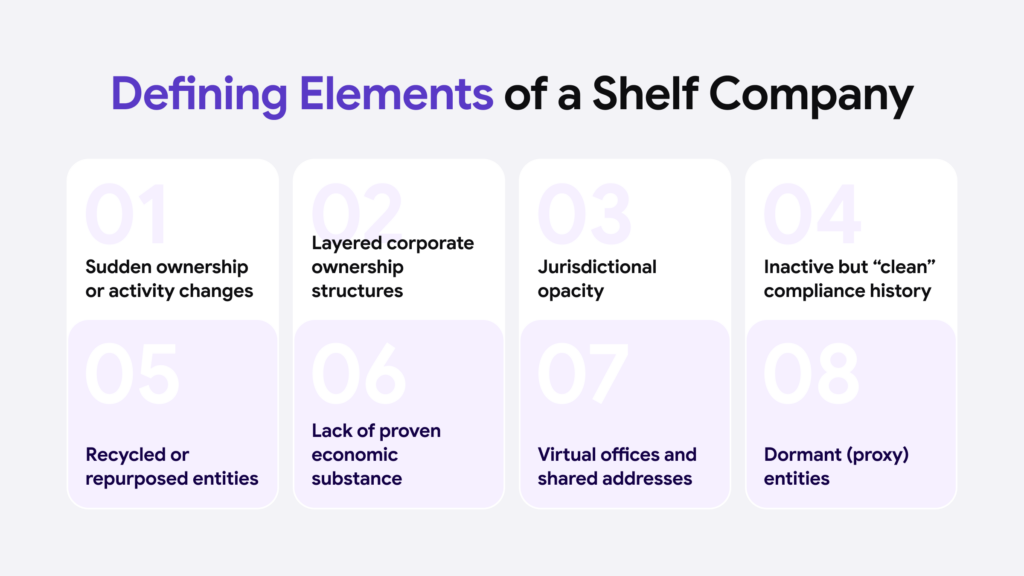

When assessing a shelf company for KYB compliance, it’s a challenge to find out who actually owns/controls the company. Shelf companies are bought from formation agents, and since they are formed by third-party agents, the buyers can shape the entity how they like, putting new, nominee directors on paper. The trail becomes complex, and the real beneficial ownership is harder to detect.

How it all becomes tricky is when:

- Jurisdictions with weak AML requirements are used

- Ownership chains are layered through suspicious shareholders and nominee directors

- Entity holding structures are specifically designed to obscure UBOs

A shelf company has no real transactions, no staff records, and no trading activity. That means there’s no baseline on where to start when assessing risk. In some cases, basic KYB solutions won’t find and automatically flag any risk signals. That means compliance teams need to review the operational history and even if it doesn’t show any red flags, run the Enhanced Due Diligence (EDD) workflow once it’s suspected that the company is a shelf entity during its onboarding.

Why Basic KYB Solutions Won’t Solve Shelf Company Verification Issues

Basic KYB software means one thing: it’s not configurable, not easily adaptable, doesn’t efficiently onboard different company types, might not support some markets or industries and might lack relevant sources, such as global/local government databases to cross-check KYB data. Often, such KYB solutions are built around basic company details and might not be the best fit for high-risk entity onboarding, like shelf companies (including edge cases, which need to be manually re-checked more thoroughly).

As a result, registration details or incorporation records aren’t enough to assess if the company doesn’t pose any risks and is not fraudulent.

What Your KYB Solution Should Verify to Detect Shelf Companies

Beyond verifying business registration data, a good KYB solution should help you:

- Check company directors. Frequent director changes or the use of nominee directors are red flags, which can lead to fraudulent schemes due to hidden ownership.

- Cross-check beneficial owners. This includes all UBOs and related individuals, preferably, at the same time, conduct AML screening and adverse media screening.

- Compare business activity. This means look into historical elements that would show tax activity, employee changes, or the entity’s trading history, not just its age.

- Review transaction history. AML red flags, such as large transactions or payments from poorly regulated jurisdictions, as well as sudden cash flows in a previously inactive company, should indicate the need for EDD.

Shelf companies have non-existent, only-on-paper operations that, with the wrong documents, are not enough to prove a business is illegitimate. Basic KYB workflows aren’t designed to spot sudden changes in ownership structure or automatically verify other sources, such as whether the company is still in good standing. If most of the KYB-related tasks need to be googled and checked manually, take it as a sign of a poor KYB solution. Real-time access and incorporation of global databases help you actually access and cross-reference important details like address updates, changes in ownership structure, or sudden shifts in business activity.

How iDenfy Can Help You With KYB Onboarding and Shelf Company Detection

iDenfy’s Business Verification is built to eliminate friction from corporate business entity onboarding. With newly added features, such as AI Company Reviewer, risks are detected automatically and provided to analysts working with the system in a concise and easy-to-understand format.

This helps:

- Apply EDD checks for edge cases and on high-risk clients without prolonging the onboarding process.

- Runs KYB-related checks 24/7, which means companies can be onboarded any time, during the weekends as well (as opposed to traditional KYB checks and human analysts).

iDenfy’s KYB platform connects to over 180 company registries across more than 120 countries, pulling real-time data directly into your KYB workflow (with downloadable, ready-made PDF reports), which means your team is no longer dependent on outdated databases or incomplete public records. SOS business search, EIN verification, UBO verification, AML screening (PEP/Sanctions & adverse media), criminal background checks, or other important tasks like KYC verification for any related individuals (and custom questionnaires for faster business document collection) are all built-in options that you can enable with the KYB solution.

Still have doubts? Click here to get your free demo.