As of May 2026, the Financial Action Task Force (FATF), a major intergovernmental body responsible for setting high Anti-Money Laundering (AML) compliance standards all over the world, identifies numerous jurisdictions that share common characteristics, like weak AML frameworks. Other red flags for high-risk jurisdictions include high levels of corruption, sanctions exposure, and space in general where criminal activity can be a big issue.

If you’re a regulated entity and work in sectors like finance, depending on your risk appetite, you need to assess the level of risk when partnering with all clients, including individuals and businesses. The issue is that AML/CFT frameworks vary by country, exposing you to regulatory gaps and vulnerabilities. However, tools like FATF’s “Black” and “Grey” lists for countries with severe deficiencies help apply different onboarding workflows and due diligence measures.

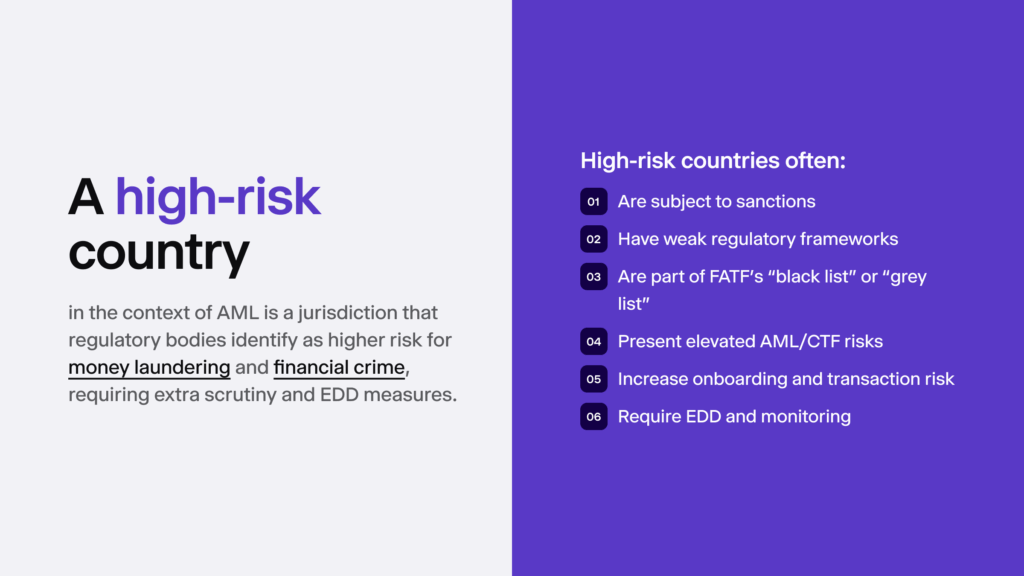

Jurisdictions that come from the “Black” or “Grey” lists require extra controls, like monitoring or even not being able to start a B2B relationship at all. Which countries make up the list of high-risk countries, how you should respond, what kind of automation tools can help you comply with AML standards, and more questions answered — all below.

What Does the Term “AML High-Risk Countries” Mean?

“AML high-risk countries” is a term used for jurisdictions that are considered riskier due to their weak AML frameworks. They are considered high-risk due to posing a heightened risk for various crimes: financial crime, money laundering, terrorist financing, the proliferation of weapons of mass destruction, etc. These countries are identified and reviewed constantly by regulatory watchdogs, such as the mentioned FATF, as a way to differentiate more risky countries that often require enhanced due diligence (EDD) measures and extra monitoring.

For example, Chad, Myanmar, or Haiti are such countries. They are among the highest-risk jurisdictions in the world. In contrast, the European Union averages a lower risk score of 3.96, compared to a score of 8+ for the mentioned regions, as shown in the Basel Index. Ultimately, regulatory watchdogs like the FATF assess various risk factors, in which jurisdictional risk plays a big part when identifying if a country is “high-risk”.

➡️ The Basel Index provides risk scores that are calculated using different factors. They include bribery and corruption levels, the overall quality of the jurisdiction’s AML/CFT framework, legal/political risks, financial transparency, as well as public transparency and accountability.

Automate your AML checks

Screen customers against global sanctions, PEPs, and watchlists in real time with iDenfy AML Screening.

AML Screening SoftwareWhat are High-Risk AML Sectors?

Crypto exchanges, virtual asset service providers (VASPs), money services businesses (MSBs), banking platforms, fintechs, luxury item and art dealers, or real estate and PropTech firms are considered regulated, high-risk AML sectors due to their exposure to large transaction volumes, speed, or limited transparency.

For example, art pieces can be used for money laundering. That’s why online art auctions carry out due diligence, both screening and identifying participants (buyers) and partners (artists) with KYC/KYB measures to ensure fair transactions.

Other examples of industries that are under strict AML scrutiny include iGaming and gambling platforms, precious metals, insurance, legal service providers, credit unions, and similar companies that require handling high-risk transactions, historically known to be prone to fraud.

Can You Do Business With a High-Risk Country?

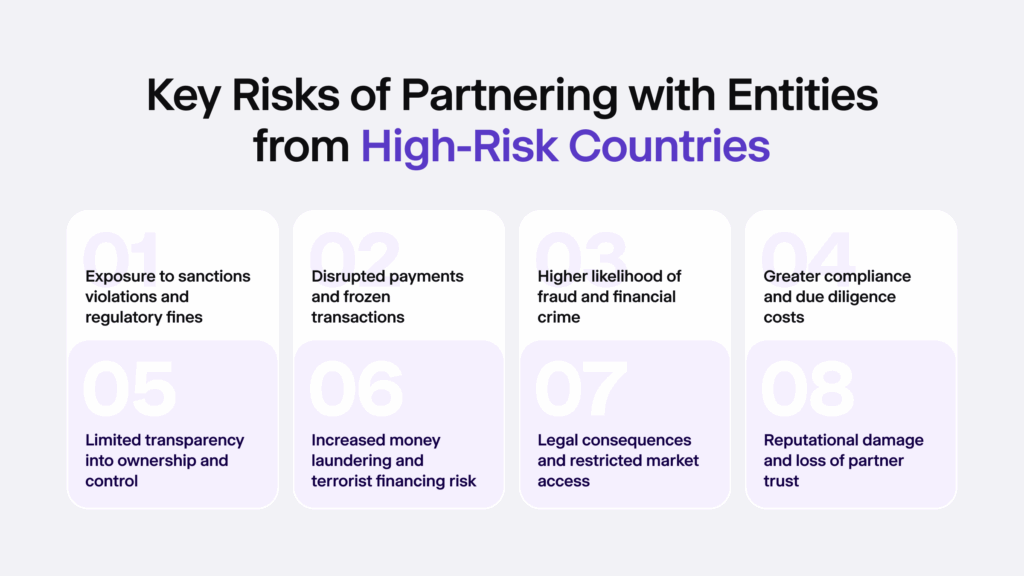

Yes. The FATF’s “high-risk country” label doesn’t automatically ban you from doing business, but it does require the application of EDD and, in some cases, additional screening processes to actually evaluate if the high-risk status is worth it and is appropriate for your AML risk assessment. In other words, starting a business relationship with such a business often increases operational risks and compliance costs linked to regulatory scrutiny.

So, what happens in practice? Here’s an example:

- An EU-based institution enters a partnership with a company that operates in a country on the FATF’s list of high-risk jurisdictions.

- The firm then faces closer supervision from regulators, including extra operational burdens like stricter reporting obligations or even restricted access to partner banks that process international payments on their behalf.

That’s why many businesses avoid such companies with some exceptions, unless the contract serves a clearly defined business purpose that justifies the higher risk, and, of course, supports proper AML controls.

What Makes a Country Fall Into the List of High Risk for Money Laundering?

You can say that most countries follow a standard approach and classify a country as high risk when 1) its AML/CTF frameworks are poor; 2) there are other factors, such as structural and economic weaknesses.

Universal risk factors that make a country prone to money laundering risks include those that are known to have:

- Large sectors where cash transactions dominate

- Widespread bribery and unstable governance

- Geographic proximity to drug trafficking and other terrorist financing networks

- Low tax regimes and limited transparency linked to the banking sector

It depends on the regulator and its criteria. Regulatory bodies constantly review jurisdictions to maintain up-to-date data.

🇺🇸 The US’s System For Identifying AML High-Risk Countries

The US follows recommendations from the Financial Crimes Enforcement Network (FinCEN) and, additionally, uses the lists presented by the FATF:

- Countries on the Black List are considered high-risk

- Countries on the Grey List are under stricter monitoring

Like in the EU, US-regulated institutions are required to apply EDD measures to foreign financial institutions when dealing with high-risk jurisdictions. Additionally, they are required to follow the risk-based approach (RBA) to AML compliance as a way to better identify and prevent potential money laundering activities.

Related: What is the Bank Secrecy Act (BSA)?

🇪🇺 The EU’s System For Identifying AML High-Risk Countries

Apart from FATF’s recommendations, the EU follows its own regime that defines the workflow for identifying high-risk jurisdictions:

- Prioritizing. Identifying and listing some big players first based on their impact on economic ties to the EU, or the links to the EU financial system. For example, the European Commission uses FATF’s list and then additionally conducts another assessment even if the FATF hasn’t flagged the selected country as “high-risk” yet. You can read more about this methodology here.

- Assessing. Evaluating each country’s AML/CTF framework and practical implementation across key areas, like money laundering criminalization, record-keeping, actions from legal authorities, or the application of CDD measures, and reporting suspicious activity. All these factors are primary or base criteria for keeping a transparent assessment of each monitored country.

- Listing. Inserting the identified high-risk countries into the EU’s high-risk third-country list. This automatically triggers EDD by law. That means all regulated entities are required to use extra due diligence measures on the high-risk/listed countries.

- Monitoring. Tracking the list and keeping up with changes that could affect the countries’ risk profiles. Similar to how user risk profiles change, the greylisted countries can improve and minimize risks. For example, the British Virgin Islands (BVI) are added to the monitoring section even though it’s a popular place for various crypto/payment startups due to the benefits of low-tax regimes.

Related: What are the EU’s Anti-Money Laundering Directives (AMLDs)?

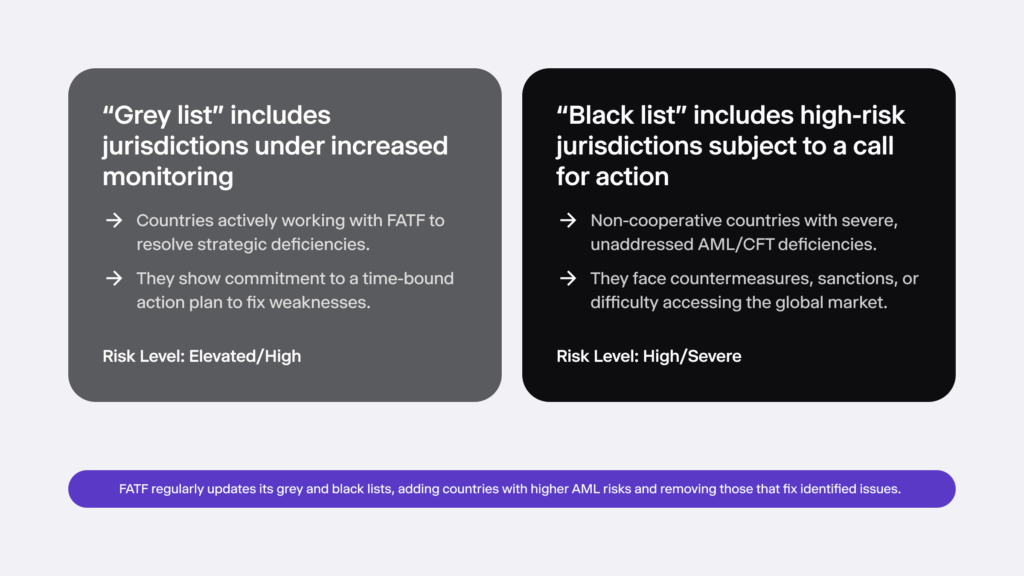

🌐 FATF’s Black List and Grey List System

The FATF sorts out two jurisdictional categories:

The FATF Black List

The countries on this list are officially known as the High-Risk Jurisdictions subject to a Call for Action. They present serious money laundering/terrorist financing risks. Examples include North Korea or Myanmar.

Blacklisted countries share patterns, as they are all known for:

- Mandatory EDD measures

- Severe AML/CFT deficiencies with limited or no commitment to remediation

- Elevated reputational and regulatory risk for companies working with them

- High likelihood of sanctions exposure and restricted access to global finance

The FATF Grey List

The countries on this list require monitoring to ensure that they’re committed to complying with AML/CTF policies and are continuing to change/adapt their frameworks accordingly. In simple terms, these countries have weaknesses in their systems and have agreed to fix them under close international monitoring and strict timelines.

Some factors that greylisted jurisdictions share in common:

- Gaps in AML/CFT systems (with future remediation plans)

- Necessary transaction monitoring (including periodic risk reviews)

- Required EDD measures (with expected changes in risk levels)

- Higher compliance costs (due to more complex onboarding flows required for clients from these jurisdictions)

While greylisted countries aren’t formally sanctioned, their status can still lead to reduced trade, higher scrutiny from banks, and limited access to international financial services, compared to a low-risk jurisdiction.

What is the Current List of AML High-Risk Countries?

The FATF has included the following jurisdictions:

High-Risk Jurisdictions (Black List)

- Iran

- Myanmar

- Democratic People’s Republic of Korea (DPRK)

Jurisdictions Under Increased Monitoring (Grey List)

- Angola

- Algeria

- Bolivia

- Bulgaria

- Cameroon

- Côte d’Ivoire

- Democratic Republic of the Congo

- Haiti

- Kenya

- Lao PDR

- Lebanon

- Monaco

- Namibia

- Nepal

- South Sudan

- Syria

- Venezuela

- Vietnam

- Virgin Islands (UK)

- Yemen

For example, Burkina Faso, Nigeria, Mozambique, and South Africa were removed from the increased monitoring list.

➡️ Keep in mind that this is the data from January, 2026. The FATF updates these lists three times a year, so countries on the list will likely change their status. You can keep an eye on the changes here.

If you want to automate your AML program and build custom onboarding and monitoring flows for high-risk clients, we got you. iDenfy’s end-to-end KYC/KYB and AML Screening Software covers multiple regions, helping you save time and costs with automation.

Book a demo to find out more.